Token Velocity: Why High Velocity Destroys Value and How Design Fixes It

Token velocity is the rate at which a token circulates through an economy. High token velocity compresses price regardless of protocol usage. This post explains the mechanism and the five design decisions that fix it.

Token velocity: The rate at which a token circulates through an economy, measured as the number of times a token changes hands in a given period. High token velocity compresses token price because the monetary equation of exchange (MV=PQ) is inversely proportional: when velocity increases and supply is constant, price falls. The token velocity problem is a mechanism design failure, not a market condition.

Token velocity is the rate at which a token circulates through an economy. A high-velocity token is one that changes hands frequently, acquired for a purpose, used immediately, and sold. A low-velocity token is one that holders retain, stake, lock, or otherwise hold rather than circulate. The token velocity problem arises when a protocol's token architecture provides no rational reason to hold the token, so every holder immediately sells after use.

The token velocity problem is not a market problem. It is a mechanism design problem. Protocols that treat velocity as a downstream market variable to be solved with trading incentives or exchange listings have misdiagnosed the failure mode. The velocity problem is created at the point of token design, by what the token is required to do and whether the protocol provides a rational reason to hold rather than immediately sell.

Monetary equation of exchange (MV=PQ): The foundational equation for analyzing token price dynamics, where M = token supply, V = velocity (transactions per period), P = token price, and Q = quantity of goods or services transacted. The equation states that the total value of transactions (PQ) equals the money supply times its velocity (MV). In a token economy with fixed supply and growing transaction volume, price is determined by the relationship between velocity and transacted quantity: if velocity grows faster than transacted quantity, price is compressed downward. Token designers use MV=PQ to identify whether price stagnation is driven by supply, velocity, or insufficient economic activity captured by the token.

veTokenomics (vote-escrowed tokenomics): A token locking mechanism in which holders lock their tokens for a defined period to receive "vote-escrowed" tokens (ve-tokens) that carry governance weight and, in some implementations, a revenue share. First implemented by Curve Finance (veCRV). The longer the lock period, the greater the governance weight assigned. veTokenomics reduces velocity by removing locked tokens from circulation, but velocity reduction is limited to governance-motivated holders, typically a minority of total token supply. veTokenomics without economic coupling (no revenue share to ve-token holders) is a partial velocity solution; veTokenomics with revenue share creates a rational return incentive that extends hold demand beyond governance participants.

#How Token Velocity Works and Why It Destroys Value

The monetary equation of exchange, MV=PQ, applies to token economies with direct consequences for token designers. In a token economy: M is the token supply, V is velocity (the number of times the token changes hands per period), P is the token price, and Q is the quantity of goods or services transacted using the token.

If supply M and transacted quantity Q are held constant, price P and velocity V are inversely proportional. Doubling velocity halves price, all else equal. This is not a theoretical relationship. It is a mechanical consequence of the equation. A protocol that doubles its transaction volume, growing Q, while simultaneously doubling token velocity achieves no price appreciation. Growth without value capture is the defining pattern of the token velocity problem.

The structural cause is token utility architecture. When a token's only function is as a medium of exchange, "acquire the token to use it, then sell it", there is no rational reason to hold it between uses. Every acquisition is followed by an immediate sale. This creates persistent sell pressure regardless of protocol adoption. Protocol usage can be growing while token price stagnates or falls, because every new user is a new source of sell pressure.

The high token velocity pattern in crypto is most visible in three common token types. CryptoRank token market data consistently shows that utility tokens with no enforced hold mechanics underperform governance tokens with economic coupling across comparable protocol adoption curves. First, utility tokens required to pay protocol fees but immediately convertible back to stablecoins after payment, rational users hold the minimum balance required for the transaction. Second, governance tokens with no economic rights, voting utility alone does not generate a return expectation, so non-governance participants have no hold incentive. Third, reward tokens with no sink mechanism, tokens distributed as incentives that recipients immediately sell to realize value.

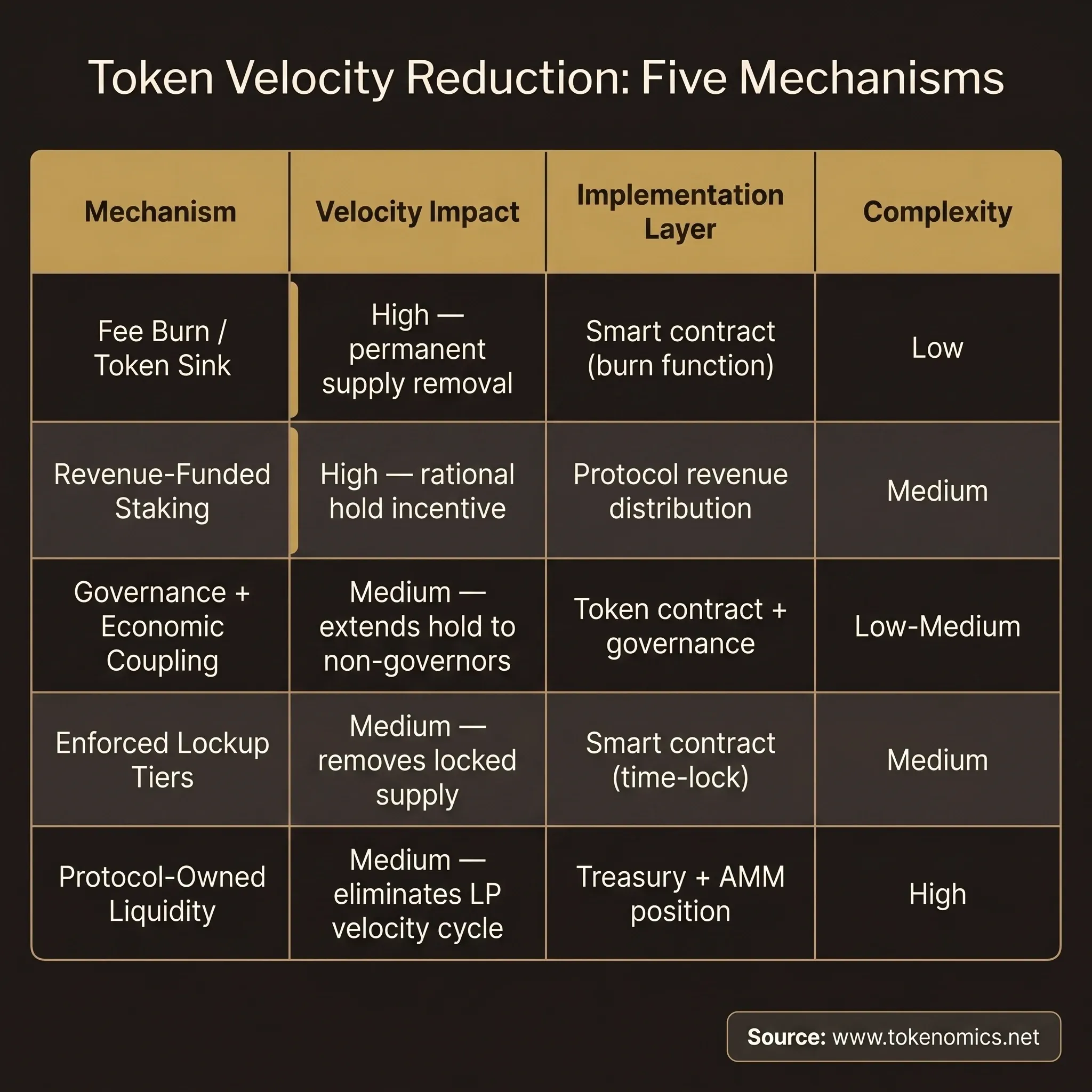

#The Five Velocity-Reduction Mechanisms

Five mechanism design decisions reduce token velocity structurally. Each creates a rational reason to hold, not a social incentive or a marketing message, but an enforced economic incentive embedded in the token's architecture.

Token sinks (burn mechanics). A token sink permanently removes tokens from circulation, reducing M and applying upward pressure on P independent of velocity changes. Fee burn mechanics, where a percentage of protocol fees is used to purchase and burn tokens, create a mechanical link between protocol activity and supply reduction. EIP-1559's fee burn mechanism is the canonical implementation: each transaction permanently removes a portion of the fee from supply. The key design variable is what percentage of fees are burned versus distributed. A higher burn percentage creates stronger deflationary pressure; a lower percentage preserves more for distribution to stakeholders. Either way, the sink creates a supply-side velocity buffer.

Value-accrual staking (economic staking, not inflationary staking). Staking that distributes a share of protocol revenue to stakers gives holders a rational return reason to hold. When a protocol's staking yield comes from on-chain economic activity, swap fees, lending spread, liquidation revenue, stakers are holding the token to earn a claim on that revenue stream. Tokens that are staked are not circulating, which directly reduces velocity. The critical distinction: yield must come from protocol revenue, not from new token emissions. Emission-funded staking rewards are not value accrual. They are inflation distributed to stakers while diluting all other holders. A 40% APY funded by new token mints is a dilution schedule, not a yield program.

Governance rights with economic coupling. Pure governance tokens, tokens that grant voting rights and nothing else, have a weak hold incentive for non-governance participants. When governance rights are coupled with economic rights (revenue share, fee reduction, priority access to protocol functions), the governance token becomes an income-producing asset. The hold incentive extends beyond governance-motivated holders to any rational participant who values the economic claim. Economic coupling does not require a complex mechanism: a percentage of protocol fees distributed proportionally to governance token holders achieves the coupling without additional contract complexity.

Tiered access and utility lockups. Tokens required to be locked, not just spent, to access premium protocol tiers create enforced hold demand. The design distinction is between spending and locking: a token that is spent leaves the holder's wallet; a token that is locked remains in the holder's wallet but is inaccessible for a defined period. Smart-contract time-locks enforce the lockup without relying on holder discipline. The protocol tier architecture must make the lockup meaningful: the premium tier must offer sufficient value that rational holders choose to lock tokens to access it.

Protocol-owned liquidity (POL). When a protocol controls its own liquidity rather than renting it from incentive-chasing liquidity providers, it removes a significant velocity source. Mercenary LP dynamics, where LPs enter for incentives and exit when incentives end, create cyclical velocity spikes: emission → LP entry → LP exit → sell. POL absorbs the liquidity function into the protocol's balance sheet, removing that velocity cycle. Uniswap Protocol fee mechanics demonstrate how on-chain liquidity can be structured as a durable protocol function rather than a rented incentive. The protocol's liquidity does not chase incentives, so the velocity source is eliminated.

#Why Staking Alone Does Not Solve the Token Velocity Problem

The most common velocity-reduction attempt is adding staking with attractive APY. It is also the most common velocity-reduction failure. The mechanism is seductive: staking demand creates buy pressure, high APY attracts new stakers, and the staked supply appears to reduce circulation. The structural problem is that emission-funded staking is velocity laundering, not velocity reduction.

The inflationary staking cycle works like this: new tokens are minted as staking rewards, expanding the supply M. If velocity V is unchanged and the quantity of transacted goods Q does not grow proportionally with M, price P must fall. The early stakers who entered at high APY exit with their yield at higher prices; later stakers face a diluted token. The protocol has converted its velocity problem into a dilution problem, different failure mode, same outcome.

Real velocity reduction through staking requires revenue-funded yield. The protocol's on-chain economic activity, swap fees, lending spread, protocol fees, funds the yield paid to stakers. Revenue-funded yield does not expand the token supply. It redistributes value from protocol users to token holders. Stakers earn a return because the protocol earns revenue, not because the protocol mints new tokens to pay them. This is the distinction between how to reduce token velocity sustainably and how to simulate velocity reduction temporarily.

The governance-only staking problem compounds this. veTokenomics, where token holders lock their tokens for governance weight, reduces circulating supply without creating a revenue claim for non-governance participants. The velocity reduction is real but narrow: governance-motivated holders lock, but holders who are not interested in governance have no rational reason to participate. In a typical protocol, governance-motivated holders are a small percentage of total token supply. The velocity reduction from veTokenomics alone is partial.

#Designing for Low Velocity from Day One

The token velocity problem is cheapest to fix at design time. Post-launch, retrofitting velocity-reduction mechanics requires mechanism changes that affect existing holders: a governance vote to implement a fee burn, a token migration to add veTokenomics, a treasury restructuring to establish POL. Each retrofit has coordination costs, governance risk, and incumbent holder resistance. Designing for low velocity from day one eliminates the retrofit.

The design checklist for low-velocity token architecture has five questions.

What is the token required to do, and does the protocol enforce that requirement at the contract level? A token that is optional for any protocol function has elastic demand, rational users replace it with a cheaper alternative whenever possible. A token required at the contract level to access core protocol functions has inelastic demand within that function.

What percentage of protocol revenue is distributed to token holders, and through what mechanism? Revenue share creates a rational return expectation tied to actual protocol usage. The share percentage and distribution mechanism determine how strong the hold incentive is. Zero revenue distribution means the only rational reason to hold is governance participation or speculative appreciation.

Is there a fee sink that burns tokens proportional to usage? A burn mechanic tied to on-chain activity creates deflationary pressure that scales with adoption. As usage grows, the burn accelerates, compressing supply. This is the opposite of the high token velocity pattern: growth reinforces price stability rather than amplifying sell pressure.

Is liquidity protocol-owned or rented? Rented liquidity creates mercenary LP dynamics and a recurring velocity source. POL eliminates that dynamic. The transition from rented to owned liquidity has upfront cost (the protocol must capitalize the liquidity) but creates a permanent velocity-reduction structural advantage.

What is the governance design, and does it carry economic coupling? Pure governance tokens with no economic rights give non-governance participants no rational hold incentive. Economic coupling, even a small revenue share, extends the rational hold incentive to a broader holder base.

The DeFi protocols that will attract institutional capital in 2027-2028 will be those with documented, enforced velocity-reduction mechanics. Institutional due diligence asks a direct question: what is the rational reason to hold this token? Emission-funded APY is not an acceptable answer to a sophisticated allocator. Revenue-funded yield, enforced lockups, and fee sinks are.

#Common Token Velocity Mistakes in Protocol Design

After 80+ protocol tokenomics engagements, the velocity design failures follow predictable patterns.

"Utility" tokens with no enforced utility. A token described as a utility token in the whitepaper but accepted alongside ETH and USDC as one of three payment options has no enforced demand. Rational users pay in the cheapest currency available. The utility token's demand is discretionary, which means it has no mechanically enforced hold incentive. Enforced utility means the protocol accepts only the native token for core functions, or requires the token to be locked for tier access, at the smart-contract level.

Emission-funded staking presented as yield. New token emissions are not yield. They are inflation distributed proportionally to stakers while diluting all non-stakers. The protocol that presents 40% APY funded by token emissions is distributing dilution to those who participate while compressing the value of those who don't. Real yield, revenue-funded distribution to stakers, is a fundamentally different mechanism.

Governance token with no economic rights. A pure governance token that grants voting rights but zero economic rights gives non-governance participants no rational reason to hold. Governance-only tokens have a structurally limited holder base: insiders who received the token at low cost and large stakeholders who value protocol control. The broader market has no return expectation.

Token buybacks without burn. Buying tokens on the open market and returning them to the treasury reduces circulating supply temporarily, but treasury-held tokens are potential future supply. They create a sell pressure expectation: the market prices in eventual re-release. Burn is permanent removal; treasury accumulation is deferred supply. The distinction matters for velocity: burned tokens never return to circulation; treasury tokens can.

Liquidity mining programs that amplify velocity. High-emission liquidity mining programs accelerate the velocity cycle: emissions are distributed to LPs → LPs claim rewards → LPs sell rewards to realize value → sell pressure. High-emission LM is a velocity amplifier. Protocols that run aggressive LM programs and then add staking APY to compensate are layering one velocity source on top of another.

The token velocity problem compounds over time. A protocol with high velocity and no sink mechanism accumulates sell pressure as adoption grows. The fix becomes harder as the holder base expands and the governance complexity increases. Protocols that design for low velocity from day one avoid the retrofit problem entirely, and build the institutional-grade tokenomics architecture that the 2027-2028 market will require.

#Frequently Asked Questions: Token Velocity

What is token velocity? Token velocity is the rate at which a token circulates through an economy, the number of times a token changes hands within a defined period. It is the V variable in the monetary equation of exchange (MV=PQ). High token velocity means the token changes hands frequently; low token velocity means holders retain it for extended periods. Token velocity is driven by the token's utility architecture: tokens whose only function is as a medium of exchange (acquire, use, sell) have structurally high velocity; tokens that provide a rational return reason to hold have structurally lower velocity.

Why is high token velocity bad for token price? High token velocity compresses token price through the mechanics of MV=PQ. If token supply M is fixed and the quantity of transacted goods Q grows at the same rate as velocity V, price P remains constant. But when velocity grows faster than underlying economic activity, the common pattern for utility tokens with no hold incentive, price falls regardless of protocol adoption. This creates the "usage without value capture" pattern: growing protocol transaction volume paired with stagnant or declining token price. High token velocity is not a market problem, it is a token design problem.

What is the token velocity problem? The token velocity problem is the mechanism design failure in which a token's utility architecture provides no rational reason to hold, so every holder acquires the token to use it and immediately sells. The result is persistent sell pressure that scales with protocol usage: the more the protocol is used, the more sell pressure the token experiences. The token velocity problem is most common in utility tokens required to pay fees (but immediately convertible to stablecoins after payment), governance tokens with no economic rights (no rational hold incentive for non-governors), and reward tokens with no sink mechanism (recipients immediately sell to realize value).

How do you reduce token velocity? To reduce token velocity, you build mechanisms that give holders a rational economic reason to hold rather than sell. The five proven velocity-reduction mechanisms are: (1) fee burn mechanics, permanently removing tokens from supply proportional to usage; (2) revenue-funded staking, distributing protocol fee revenue to token stakers (not inflationary emissions); (3) economic coupling of governance rights, revenue share tied to governance token holding; (4) smart-contract-enforced lockups for tier access, requiring token locking (not just spending) for premium protocol functions; and (5) protocol-owned liquidity, eliminating mercenary LP velocity cycles by capitalizing the protocol's own liquidity. The key principle: velocity reduction mechanisms must create a rational economic incentive, not just a social convention.

What is the difference between revenue-funded staking and inflationary staking? Revenue-funded staking pays staking yield from actual protocol economic activity, swap fees, lending spread, liquidation revenue. It does not expand the token supply; it redistributes value from protocol users to token holders. Inflationary staking pays staking yield by minting new tokens as rewards. It does expand the token supply: every staking period, the total token supply grows. The practical difference is that revenue-funded staking is a genuine yield mechanism (value transferred from protocol activity to holders), while inflationary staking is a dilution mechanism that benefits early participants at the expense of later ones. Protocols presenting inflationary APY as "yield" are running a dilution schedule with the appearance of yield.

What is protocol-owned liquidity and how does it reduce token velocity? Protocol-owned liquidity (POL) is a mechanism in which the protocol itself holds and manages its liquidity rather than renting it from external liquidity providers using emissions incentives. The velocity-reduction effect is structural: incentive-rented LP programs create a velocity cycle (emissions distributed to LPs → LPs claim rewards → LPs sell → sell pressure). When the protocol owns its liquidity, that cycle is eliminated. The protocol's liquidity is not chasing yield; it is serving the protocol function of enabling trading. POL requires upfront capital to establish (the protocol must fund the liquidity position), but it eliminates a recurring velocity source and removes the mercenary LP dynamic permanently.

When should you design for low token velocity? At the token design stage, before launch. The token velocity problem is cheapest to fix at design time, fee burn mechanics, revenue share parameters, and lockup architecture are straightforward to implement in the initial token contract. Post-launch, retrofitting velocity-reduction mechanics requires governance votes, token migrations, and mechanism changes that affect existing holders. Each retrofit step has coordination costs, governance risk, and the potential for incumbent-holder resistance. Protocols that launch with inflationary staking and later attempt to transition to revenue-funded yield face exactly this problem: the migration is technically and politically difficult. Design for low velocity from day one.

If your protocol has a token velocity problem, or if you're designing a token and want to build velocity-reduction mechanics in from the start, book a strategy call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.