Governance Token Design: Voting Power, ve-Tokenomics, and What Works

Governance token design determines how protocols coordinate. Covers voting structures, ve-tokenomics, and the five launch mistakes founders repeat.

Governance token design is the discipline of structuring onchain decision-making rights so that voting power reflects genuine protocol alignment rather than plutocratic wealth concentration. Every governance design must resolve three structural choices: the voting mechanism (how votes are counted), the power structure (who holds voting weight and how that weight is acquired), and the incentive design (what economic behavior the governance token rewards). Get any one of those three wrong and the governance layer becomes a liability.

The cost of bad governance design is not abstract. Compound's 2020 governance attack used delegated voting weight to push through a proposal that nearly drained the treasury (Source: Compound Governance Proposal 63, on-chain record). MakerDAO governance spent years fighting voter apathy that left critical risk parameters up to a shrinking pool of active delegates. The Curve Wars turned governance tokens into a bidding market where the highest bribe, not the most aligned holders, controlled emissions (Source: Curve Finance veCRV gauge weight governance, on-chain data). Each of those outcomes traces back to governance design decisions made at launch, not to market conditions.

This guide covers the three voting power models in active use, how ve-tokenomics works and when it is and is not appropriate, the most common launch errors, and the checklist questions every founder should answer before deploying a governance token.

#What Governance Tokens Actually Do (And What They Don't)

governance token: A governance token is a digital asset that confers formal onchain decision-making rights over protocol parameters to its holders, distinct from a utility token (which grants access to protocol features) and a security token (which represents an investment contract).

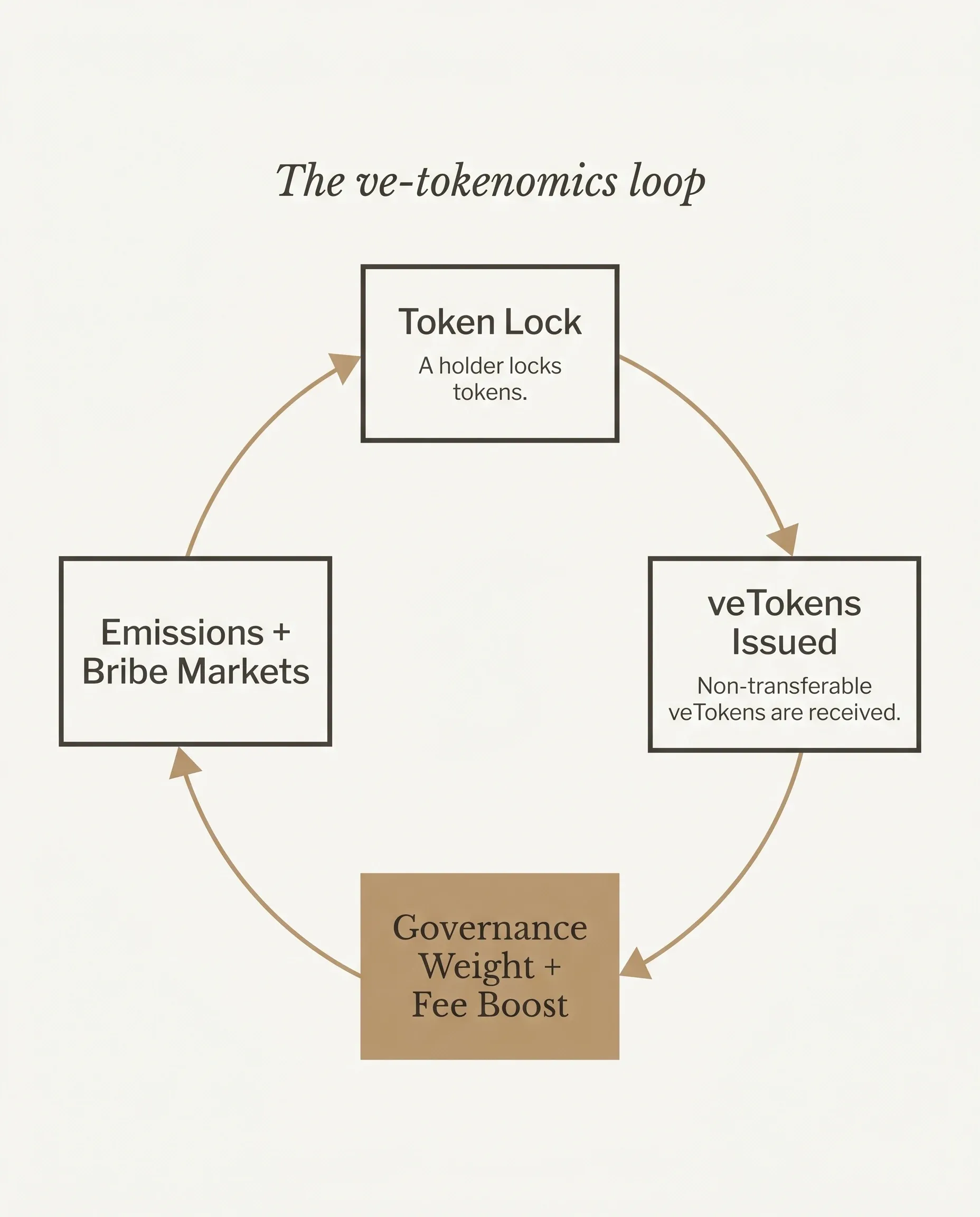

ve-tokenomics: Vote-escrow tokenomics is a governance incentive model in which token holders lock tokens for a fixed duration to receive non-transferable veTokens, which carry governance voting weight and fee distribution rights proportional to lock duration.

quorum: In onchain governance, a quorum is the minimum percentage of circulating token supply that must participate in a vote for the result to be binding. Without a quorum floor, proposals can pass with minimal participation from a small coordinated group.

A governance token is a formal claim on protocol decision rights. It is not, by default, a claim on protocol revenue. That distinction matters enormously for how you design the token and for how regulators may classify it.

A governance token can legitimately do two things: signal holder alignment with the protocol's direction, and coordinate parameter changes that require a distributed decision rather than a central operator. What a governance token cannot do without triggering a serious securities analysis is distribute protocol revenue to holders on a pro-rata basis. The moment a token starts looking like a dividend-bearing instrument, the Howey test analysis becomes fact-specific and jurisdiction-specific, and "it's just a governance token" is not a legal defense.

The most common design mistake is conflating governance rights with economic rights because it is convenient for fundraising. Institutional investors pushing for fee-sharing mechanisms, a governance token that earns yield from the protocol, understand exactly what they are asking for. Make that design choice with open eyes and with a legal opinion from counsel in your primary jurisdiction, not because it felt like a natural extension of the governance model.

Two things to avoid at the definitional level: utility tokens rebranded as governance tokens to avoid securities exposure (the wrapper does not change the substance), and dual-token structures where the governance token is presented as separate from economic rights while the two tokens are so mechanically intertwined that the separation is cosmetic.

#Voting Power Structures: The Three Design Decisions

Every governance token design is essentially a choice among three voting architectures, or a deliberate hybrid of them.

One-token-one-vote (token-weighted voting) is the default because it is the simplest to implement. One token equals one vote. Voting power is proportional to holdings. The risk is plutocratic capture: a small number of large holders can consistently outvote the broader community, and quorum requirements can be gamed by concentrating tokens ahead of a vote. The Compound governance incident is the canonical example. A single whale delegating to a controlled address submitted a proposal that would have transferred over $150 million in tokens to that address. The proposal passed initial quorum before the community mobilized to override it. Token-weighted voting works at scale when the holder base is genuinely distributed. It breaks down when early investors, founders, and associated entities hold a combined majority.

Quadratic voting addresses whale dominance by computing voting power as the square root of token holdings rather than the linear sum. A holder with 10,000 tokens gets 100 votes, not 10,000. This compresses the advantage of large holders and gives mid-size holders meaningful participation. The structural cost is sybil resistance: quadratic voting invites Sybil attacks where a single entity splits tokens across hundreds of addresses to multiply voting power. Effective quadratic voting requires identity verification or stake-weighted participation costs that make splitting economically irrational. For most protocols at launch, the tooling overhead of sybil-resistant quadratic voting outweighs the benefit. It is better suited to mature governance systems with established identity layers. The governance comparison framework at /blog/quadratic-voting-vs-token-weighted-voting covers the tradeoffs in detail.

Conviction voting and delegation take a different approach: time-weighted or delegation-based systems where holding longer, or delegating actively, accumulates more governance weight. Conviction voting, used by Gardens (1Hive's governance framework), requires that a voter signal conviction over time before a proposal passes. Proposals can only pass when accumulated conviction reaches a threshold. Delegation systems, popularized by Compound's Governor Bravo, let any token holder delegate their voting weight to an address (often a professional delegate or another holder). This concentrates actual governance participation among a smaller set of active participants while allowing passive holders to remain represented. The governance-minimization principle underlies both: the fewer decisions that require active participation, the more durable the governance system under low engagement conditions.

Here is how the four voting architectures compare across the dimensions that decide most launches. The fourth model, ve-tokenomics, gets its own section below, but it belongs in the comparison because most founders weigh it against the simpler three.

| Dimension | Token-weighted | Quadratic | Conviction / delegation | ve-Tokenomics |

|---|---|---|---|---|

| Sybil resistance | High (cost scales with holdings) | Low without an identity layer | Medium (delegation concentrates trust) | High (lock cost deters splitting) |

| Whale dominance risk | High | Low (square-root compression) | Medium (delegates can still concentrate) | High (early lockers entrench) |

| Participation rate | Low (passive holders rarely vote) | Medium (mid-size holders engage) | Higher (delegation covers passive holders) | Low to medium (locking is a barrier) |

| Implementation complexity | Low | High (needs sybil tooling) | Medium | High (lock accounting plus bribe markets) |

No architecture eliminates plutocracy entirely. The question is which failure mode your protocol can absorb and recover from.

#ve-Tokenomics: The Curve Model and Its Variants

Vote-escrow tokenomics, commonly called ve-tokenomics, was introduced by Curve Finance and has since been adopted across a significant portion of DeFi's governance layer.

The mechanics are straightforward. A holder locks their governance tokens for a defined duration (Curve allows locks of one week to four years). In exchange, they receive non-transferable veTokens (vote-escrowed tokens). VeToken balance determines two things: voting weight on gauge emissions (which liquidity pools receive CRV rewards) and fee distribution (50% of Curve's trading fees go to veCRV holders). Longer locks equal more veTokens. Holdings decay as the lock expiration approaches, creating an ongoing incentive to extend locks.

Ve-tokenomics spread because it solved a real problem: aligning long-term holders with protocol governance while penalizing short-term extraction. Protocols that adopted the model include Balancer (veBAL), Frax, Velodrome, and dozens of smaller forks. The consequence was the Curve Wars, a competitive dynamic where protocols seeking to direct CRV emissions toward their own liquidity pools began bribing veCRV holders through platforms like Votium and Hidden Hand. Convex Finance built an entire layer on top of veCRV, accumulating governance weight on behalf of CRV depositors and capturing a substantial fraction of veCRV supply.

The three structural risks of ve-tokenomics are worth naming directly.

Liquidity cliffs. When large lock tranches expire simultaneously, the protocol faces a wave of tokens returning to circulation. If the unlock is not staggered, sell pressure can be severe. Design for lock-expiry distribution, not just lock-depth.

Early-locker concentration. The first holders to lock tokens under a ve system accumulate disproportionate governance weight relative to later participants. In practice, this means the initial investor syndicate and the protocol team, who receive tokens first, often own a permanent plurality of governance power unless the system is designed to dilute early-locker advantage over time.

Bribery market decoupling. Once a bribery market exists, governance votes are driven by the highest payer rather than by the most aligned holders. For mature protocols with real fee revenue, this can be an efficient capital allocation mechanism. For early-stage protocols with no fee revenue, it is governance theater: decisions are made by mercenary capital with no long-term stake in protocol health.

Ve-tokenomics is appropriate when the protocol has meaningful fee revenue to distribute, a holder base with genuine long-term alignment, and a governance surface that is deep enough (gauge weights, fee parameters, risk parameters) to justify the complexity. It is not appropriate for early-stage launches, protocols without fee revenue, or teams that want governance as a marketing signal rather than a real coordination mechanism.

#Delegation and Governance Minimisation Frameworks

The governance-minimization principle argues that the less a protocol relies on continuous onchain governance, the more secure and durable it becomes. Every parameter that requires a vote is an attack surface. Every vote that requires quorum is an engagement risk.

Compound Governor Bravo introduced delegation as a practical response to governance apathy. Any COMP holder can delegate their votes to any address, including themselves, without transferring tokens. Professional delegates, researchers, and institutional participants have emerged as a class of active governance participants who hold delegated weight from thousands of passive holders. This concentrates decision-making among a smaller set of engaged participants while maintaining the distributed ownership of the token itself.

Optimism's bicameral Token House and Citizens' House is the most sophisticated current approach to separating economic governance from values-based governance. The Token House holds voting weight based on OP token holdings. The Citizens' House holds non-transferable voting rights based on Optimism Citizenship (a form of identity-based governance). Economic decisions and public goods funding decisions go to separate chambers. Neither can override the other without cooperation. It is not appropriate as a day-one governance structure, but it points toward where durable governance architecture is heading.

Practical guidance: if your protocol has fewer than 5,000 active token holders, you do not have the participation base to make complex onchain voting function reliably. Governance proposals with 0.5% participation rates are not governance; they are the appearance of governance. At that stage, lean into delegation or a transparent multisig with a clear published upgrade path toward progressive decentralization. Decentralizing before the participation base exists does not create community ownership; it creates a governance vacuum that concentrated actors fill.

#Governance Token Launch Decisions That Haunt Founders Later

These are the five governance design errors we see most often across the projects we advise. Each one is recoverable in theory, but each becomes harder to fix the longer it sits.

Minting governance rights to early investors at launch. When a protocol's initial token distribution gives investors 20-30% of supply with immediate governance rights, the governance structure is captured before the community exists. Low-float-high-FDV governance tokens are not just a price problem; they are a governance legitimacy problem. The community that shows up post-launch has no meaningful say. How you split supply at genesis decides who holds power on day one, so work through the token distribution model before you assign governance weight, and see the tokenomics audit checklist for how to audit this before it becomes a reputational liability.

No quorum floor. Proposals that can pass with 0.1% participation are not community decisions. They are decisions made by whoever showed up, often a coordinated actor with a specific agenda. Set a quorum floor that is high enough to be meaningful (5-10% of circulating supply is a reasonable starting range) and revisit it as participation data accumulates.

Missing time-locks between vote and execution. Without a delay (Compound's standard time-lock is 48-72 hours), a passed governance proposal can be executed before the broader community has a chance to respond, exit, or counter-mobilize. Time-locks are not bureaucracy; they are the window during which the community can catch governance attacks before they land.

Treating governance as marketing. "Community-governed" as a marketing line without governance substance corrodes trust faster than no governance claim at all. When the governance theater becomes visible, and it always does, the reputational damage exceeds whatever marketing value the claim generated. Real governance is accountability infrastructure, not a sales pitch. It sits alongside the other tokenomics mistakes that look harmless at launch and turn structural later.

Decentralizing governance before the product exists. Premature decentralization kills execution speed. When every parameter change requires a governance vote from day one, the protocol's ability to iterate quickly is hobbled before the product has found product-market fit. There is a real cost to governance overhead. Design a clear path toward governance maturity rather than governance theater at launch.

#How to Design Governance Token Incentives That Actually Align

The alignment test for any governance incentive is this: does the token reward holders for taking governance actions that improve protocol health, or for holding passively and extracting yield? These are not the same thing, and most governance token incentive structures conflate them.

Three incentive levers are available.

Fee distribution to active voters. When protocol fees are distributed to holders who participate in governance, the incentive connects economic reward to governance engagement. This is the ve-tokenomics model. The design question is how to define "participation" in a way that rewards genuine engagement rather than rubber-stamp voting.

Voting rewards. Subsidising governance participation directly (small token rewards for casting votes) lowers the participation cost for small holders and improves quorum. The risk is mercenary voting: holders who vote on every proposal without reading them to collect rewards. Voting rewards work best when combined with conviction or delegation mechanics that weight long-term engagement.

Locking mechanisms that penalize short-term extraction. Ve-tokenomics uses lock duration as a proxy for alignment. Time-weighted average balance voting uses holding duration. Both penalize governance participation by new entrants who acquired tokens specifically to influence a single vote, which is the Sybil pattern applied to governance rather than to wallets.

The warning on bribery markets bears repeating. Votium and Hidden Hand are capital allocation tools that mature protocols use because the underlying fee revenue makes bribery economically efficient. Early-stage protocols that adopt bribery markets before establishing real fee revenue are not accelerating governance; they are replacing governance alignment with governance mercenaries. The connection to token velocity is direct: a governance token that circulates primarily to collect bribes and then exit has the same velocity problem as a utility token with no sink. See the token velocity post for the design patterns that address this.

Governance token design cannot save a protocol with no revenue. It can only preserve or destroy whatever value the underlying business creates. The token is infrastructure. The business is the engine.

#ve-Tokenomics Alternatives: What Works When Curve's Model Doesn't Fit

Not every protocol needs Curve-style locking. Three alternative models address different constraints.

Time-weighted average balance (TWAB) voting. Rather than requiring a formal lock, TWAB computes each holder's voting power as the time-weighted average of their token balance over a trailing period. A holder who has held 10,000 tokens for six months has more governance weight than a holder who acquired 10,000 tokens yesterday. No lock required, no liquidity cliff, and the calculation is onchain-verifiable. The tradeoff is that there is no explicit economic reward for long-term holding, so the alignment incentive is weaker than ve-tokenomics. TWAB governance suits protocols that want to reduce manipulation risk without the lockup complexity.

NFT-based governance (non-fungible voting rights). A fixed supply of governance seats represented as non-transferable or transfer-restricted NFTs. Each seat carries one vote. This suits small protocol councils, multi-sig replacements, and governance structures where a defined set of participants needs to be accountable for decisions without the plutocratic dynamics of fungible token voting. The limitation is that seat distribution must be governed by a credible process; otherwise the initial seat allocation captures governance permanently.

Snapshot plus multisig execution. Off-chain governance (Snapshot) with on-chain execution via a trusted multisig. This is the pragmatic choice for protocols still centralized by design with a published roadmap to progressive decentralization. It separates the signaling function (gathering community input) from the execution function (making changes to the protocol). The risk is the trust model on the multisig signers. Design for multisig rotation and signatories that are accountable to the community, and publish a clear timeline for moving execution onchain as the protocol matures.

#The Governance Token Design Checklist Before You Launch

Eight questions to answer before deploying a governance token. If you cannot answer any of them with specificity, the governance design is not finished.

- Have you defined in writing what decisions governance can and cannot make? (Scope creep in governance is a real governance attack vector.)

- Does your voting mechanism match your current holder distribution? (One-token-one-vote with insider-concentrated supply is not community governance.)

- Do you have a quorum floor and a time-lock defined in the governance contract or in a governance framework document?

- Is fee distribution to token holders part of the design? If yes, have you received a legal opinion on securities classification in your primary jurisdiction? The tokenomics compliance post covers the post-FIT-21 compliance landscape for this class of design decision.

- Is your initial token distribution governance-diverse enough to prevent day-one insider capture?

- Does your governance design have a documented path toward minimization as the protocol matures and fewer parameters require frequent updates?

- Have you modeled a realistic whale-capture scenario against your governance architecture?

- Is your governance interface (Snapshot, Tally, on-chain forum) accessible to the non-technical holders who make up your community?

If a tokenomics audit has not covered these questions for your project, the tokenomics consulting engagement framework starts here.

#Governance Token Design Is Infrastructure

Governance token design determines whether a protocol can upgrade itself over time, defend against coordinated attacks, and maintain the holder trust that converts governance legitimacy into market credibility. No revenue model fixes a governance structure that has been captured. No marketing compensates for a governance token that the community knows is theater.

The protocols that have maintained governance credibility over multi-year time horizons are the ones that treated governance design as infrastructure: defined scope, matching mechanism to holder distribution, time-locks, quorum floors, and a clear path toward minimization rather than toward perpetual governance overhead.

If you're building onchain and need your governance token design to hold up under institutional scrutiny, book a discovery call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.