Tokenomics Compliance: What the Post-FIT-21 Era Requires of Token Design

Tokenomics compliance means building regulatory requirements into the token mechanism from the start. This post covers the FIT-21 and MiCA compliance surface for token designers.

Tokenomics compliance: The discipline of building regulatory requirements directly into a token model's mechanism, token classification analysis, transfer restriction architecture, KYC/AML integration, supply management controls, and investor protection documentation, so that compliance is structural, not added after launch.

Tokenomics compliance is the design discipline of building regulatory requirements into a token's mechanism from the start. It covers token classification, transfer restriction architecture, KYC/AML integration, supply management, and investor protection documentation. It is not the legal team's responsibility to add after mechanism design. It is the mechanism designer's responsibility to build in from day one.

Compliance is the architecture, not a feature. Projects that treat compliance as a post-launch legal task face a specific failure pattern: they build a mechanism that is structurally incompatible with the regulatory requirements their target markets impose. The retrofit is not a legal document. It is a re-architect of the token contract, the distribution model, and the investor documentation package. That doesn't work.

#The Compliance Landscape in 2026 and Where It Is Heading

Three regulatory regimes are converging to define what tokenomics compliance means in practice. By 2028, the distinction between "compliant" and "non-compliant" token models will be built into exchange listing requirements, institutional investor due diligence checklists, and regulatory enforcement priorities in every major market.

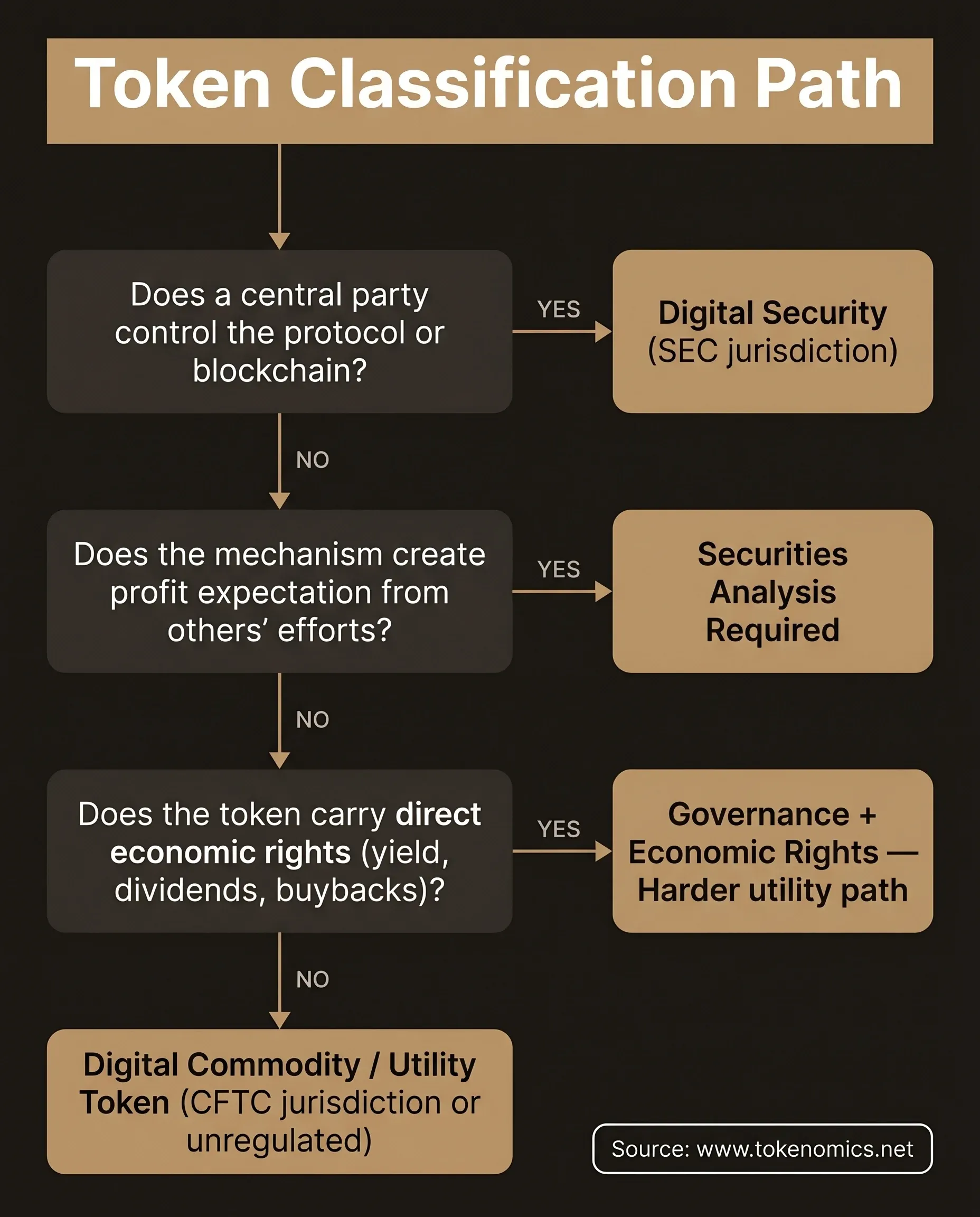

United States: FIT-21. The FIT-21 digital asset legislation creates two primary token categories: digital commodities (tokens where no central party has a controlling stake in the blockchain or associated protocol) and digital securities (tokens that do not meet the decentralization threshold). Classification is determined token-by-token, not protocol-by-protocol. The SEC retains jurisdiction over digital securities. The CFTC receives jurisdiction over digital commodities. The determination affects what exchange the token can list on, what investor protections apply, and what disclosures are required.

European Union: MiCA. The Markets in Crypto-Assets regulation creates three categories for token issuers: asset-referenced tokens (ARTs), e-money tokens (EMTs), and crypto-assets (everything else). ARTs and EMTs face the strictest tokenomics design requirements: authorization from a national competent authority, minimum capital requirements, reserve management rules for stablecoins, and transaction reporting requirements above the €1 million daily threshold. Stablecoin compliance under MiCA requires mechanism-level design choices, the reserve architecture, the redemption rights structure, and the governance path for reserve changes must be documented and enforceable.

Offshore jurisdictions. The offshore compliance advantage is narrowing in a defined direction. FATF travel rule requirements now apply in most offshore VASP jurisdictions. Regulatory arbitrage is harder than it was in 2021. Projects designing for offshore with no compliance architecture are designing for a market that is contracting.

FIT-21 tokenomics implications are not theoretical. The legislation establishes the regulatory framework that institutional investors will use to evaluate token compliance in the US market. Projects designed today that are compliant with FIT-21's digital commodity standards are ahead of the mandatory floor; projects designed for regulatory ambiguity are behind it.

Howey test: The four-part test derived from the 1946 US Supreme Court case SEC v. W.J. Howey Co. that determines whether a transaction constitutes an "investment contract" (and therefore a security) under US law. A transaction is a security if it involves (1) an investment of money, (2) in a common enterprise, (3) with an expectation of profits, (4) from the efforts of others. If a token mechanism creates a return expectation dependent on a founding team's or protocol's ongoing management work, it satisfies prong four and faces a securities classification risk.

MiCA ART (Asset-Referenced Token): Under the EU Markets in Crypto-Assets regulation, an ART is a token that purports to maintain a stable value by referencing multiple currencies, commodities, or crypto-assets. ARTs require authorization from a national competent authority, minimum own funds of at least €350,000 or 2% of average outstanding token value (whichever is higher), and reserve asset management in segregated, liquid instruments. MiCA EMT (E-Money Token): An EMT is a token that purports to maintain a stable value by referencing a single official currency. EMTs must be issued by an authorized e-money institution and carry the same capital and reserve requirements as ARTs, plus real-time redemption rights for all holders at par value.

#Token Classification: The Design Decision That Determines Everything

Token classification is not a legal judgment made after the fact. It is a consequence of specific mechanism design choices. The same token can be classified differently in the US and the EU because the classification frameworks differ. The same token can be reclassified if the protocol's decentralization posture changes post-launch.

Three mechanism design factors determine classification risk:

Profit expectation from others' efforts. The Howey test defines an investment contract as an investment of money in a common enterprise with an expectation of profits from the efforts of others. If the token mechanism creates a return expectation that depends on the founding team's or protocol's ongoing work, through staking yields funded by team effort, through governance token appreciation dependent on active protocol management, or through algorithmic peg mechanisms dependent on team intervention, the token faces a securities analysis risk.

Transfer restriction architecture. Tokens that can be freely transferred to any wallet without identity verification have a different regulatory profile than tokens with embedded transfer restrictions. ERC-3643 tokens, for example, can only be transferred to wallets that have passed the associated identity verification check. The restriction itself signals a securities-compliant design path; the absence of restriction signals a utility or commodity path.

Governance rights vs. economic rights. Governance tokens that grant voting rights without economic rights (no direct revenue distribution, no yield mechanics) have a cleaner utility token path in most jurisdictions. Governance tokens that distribute protocol revenue to holders, in the form of yield, dividends, or buy-back mechanics, face a harder securities analysis because the economic right resembles a dividend expectation tied to the protocol's management performance.

The tokenomics regulatory standard for each classification path is defined by these three factors. The mechanism design choices are not downstream of the legal opinion. They are the input to it.

#Compliance by Design: Five Mechanism Decisions

Five mechanism design decisions create or eliminate compliance risk at the tokenomics layer.

Transfer restriction architecture. ERC-3643 or ERC-1400 embed transfer restrictions at the smart contract level, transfers are validated against an on-chain identity registry before execution. ERC-20 tokens with compliance requirements applied only at the application layer have a structural gap: the application layer can be bypassed, and the token itself enforces no restriction. Regulators have closed this gap in enforcement actions. The architectural standard for regulated token contexts is contract-level enforcement, not application-level policy.

KYC/AML integration. For tokens interacting with regulated markets, KYC must be built into the wallet whitelist enforced at the contract level. Off-chain KYC with on-chain enforcement is the institutional standard: the identity verification happens off-chain (by a regulated KYC provider), and the result is written on-chain as a whitelist authorization. An ERC-20 token that applies KYC at the front end only is not compliant with the requirement in regulated contexts, the restriction is not enforced by the token.

Supply management and inflation controls. Unbounded inflation creates regulatory exposure when token holders expect the protocol's management to control supply outcomes. Algorithmic supply controls with transparent, governance-documented parameters reduce the management-effort dependency that creates securities risk. The supply management documentation must include what the maximum inflation rate is, who can change it, under what governance process, and with what notification to holders.

RWA compliance mechanics. For tokens representing real-world assets, the minimum compliance components are: an SPV (special purpose vehicle) structure establishing legal ownership of the underlying asset, a legal opinion on the token's classification and the SPV's ownership rights, income distribution via smart contract (automated, not discretionary), and periodic NAV attestation from a third party. Centrifuge on-chain credit markets and Maple Finance institutional lending represent the institutional standard for on-chain RWA compliance architecture in credit markets. RWA compliance is fact-specific; the above components are the floor, not the ceiling.

Stablecoin compliance. For fiat-backed stablecoins targeting the EU market, MiCA EMT requirements include: authorization from a competent authority (a national financial regulator), minimum capital (typically 350,000 EUR or 2% of average outstanding token value), reserve management in liquid instruments, real-time redemption rights for holders, and transaction reporting above the €1 million daily threshold. Stablecoin mechanism design must accommodate these requirements from day one; retrofitting a deployed stablecoin to meet MiCA's reserve management and redemption requirements requires mechanism changes that affect existing holders.

#The Compliance Documentation Package

The compliance documentation package is the evidence set that exchanges, institutional investors, and regulators request. Building it before listing is not optional, it is what separates projects that list on Tier 1 venues from those that don't.

Token classification legal opinion. The foundational document. Answers: what is this token, in what jurisdiction, under what regulatory framework, and what investor protections apply. The legal opinion is based on the mechanism design analysis, it reads what the token does, not what the whitepaper says it is.

Transfer restriction documentation. How transfer restrictions are enforced at the contract layer, what the governance path is for updating the restriction logic, and what the emergency governance path is if restrictions need to be modified urgently.

KYC/AML integration specifications. Who conducts the KYC, what data elements are verified, how the verification result is linked to the on-chain whitelist, and how the system handles whitelist updates when a holder's compliance status changes.

Stablecoin reserve documentation (for stablecoin issuers). Reserve composition, custodian documentation, attestation frequency, redemption policy, emergency governance path for reserve changes.

RWA documentation (for RWA token issuers). SPV structure documentation, legal opinion on asset ownership, income distribution mechanics, NAV attestation provider and frequency.

These documents collectively constitute the tokenomics compliance component of the investor data room. Projects that have completed this package move through diligence faster, because the questions have been answered before the meeting.

#Common Compliance Failures in Token Design

After reviewing dozens of tokenomics compliance architectures across 80+ engagements, the failure patterns are predictable.

Applying compliance at the UI, not the contract. A front-end KYC gate with an ERC-20 token is not compliant in regulated contexts. The restriction must live in the token contract. Front-end compliance enforcement is one deployment of a compliant contract away from circumvention.

Designing for US regulatory ambiguity. The SEC has demonstrated it will classify tokens as securities when the mechanism supports the inference. Designing for ambiguity is not a compliance strategy. It is a deferred enforcement event.

Treating MiCA as a European-only concern. Any stablecoin or asset-referenced token targeting EU users must be MiCA-compliant regardless of the issuer's jurisdiction of incorporation. The MiCA requirement follows the user, not the issuer's address.

Updating supply mechanics post-launch without governance documentation. When a protocol changes its inflation rate or emission schedule after launch, the change must be documented as a governance decision with a clear process. Undocumented post-launch changes to supply mechanics create a securities compliance risk: they suggest that a central party is actively managing the token's economic parameters.

Not obtaining a legal opinion before listing. Every listing is a regulatory event. Tier 1 exchanges require a legal opinion as part of the listing review package. Projects that seek listings without one are asking the exchange to assume a regulatory risk the exchange is not willing to take, which makes the project an unlisting candidate when the compliance gap is discovered.

The regulatory environment is not getting more lenient. MiCA is fully in force. FIT-21 is advancing. Offshore regulatory arbitrage is narrowing. Projects that design their token mechanisms for compliance today are building for the mandatory standard of 2027-2028. Projects that defer compliance to a post-launch legal layer are building for a retrofit that is significantly more expensive than designing right in the first place.

#Frequently Asked Questions: Tokenomics Compliance

What is tokenomics compliance? Tokenomics compliance is the design discipline of building regulatory requirements directly into a token's mechanism from the start, covering token classification analysis, transfer restriction architecture, KYC/AML integration at the contract level, supply management governance documentation, and investor protection documentation. It is the mechanism designer's responsibility, not a legal layer added after launch.

What does FIT-21 require at the token design level? FIT-21 creates two primary US token categories: digital commodities (tokens where no central party holds a controlling stake in the blockchain or associated protocol) and digital securities (tokens that don't meet the decentralization threshold). Classification is determined token-by-token. If a token is classified as a digital security, it trades on SEC-regulated venues and requires full securities disclosure compliance. If classified as a digital commodity, it trades on CFTC-regulated markets. The classification determination happens at the mechanism design level, the decentralization posture of the token and its associated protocol is the input.

What does MiCA require for stablecoin issuers? MiCA creates two stablecoin categories: Asset-Referenced Tokens (ARTs) and E-Money Tokens (EMTs). Both require authorization from a national competent authority. Capital requirements are at least €350,000 or 2% of average outstanding token value, whichever is higher. Reserve assets must be held in segregated, liquid instruments. EMTs must offer real-time redemption at par to all holders. Transaction reporting applies above the €1 million daily threshold. All of these requirements must be built into the token mechanism from launch, stablecoin reserve architecture, redemption mechanics, and governance paths for reserve changes cannot be retrofitted.

What is the difference between contract-level and application-level compliance enforcement? Application-level compliance enforcement means the restriction (KYC check, transfer gate, investor whitelist) lives only in the front-end interface, the application that users interact with. Contract-level enforcement means the restriction is baked into the token smart contract itself: a transfer cannot execute unless the contract's on-chain validation passes. ERC-3643 and ERC-1400 implement contract-level enforcement. ERC-20 tokens with front-end-only compliance have a structural gap: a transfer can be executed directly against the contract by anyone who interacts with it without going through the front end. Regulators have closed this gap in enforcement actions, contract-level enforcement is the required standard in regulated token contexts.

What is required for an RWA token's minimum compliance architecture? The four minimum components for a real-world asset token's compliance architecture are: (1) an SPV (special purpose vehicle) structure establishing the legal ownership chain from the token to the underlying asset, (2) a legal opinion on the token's regulatory classification and the SPV's asset ownership rights, (3) income distribution via smart contract (automated, not discretionary, manual distribution creates a management-effort dependency), and (4) periodic NAV attestation from an independent third party at a defined frequency. These are the floor, not the ceiling; jurisdiction-specific requirements and asset-class-specific rules apply.

What is a token classification legal opinion and when is it required? A token classification legal opinion is a formal legal document that analyzes a specific token under the applicable regulatory framework(s) and concludes what the token is, a security, a commodity, a utility token, an ART, an EMT, in specified jurisdictions. It answers: what is this token, under what framework, in which jurisdiction, and what investor protections and exchange listing requirements apply. It is required before listing on any Tier 1 exchange (which requires it as part of the listing review package), before closing an institutional investment round, and before offering the token to users in any regulated jurisdiction. Projects that seek listings without a token classification legal opinion are asking the exchange to absorb a regulatory risk the exchange is not willing to take.

How does the Howey test apply to token design? The Howey test applies to token design through its fourth prong: the expectation of profits from the efforts of others. If a token's mechanism creates a return expectation that depends on a founding team's or protocol's ongoing work, through staking yields funded by team-directed emissions, through governance token appreciation dependent on active protocol management, or through algorithmic mechanisms that require team intervention to maintain, the token satisfies Howey's fourth prong and faces a US securities classification risk. Mechanism design choices that reduce management-effort dependency (algorithmic supply controls with transparent governance parameters, yield generated by protocol-level market activity rather than team-directed emissions, clear decentralization benchmarks for the associated protocol) reduce the Howey risk at the token level.

If you're building onchain and need your tokenomics compliance documentation to hold up under regulatory and institutional scrutiny, book a strategy call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.