The Token Distribution Model: Allocation, Vesting, and Liquidity

A token distribution model defines how total supply is allocated across stakeholders, governed by vesting schedules, and supported by liquidity. Learn the Distribution Trinity framework.

Token distribution model: A framework specifying total token supply allocation across stakeholder groups (team, investors, ecosystem, treasury, public sale), the vesting schedules governing each bucket's unlock timeline, and the initial liquidity structure supporting price discovery at TGE, engineered together as three interdependent decisions.

A token distribution model is a documented framework specifying how a token's total supply is allocated across stakeholder groups, what vesting schedules govern each allocation bucket, and how initial liquidity is structured at token generation. Getting this right is not about hitting the right percentage in any one bucket. It is about designing allocation, vesting, and liquidity as a coordinated system.

Most distribution failures we see across 80+ engagements are not caused by bad allocation percentages in isolation. A 20% team allocation is reasonable, the same allocation with a 6-month cliff and no initial liquidity creates a catastrophic sell-pressure window in the first 12 months. The failure is in the interdependencies between the three decisions, not in any one number. Token allocation strategy is the visible layer. The model underneath it determines whether the project survives price discovery.

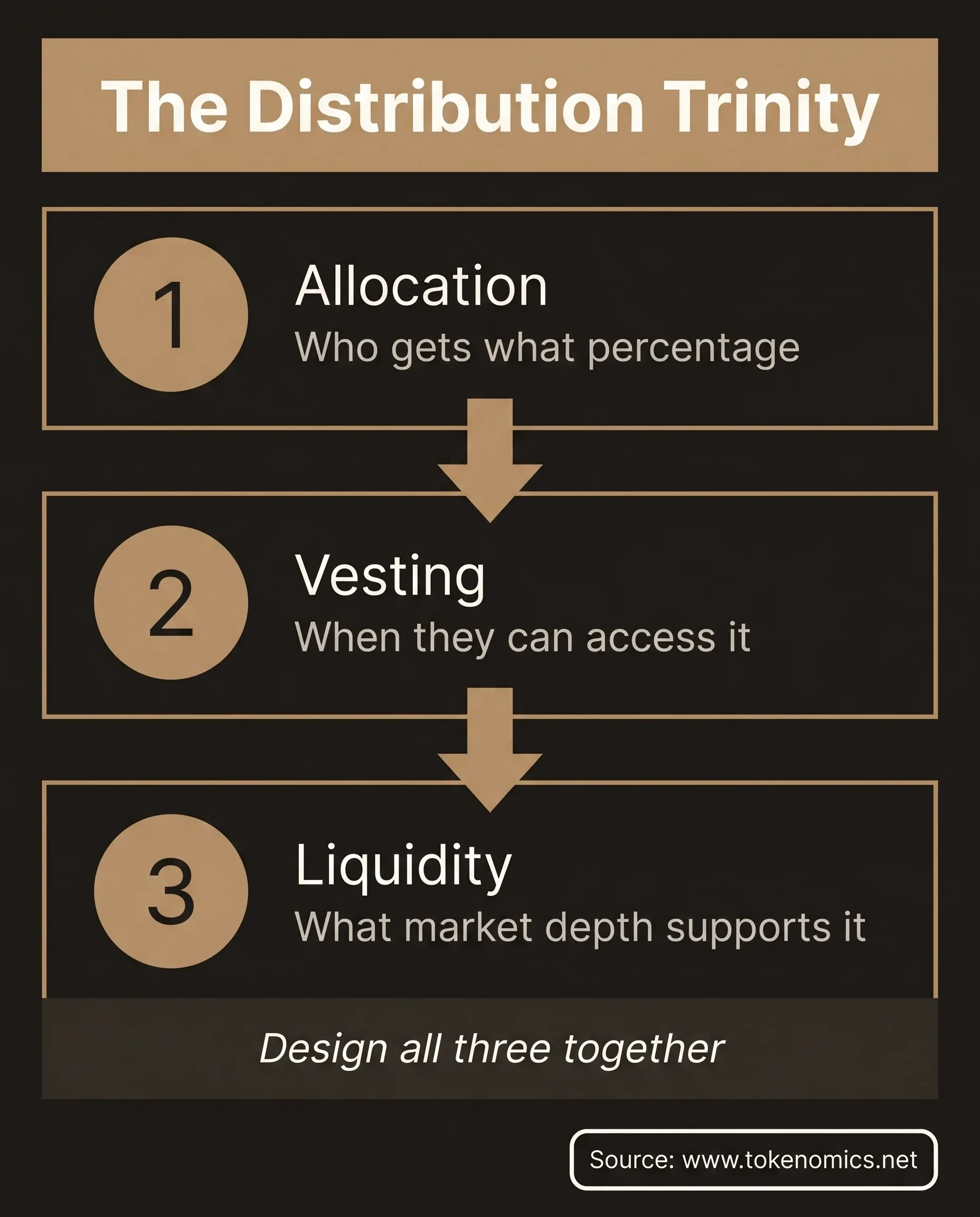

#The Distribution Trinity Framework

We call this the Distribution Trinity: three interdependent decisions that must be designed together before a single allocation percentage is set. Each decision depends on the others, and changing one without adjusting the others shifts risk in ways that compound.

The three decisions are: Allocation, who gets how much of the total supply, and by what rationale. Vesting, when each allocation bucket converts to circulating supply, and at what rate. Liquidity, what pool depth, market maker terms, and exchange infrastructure supports price discovery without creating a systematic sell wall at critical unlock windows.

The interdependency looks like this in practice. A 20% team allocation with a 12-month cliff and 36-month linear vest is institutional standard. Pair it with an initial liquidity pool of 2% of circulating supply and no market maker, and the team's first unlock event in month 13 occurs against a liquidity pool that cannot absorb the sell pressure. The allocation was fine. The liquidity was not. The distribution model failed.

Circulating supply: The number of tokens that are currently in the market and available for trading, excludes tokens locked in vesting contracts, DAO treasury, and ecosystem reserves that have not yet been released.

Token Generation Event (TGE): The moment a token protocol creates and distributes tokens for the first time, marking the beginning of the token's supply schedule and the start of vesting clock timers for all stakeholder buckets.

The Distribution Trinity framework forces founders to model all three decisions simultaneously before committing to any number. Distribution determines destiny. The projects that survive the first 18 months post-TGE almost always have allocation, vesting, and liquidity designed as a coordinated system from the start.

#Allocation: The Stakeholder Map

Allocation is the layer investors see first. The standard institutional benchmark ranges below reflect what exchange listing teams and institutional LPs have come to expect based on patterns across hundreds of reviewed token models. Deviations require documented justification.

Investor allocation (30-40% combined). Seed rounds typically receive 5-10% of total supply. Private rounds typically receive 10-15%. Strategic partners and protocols receive 5-8%. KOL and advisory allocations typically fall at 2-5%. The combined investor allocation above 40% signals excessive early investor concentration, too much early-stage capital with exit rights relative to the project's operational and ecosystem needs.

Team allocation (10-20%). This is the most scrutinized allocation bucket. Anything above 20% requires specific justification: what work has the team already done to earn a larger stake? Anything above 25% is a flag for institutional investors. Anything above 30% typically kills a listing application at Tier 1 exchanges. The team allocation is a long-term incentive, not a founders' reward; it must be paired with a vesting schedule that demonstrates alignment with the protocol's 3-5 year success horizon.

Ecosystem and community (20-30%). This bucket covers grants, liquidity mining programs, community rewards, and airdrops. The problem we see: founders allocate 25% to "ecosystem and community" without defining what programs the allocation funds, on what timeline, and with what governance over deployment. An undefined ecosystem allocation reads as an unallocated float with a better name. Investors ask for a spending plan at diligence. Have one.

Treasury and DAO (10-20%). The operational reserve. Must have clear governance over deployment, a DAO vote requirement, a multi-sig threshold, or a defined committee with mandate. Treasury allocation without governance controls creates a centralized spending risk that undermines the decentralization narrative.

Public sale and IDO (5-15%). The smallest bucket in most institutional token designs. Public sale is for retail price discovery, not capital formation. The smaller this number, the lower the post-listing sell pressure from retail participants who bought at a different price than institutional rounds.

Foundation reserve (5-10%). Long-term development funding. Typically the longest lockup in the model, 48-60 months linear vest with no cliff is standard. The foundation reserve should not have any TGE unlocks.

Token vesting design begins here: every allocation percentage maps to a vesting schedule, and every vesting schedule maps to a set of unlock events that must be stress-tested against the projected liquidity profile.

#Vesting: The Supply Unlock Architecture

Vesting schedule design is a supply-side pressure model. Every unlock event releases potential selling capacity into the circulating supply. The design question is not "when can stakeholders access their tokens?" It is "when will sell pressure be released, in what quantity, against what liquidity depth?"

Team vesting standards. Minimum: 12-month cliff, 36-month linear vest. TGE unlock for the team should be 0%. Any team TGE unlock above 5% is a systemic sell-pressure flag. The team's first access to tokens should occur after the project has operated for at least a year, demonstrated protocol function, and established a liquid secondary market.

Seed investor vesting. Standard: 6-month cliff, 24-month linear vest. TGE unlock for seed investors should be 0-5%. Seed rounds come in at the earliest stages with the highest risk; a longer lockup compensates for that risk premium while aligning the investor's exit with a maturing market.

Private investor vesting. Standard: 3-6 month cliff, 18-24 month linear vest. Private round investors get somewhat more favorable terms than seed because they typically come in at a higher valuation; this is standard. TGE unlock at 0-10%. Above 15% TGE unlock for private investors is a flag.

Strategic and advisory vesting. Standard: 6-month cliff, 12-18 month linear vest. Strategic partners often have short-term value delivery windows (introductions, integrations, listing support) and their lockup is appropriately shorter. But advisors with 0 cliff and immediate vesting are a red flag, if the advice has been rendered, there is no incentive alignment left.

Public sale vesting. Typically no lockup or 1-3 month linear vest. This is the only bucket with immediate or near-immediate exit rights; retail participants purchasing in a public sale accept a fair market value and expect liquidity. The public sale bucket should be small enough that even immediate selling does not overwhelm the initial liquidity pool.

Ecosystem and community releases. Best practice is milestone-based or performance-gated releases: ecosystem grants disbursed on delivery, liquidity mining rewards paid weekly against live protocol metrics, community rewards earned against participation benchmarks. Time-based ecosystem releases create predictable sell-pressure windows that sophisticated traders can position around.

Treasury and DAO unlocks. No automatic unlocks. The treasury is liquid when governance authorizes spending. This is the cleanest design: the treasury's circulating supply impact is a governance decision, not a mechanical schedule.

Unlock event timing against the price discovery window is the most critical analysis in the token distribution model. Map every unlock event against the target exchange listing date. The first 90 days post-listing are the highest-risk window for sell pressure from early-stage investors reaching return targets. A well-designed model spaces its first large unlock event after 180 days post-listing minimum.

#Liquidity: The Market Infrastructure

Liquidity design determines whether price discovery is constructive or destructive after TGE. Most founders under-invest in this decision because liquidity is operational, not narrative, it doesn't appear in the whitepaper in a compelling way. It appears in the market's behavior in the first 30 days.

Initial liquidity depth. Target: 5-10% of circulating supply at TGE in DEX liquidity at launch. For a token with $10M in circulating supply at TGE, that means $500K-$1M in initial DEX liquidity. Thin initial liquidity (below 2%) creates a systematic slippage problem: even moderate sell orders move the price materially, which triggers more selling, which triggers further price movement. The spiral is not unpredictable. It is a mechanical consequence of the design.

Market maker agreements. Market makers provide order book depth on centralized exchanges. What they cover: bid-ask spread maintenance within a defined range, minimum volume floor, order book depth at defined price levels. What they do not cover: guaranteed price support or guaranteed token price. Market maker agreements have exit provisions, understand what happens when the agreement terminates and how that affects liquidity depth. Institutional investors reviewing the token distribution model want to see the market maker agreement terms, not just confirmation that one exists.

DEX versus CEX split. Institutional investors prefer CEX price discovery for initial listing; the order book provides more information than an automated market maker curve. On-chain institutional liquidity products such as Ondo Finance tokenized treasury products have shown that institutional-grade secondary market participation is possible in a DeFi context, but the base requirement is a deep initial pool. DeFi-native projects often launch on a DEX first, which is structurally valid, but the initial liquidity depth requirement is higher because the AMM curve provides less resistance to large sell orders than a deep order book.

Liquidity incentive programs. Token-based LP rewards are an invisible token creation program. Every LP token earned by a liquidity provider adds to the circulating supply float when the provider exits the position. Model LP rewards as a secondary supply issuance schedule and treat them as an extension of the emission curve. A token liquidity strategy that relies on 20% APY LP incentives to maintain depth is a model with 20% APY in supply inflation. Sustainable beats aggressive.

#What Investors Look For in the Distribution Model

Institutional investors run a sell-pressure model against the token distribution model. The question they are answering is: at what circulating supply, held by whom, with what cost basis, will selling pressure exceed buying demand?

Concentration analysis. What percentage of circulating supply is in the hands of investors with a low cost basis and near-term unlock events at TGE, at 6 months, and at 12 months? Tokens where 60%+ of circulating supply at TGE is held by early-stage investors with below-market cost basis are concentration-risk tokens. The sell-pressure window starts at the first cliff. The 53% token failure rate over five years is substantially concentrated in projects where this analysis was unfavorable and unaddressed (Source: CryptoRank token market data).

Cliff alignment. Do team and investor cliffs align constructively with the exchange listing timeline? A 12-month team cliff that coincides with a target 12-month listing date means the team has no locked incentive in the listing's first day. The more defensible design: the team cliff expires 180 days post-listing, so the team has a 6-month post-listing period where they are fully locked.

Post-listing unlock schedule against liquidity. Are unlock events paced against a projected growing liquidity pool, or against a static initial liquidity? A model where the largest unlock events occur in months 13-18 post-TGE, when the liquidity pool is expected to be deeper and secondary market trading volume is established, is more defensible than a model where large unlocks occur at months 6-9.

Documentation standard. Investors expect to see the full distribution model in the data room: allocation table by bucket, vesting schedule table by bucket, initial liquidity plan, market maker agreement summary, and a sell-pressure model at 3 unlock scenarios. Projects that provide only an allocation pie chart have not built a distribution model.

#Common Distribution Mistakes

After reviewing token distribution models across dozens of engagements, the failure patterns are consistent.

Treating allocation percentages as the whole model. The allocation pie chart is one layer of a three-layer system. Allocation without vesting architecture and liquidity planning is an incomplete model. We see projects present to institutional investors with a beautifully designed allocation graphic that has no vesting schedule and no liquidity plan attached. The meeting ends early.

Giving early investors a shorter lockup than the team. This inverts the intended incentive structure. If investors have a 6-month cliff and the team has a 12-month cliff, investors can exit before the team. Institutional LPs notice this and ask why the founders are more locked than the people who funded them.

Using token-based LP rewards without supply impact modeling. LP mining programs add tokens to the circulating supply. This is not a marketing program. It is a secondary emission schedule. Failure to model LP rewards as supply expansion produces surprises in the circulating supply figures that appear in exchange listing reviews.

Not mapping unlock events against the liquidity profile. The unlock schedule and the liquidity depth must be designed as a coordinated system. A 10% investor unlock in month 6 against a $200K liquidity pool produces a different outcome than the same unlock against a $2M liquidity pool. Design for the liquidity conditions you expect, not the ones you hope for.

Setting the ecosystem allocation without a defined spending plan. Institutional investors ask for a deployment roadmap for ecosystem funds during due diligence. "For ecosystem development" is not a plan. It is an answer that costs you time and investor confidence. Per the FIT-21 digital asset legislation governance provisions, DAO-controlled treasury deployments above defined thresholds may require documented governance processes in regulated contexts.

Optimizing the distribution model for the whitepaper, not for price discovery. The whitepaper tells the story. The distribution model governs what happens in the secondary market. Projects that design distribution for narrative appeal (maximum community participation, maximum decentralization) without stress-testing the supply mechanics create structural vulnerabilities that the market finds within 90 days.

#Frequently Asked Questions

What is the Distribution Trinity in token design? The Distribution Trinity is a framework that treats allocation, vesting, and liquidity as three interdependent decisions that must be designed together. Most distribution failures happen not because any single percentage is wrong but because the three layers are designed independently, a reasonable allocation paired with an aggressive vesting cliff and thin initial liquidity creates sell-pressure conditions that a reasonable allocation alone would never produce. The framework forces modeling all three simultaneously.

What percentage of token supply should go to the team? The institutional benchmark for team allocation is 10-20% of total supply. Anything above 20% requires documented justification for institutional investors and exchange listing teams. Above 25% is a flag. Above 30% typically fails a Tier 1 exchange listing review. The team allocation must be paired with a vesting schedule, 12-month cliff and 36-month linear vest at minimum, that demonstrates alignment with the protocol's long-term success rather than an early exit.

What is the minimum vesting standard for early investors? Seed investors: 6-month cliff, 24-month linear vest, TGE unlock at 0-5%. Private round investors: 3-6 month cliff, 18-24 month linear vest, TGE unlock at 0-10%. TGE unlock above 15% for any investor bucket is a systemic sell-pressure flag. The vesting standard exists to align investor incentives with protocol development, investors who can exit immediately after listing have no remaining incentive to support the project.

How much initial liquidity does a token need at launch? The target minimum is 5-10% of circulating supply at TGE in DEX liquidity at launch. Below 2% creates systematic slippage problems: even moderate sell orders move the price materially, which triggers further selling. Initial liquidity is not optional infrastructure, it is the mechanism by which price discovery is constructive rather than destructive in the first 30 days post-listing.

Why is ecosystem allocation a red flag if it is not defined? An undefined ecosystem allocation reads as an unallocated float with a better name. Institutional investors ask for a spending plan during due diligence: what programs, on what timeline, with what governance over deployment? Projects that cannot answer these questions lose investor confidence. An ecosystem allocation above 25% without a documented deployment plan is one of the most common reasons we see diligence processes stall.

What is the sell-pressure model that investors use to evaluate token distribution? Institutional investors model the distribution by asking: at what circulating supply, held by whom, with what cost basis, will selling pressure exceed buying demand? They analyze concentration (what percentage of circulating supply at TGE, 6 months, and 12 months is held by early-stage investors with low cost basis), cliff alignment relative to the listing date, and whether unlock events are paced against a growing liquidity pool. Projects that can answer each question with documented data move through diligence faster.

What happens if large unlock events coincide with the exchange listing? Large unlock events that coincide with or immediately follow the exchange listing create a predictable sell-pressure window. Early-stage investors who have been locked since the seed round reach their liquidity event exactly when the token enters price discovery with new retail buyers. The result is almost always a structured drawdown in the first 60-90 days. The defensible design: the first large unlock event occurs at least 180 days post-listing, when the secondary market is more liquid and the price discovery window has closed.

Distribution determines destiny. The token distribution model is the technical architecture that determines whether the project's secondary market supports the protocol's development or undermines it. Projects that design the model right, allocation, vesting, and liquidity as a coordinated system, give themselves the foundation to build. Projects that don't create the conditions for their own failure.

If you're building onchain and need your token distribution model to hold up under institutional scrutiny, book a strategy call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.