7 Tokenomics Mistakes That Kill Projects Before Launch

We've diagnosed 80+ projects. These 7 structural errors cause post-TGE collapse. See the mistakes and what good design looks like.

Tokenomics mistakes are design decisions that create predictable, avoidable failure. Tokenomics mistakes, in short, are structural design errors baked into a token model before TGE. They are not bad luck. They are not market volatility. They are structural choices built into a token model before TGE that produce identifiable failure modes: concentrated sell pressure, governance capture, regulatory exposure, and incentive misalignment. We've seen the same seven errors across more than 80 projects. Most were correctable before launch. Several were not.

The consequence of getting this wrong is not a dip. It is a post-TGE price collapse that erodes community trust in the first 90 days, frozen fundraising when institutional investors look under the hood and walk away, and enforcement attention when the token's legal architecture wasn't designed for the current regulatory environment. The mechanism failing is the business failing. Those two things are not separate.

Seven structural errors appear across the projects that come to us after something has gone wrong, and across the ones that come to us before launch so we can find them first. Both sets are instructive.

#Why Tokenomics Fails (And Why It's Usually Structural, Not Strategic)

The instinct after a post-TGE price collapse is to blame market conditions. Sometimes that's accurate. More often, the market is doing exactly what the design told it to do.

The 2022 and 2023 unlock cycles made this visible at scale. Projects with FDV-to-circulating-supply ratios above 15x entered the market with a structure that produced sustained, predictable sell pressure as vesting schedules ran. The mechanics were visible in the supply tables before TGE. The outcomes were visible in the price charts 12 to 18 months later. Market conditions accelerated the timeline. The design set the trajectory.

A token without sustainable revenue mechanics is a countdown timer. The clock starts at TGE. How long it runs depends on how much community capital can absorb supply before real demand develops. Projects that designed for the fundraise instead of for the business ran out of time faster than they expected.

The seven errors below are where that clock gets set. Fixing them is not about finding smarter mechanics. It is about connecting the token design to the business underneath it.

#The Seven Tokenomics Mistakes We See Across 80+ Projects

#Mistake 1: Designing Supply Without a Revenue Model

The most common error is also the most upstream. A team builds a token supply structure, an emission schedule, a circulating supply curve, all of it modeled with precision, without ever anchoring the demand side to a real revenue mechanism.

Ten-year emission schedules exist on slide decks for projects that have no clear answer to this question: where does demand come from once emissions slow? The answer is not "ecosystem activity." That is circular. Demand comes from value created by an underlying business. If the business model is not specified, the token supply model is a fiction expressed in percentages.

Revenue-First Design means the token structure is a consequence of the revenue model, not a parallel track. Map how the protocol earns money. Identify which participants capture that value and how. Then design the token to sit in the path of that value creation, not beside it. Supply caps, emission rates, and burn mechanics are all secondary. The primary question is "what is the economic reason for this token to exist?"

Projects that answer that question before modeling supply have a design. Projects that model supply first and answer the question later have a problem that will surface at the worst possible time.

Here is the diagnostic question we run on every engagement at this stage: if the protocol stopped distributing token rewards tomorrow, would any participant's behavior change in a way that still benefits the protocol? If the answer is no, the token is not doing real work. It is moving capital from later participants to earlier ones, which is not a business model.

The fix requires going upstream. We document the revenue mechanism before opening the supply modeling spreadsheet. Where does money come from? Who pays it, and to whom? How does the business capture a portion of that value sustainably? The supply model is built as a consequence of those answers, not as their precondition.

#Mistake 2: Allocation That Front-Loads Insiders

When we see an allocation table where team plus investor allocation sums to 40% or more with vesting that completes inside 18 months, the supply structure is working against the community from day one.

The historical pattern is consistent. Concentrated insider allocations with short vesting schedules produce sell pressure events at the 12-month and 18-month marks that the open market cannot absorb at current liquidity depth. The price action is not random. It is a calendar. (Source: CryptoRank token unlock data, 2022-2024 cohort analysis.)

Sustainable distribution looks different. Team and investor combined allocation in the 25-35% range with a 12-month cliff and 3-4 year linear vest. Ecosystem and community allocation in the 40-50% range, governed through a multi-sig treasury with disbursement criteria. The remaining portion allocated to liquidity provisions and grants programs with defined spend rates.

Distribution determines destiny. The allocation table is the first document institutional investors review. Projects that front-load insiders are communicating something about whose interests the token design actually serves. That communication lands.

The institutional benchmark has shifted. Two years ago, 40% team-plus-investor allocation with 18-month vesting was standard. Today, institutional due diligence teams flag it as a risk item. The projects that attract institutional capital in the current cycle arrive with allocation structures that are defensible on paper and verifiable on-chain, with cliff and linear vest parameters that match the liquidity depth the token can realistically support at launch.

Insider allocations are not inherently wrong. Founders and early investors took real risk and should be compensated for it. The error is sizing that compensation against fundraise valuation rather than against the token's ability to absorb the sell pressure those allocations will generate. Those are different numbers. Most allocation tables optimize for the first. Almost none model the second.

#Mistake 3: Vesting Designed for Optics, Not Mechanics

A four-year linear vest with a 12-month cliff sounds responsible. It is, until you model the daily unlock rate against the available liquidity depth.

We've seen founders proud of their vesting schedule discover that their token's liquidity depth, measured at the 30-day average daily volume at the cliff date, cannot absorb even 0.5% of daily unlock without material price impact. The schedule looked clean on a slide. The mechanics produced a sell cliff at month 13 that looked exactly like the 12-month cliffs the schedule was designed to avoid.

Vesting is a sell-pressure management tool, not a legal formality. The question is not "how long does vesting run?" The question is "what is the market's capacity to absorb supply as it unlocks, and does the unlock rate match that capacity?"

Monte Carlo stress testing against liquidity depth scenarios should happen before the vesting parameters are finalized. Ten thousand simulations across a range of liquidity depth assumptions and unlock scenarios produce a distribution of outcomes. Founders who see that distribution before TGE can adjust the cliff, the linear rate, or the liquidity bootstrap target. Founders who see it after TGE are managing damage.

The practical output of that stress testing is a liquidity bootstrap target. If the model shows that the token needs $X in average daily volume to absorb the daily unlock rate without material price impact, that number becomes a hard input for the exchange listing strategy and the market-maker agreement. Projects that run the stress test know their number. Projects that don't are hoping the market is liquid enough when the cliff arrives.

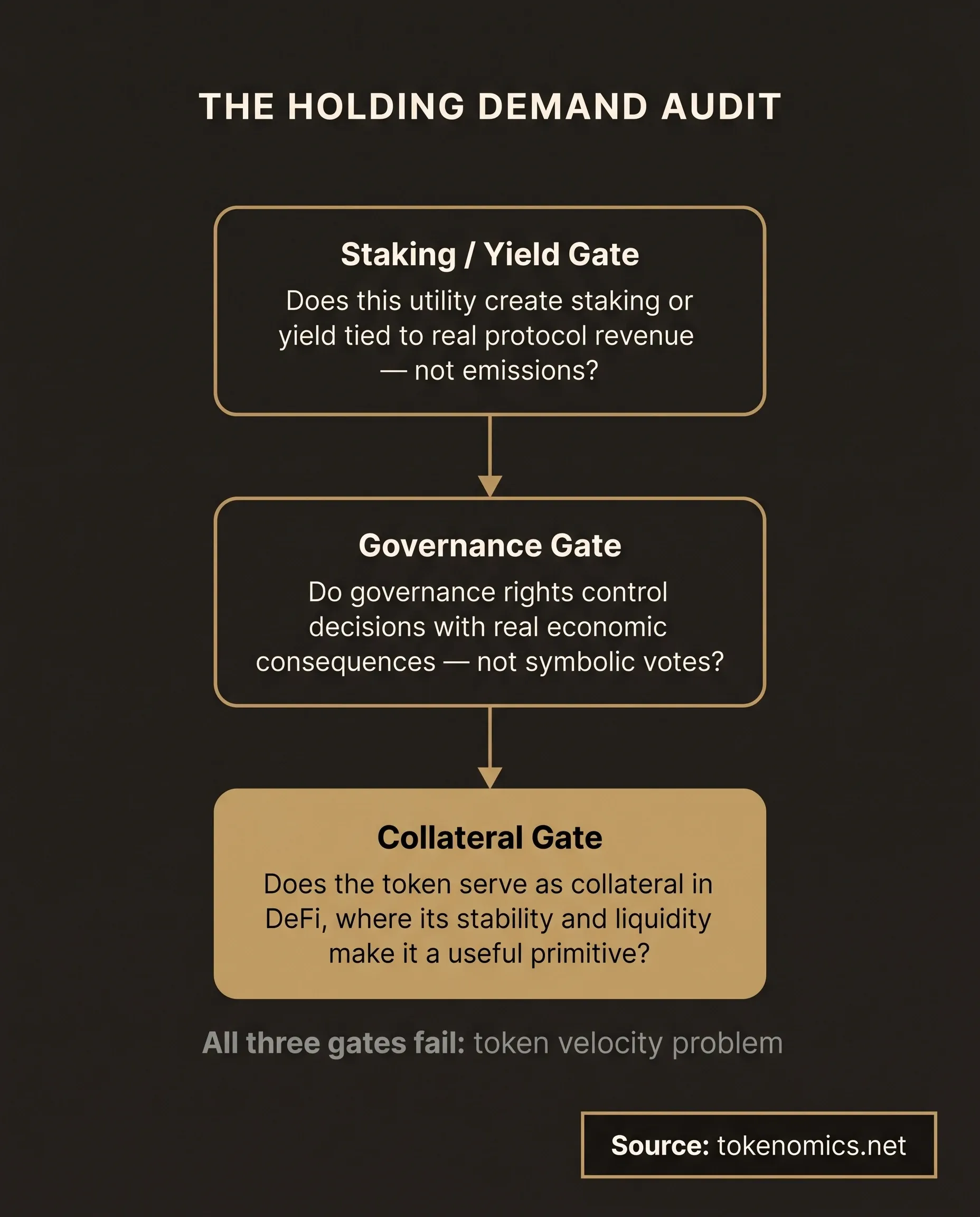

#Mistake 4: Token Utility That Doesn't Create Holding Demand

Utility tokens where every utility event is a spend event have a token velocity problem. The token changes hands fast. There is no economic reason to hold it. The market equilibrates at whatever price clears the float, and that price is lower than the team modeled because the model assumed holding demand that the design never created.

Utility is not the same as holding demand. Using a token to access a protocol service is not a value accrual mechanism. The token cycles through the system quickly. A high-frequency spend token behaves like a fee coupon, not like equity in the business.

Real holding demand comes from three sources. Staking or yield tied to actual protocol revenue, not emissions. Governance rights over decisions with real economic consequences, not symbolic votes. Collateral utility in a broader DeFi context where the token's stability and liquidity make it useful as a primitive. Well-designed DePIN tokenomics incentive structures illustrate this clearly: node operators hold the token because holding is how they participate in the network's revenue, not because they were told to.

Projects that audit utility design for holding demand separately from usage demand find the gap early. The question to ask for each utility: if a rational actor uses this utility today, what is their economic reason to hold the token tomorrow? If the answer is "nothing specific," the utility does not create holding demand.

The utility audit is not complicated but it does require working through each use case individually. Access control utilities often fail the test because the token grants access but doesn't accrue value from that access. Payment utilities often fail because the payment routes through the token without any portion staying in it. Burn mechanics can pass the test when they are funded by real protocol revenue, and fail when they are funded by treasury reserves that will eventually run out.

We have seen protocols with seven distinct utility functions where five of them failed the holding-demand test. The market found this before the team did. Doing the audit before launch is less expensive.

#Mistake 5: Governance Without Economic Consequence

The governance token with 500,000 registered holders, a 0.3% participation rate, and a treasury that has never executed a proposal is not a failure of community engagement. It is a failure of design.

Governance token holders do not vote when governance does not control anything that matters economically. If the fee switch is off, the treasury is symbolic, and governance proposals are non-binding, then governance participation is a volunteer activity with no personal economic stake. The participation rate reflects the design, not the community's commitment.

Governance should control the economic levers of the protocol. Fee structure. Treasury deployment. Revenue routing to holders versus reinvestment. Staking parameters. These are decisions with real dollar outcomes attached to them. When governance tokens control those decisions, governance token holders have a reason to care, to study proposals, to vote, and to hold the token to preserve their governance position.

Most projects make the mistake of treating governance as a feature to add after the mechanism design is complete. That doesn't work. Governance needs to be designed at the same time as the economic architecture, because governance is the economic architecture's control system. Build it that way.

The most defensible governance designs we have seen start with this question: what are the five most economically consequential decisions this protocol will make in the next two years? Those decisions are the scope of governance. The token structure is then designed to incentivize participation in exactly those decisions, not in symbolic ones.

If your protocol's answer to that question is "we're not sure yet," governance design should wait until the answer is clear. Governance tokens issued before governance scope is defined almost always end up controlling nothing that matters. The market prices that correctly, and the project discovers why governance token valuation is poor after the fact.

#Mistake 6: No Compliance Architecture at the Design Stage

The token design is finalized. The community is excited. The exchange listing conversation has started. Then the exchange's counsel asks for a legal opinion, and the team discovers for the first time that their token's design looks like a revenue-sharing instrument under the SEC's Howey test analysis.

This is not theoretical risk. We have seen it happen. The cost is not just the legal fees to restructure. It is the delay at the worst possible moment in the launch calendar, the community confidence hit when the TGE timeline slips, and in some cases a redesign that changes the utility mechanics that were already publicly announced.

Compliance is the architecture, not a feature. In the post-Coinbase enforcement environment, after the Tornado Cash OFAC sanctions, with FIT-21 digital asset legislation reshaping the U.S. framework, token designs that were acceptable three years ago carry different risk profiles today. The post-enforcement era is the operating context for every token launch. Content that doesn't acknowledge it is content that doesn't reflect where the market actually is.

Token classification comes first. Before the vesting schedule. Before the allocation table. Before the emission model. Get the legal opinion from counsel experienced in digital assets, in the jurisdictions where the token will be offered, and build the mechanism design around the compliance architecture they establish. Compliance isn't something you bolt on after mechanism design. It's the foundation that determines which mechanisms are even possible.

What that looks like in practice: the legal review covers the token's structure under the Howey test analysis and, depending on target markets, under MiCA (Markets in Crypto-Assets) and Singapore's MAS framework. The review produces a token classification and a set of design constraints. Revenue-sharing mechanics may be restricted. Transfer restrictions may be required. Accreditation verification may be a precondition for certain holder categories. The mechanism designer works inside those constraints, not around them.

Projects that skip this step are not saving time. They are borrowing it. The bill arrives at listing, at exchange legal review, or at a regulatory inquiry, when the cost of restructuring is measured in months and community trust, not in legal fees.

#Mistake 7: Ignoring the Post-TGE Maintenance Requirement

The tokenomics paper is version 1.0. It ships at TGE. The team moves on to product. By month 18, the vesting assumptions are no longer accurate because a key contributor left and forfeited tokens outside the original model. The treasury multi-sig quorum hasn't met in six months. The governance participation rate is 0.1%. The emission schedule is running as designed, but the demand assumptions it was built on have changed.

Tokenomics is a living system. The model is not the reality. The model is a starting estimate. The reality is whatever the on-chain data shows at any given point, and that data needs to be compared against the model on a schedule.

Quarterly review covers four things. Circulating supply versus model, to catch deviations early. Treasury runway versus spend rate, to understand how long the protocol can operate without external capital. Governance participation rate versus baseline, to catch disengagement before it becomes a structural failure. Emission rate versus liquidity depth, to catch the vesting cliff problem in Mistake 3 before it becomes a live event.

Projects that treat tokenomics as done at TGE are running a business with a financial model they built before they had any customers. That would be unusual in any other context. It is standard in crypto. It should not be.

The quarterly review cadence also serves a second function. It creates a paper trail. Institutional investors doing secondary market due diligence look for evidence that the team has been actively managing the token model, not just watching it. Meeting notes from governance discussions, treasury reporting, and circulating supply updates all signal that the team treats tokenomics as an ongoing operational discipline. Teams that have this documentation move faster in secondary processes. Teams that don't are explaining the absence.

#How to Audit Your Own Tokenomics for These Errors

The seven mistakes above are all detectable before TGE. The diagnostic is not complicated. Work through each error category with the following questions.

For Mistake 1: can the team write a one-paragraph description of the protocol's revenue mechanism, naming who pays, who receives payment, and how the token sits in that flow? If it takes more than one paragraph to answer, the revenue model is not clear enough to build a token on.

For Mistakes 2 and 3: model the daily unlock rate against the 30-day average daily volume at each cliff event. Run 10,000 Monte Carlo simulations. If the 10th-percentile scenario produces a daily unlock rate above 1% of average daily volume, the vesting parameters need adjustment before TGE.

For Mistake 4: for each utility function in the token design, write a two-sentence answer to this question: if a rational actor uses this utility today, what is their economic reason to hold the token tomorrow? If you cannot write a credible two-sentence answer, that utility does not create holding demand.

For Mistake 5: list the five most economically consequential decisions the protocol will make in the next two years. Verify that governance controls each of them directly, not symbolically. If governance controls none of them, governance token valuation has no anchor.

For Mistake 6: obtain a legal opinion from digital asset counsel before the vesting schedule is finalized. This is not optional in the current enforcement environment. If the opinion is already in hand, verify it covers the jurisdictions where the token will be offered.

For Mistake 7: build the quarterly review into the post-TGE operations plan before TGE. Set calendar invites. Assign ownership. The review does not happen by itself.

These six diagnostic passes take less time than the redesign they prevent.

#What Good Tokenomics Design Looks Like Instead

The seven mistakes above share a common root: designing the token as an independent system rather than as infrastructure for a business that creates real value. Good tokenomics design starts from the opposite direction.

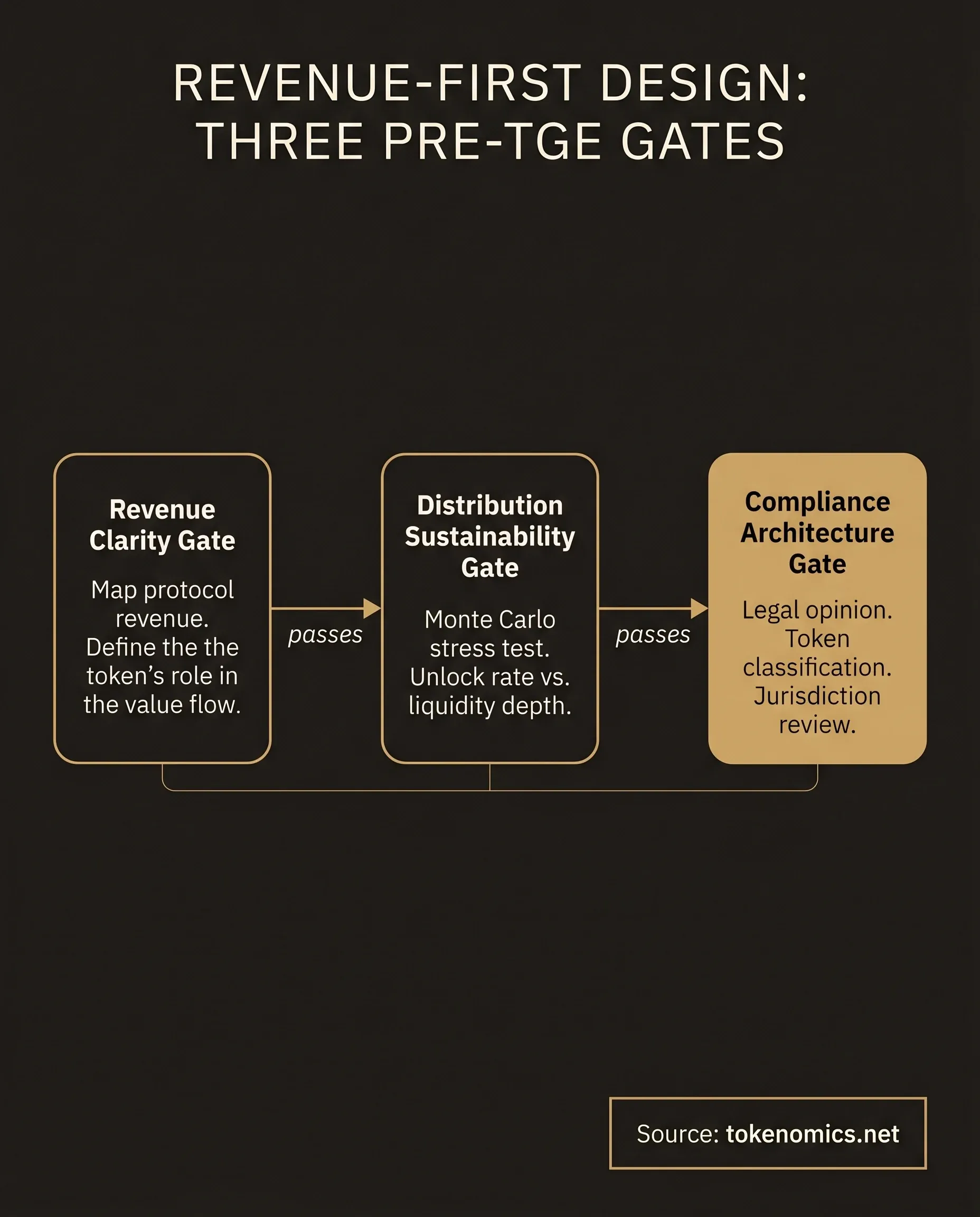

We use what we call the Revenue-First Design framework. Three design gates applied before any supply model or emission schedule is finalized.

Revenue clarity. The protocol's revenue mechanism is documented before token design begins. How does the business earn money? Who pays? What is the flow of value from payer to protocol? The token design must sit in that flow or serve a real function for participants in that flow.

Distribution sustainability. The allocation table is stress-tested against historical unlock absorption data for comparable protocols at similar liquidity depth. The vesting schedule is modeled under Monte Carlo simulations across liquidity scenarios. Distribution passes only when the unlock rate is within absorption capacity across the 10th-percentile liquidity scenario.

Compliance architecture. Token classification is resolved before mechanism design is finalized. Legal opinion from jurisdiction-appropriate counsel is in hand before the vesting schedule is locked. The mechanism is designed to be operable within the compliance parameters established by the legal review.

Get your house in order before you go to market. Projects that arrive at institutional investors, at exchange listing committees, or at regulatory review with these three gates clear move faster. Projects that don't spend the time after the fact, at higher cost, under worse conditions.

The three gates also function as a pre-flight checklist for the audit process. When we run a tokenomics audit engagement, these three areas are where we spend the most time, because they are where the seven structural errors originate. Revenue clarity catches Mistakes 1 and 4. Distribution sustainability catches Mistakes 2 and 3. Compliance architecture catches Mistake 6. Mistakes 5 and 7 are surfaced by a governance design review and a post-TGE operations assessment that run alongside the three gates. The same Revenue-First framework underpins our work on RWA tokenization design, where compliance architecture and revenue clarity are prerequisites before any supply modeling begins.

The result of a clean audit is not a certificate. It is documentation. The token design rationale, the Monte Carlo stress test outputs, the legal opinion, the allocation model with absorption projections. That documentation is what institutional capital requires before it writes a check or countersigns a listing agreement. Institutional capital requires institutional-grade documentation. That's what the complete data room delivers.

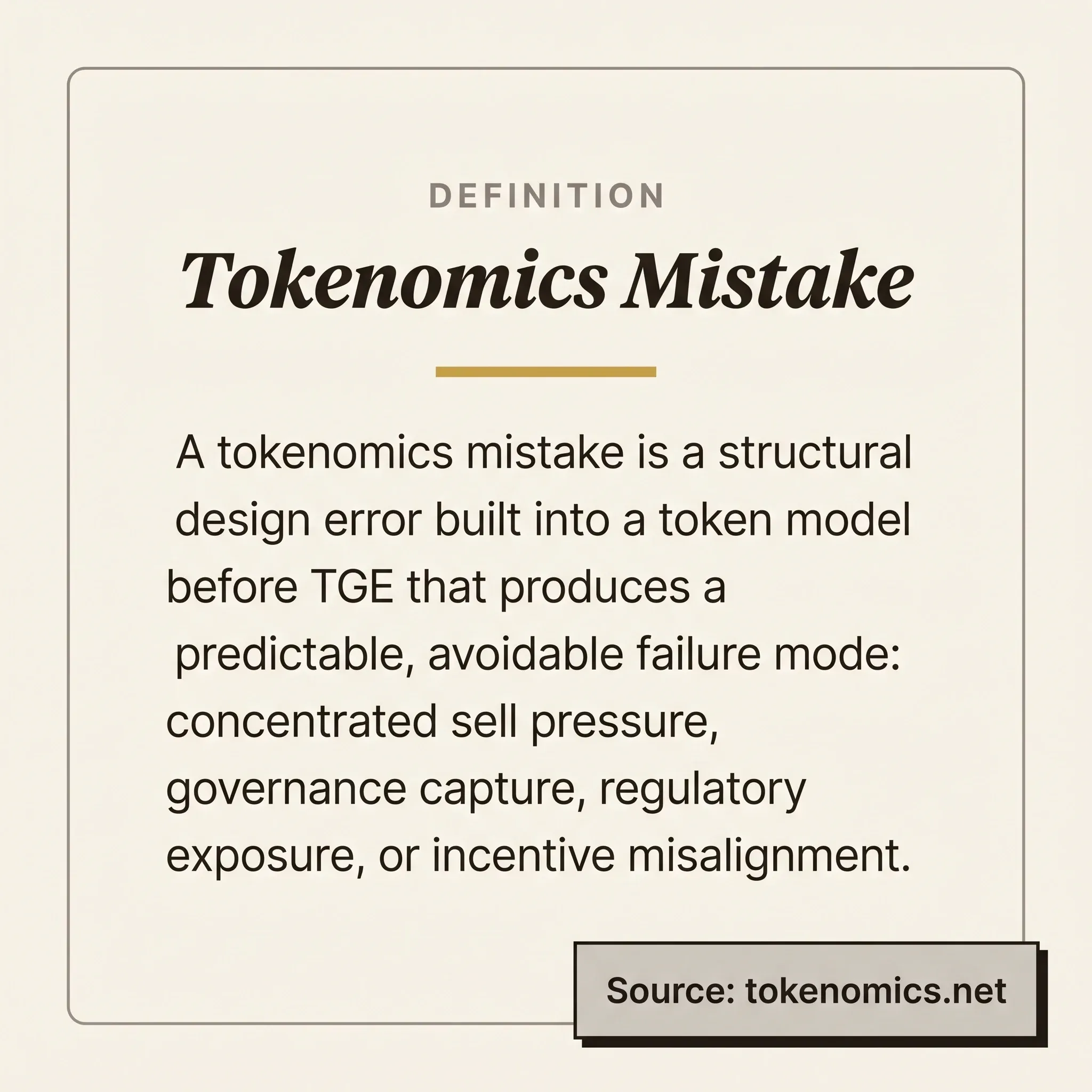

Definition: Tokenomics Mistake A tokenomics mistake is a structural design error built into a token model before TGE that produces a predictable, avoidable failure mode: concentrated sell pressure, governance capture, regulatory exposure, or incentive misalignment between founders, investors, and the community. Tokenomics mistakes are distinguishable from market volatility because they originate in design choices, not in external conditions.

#Frequently Asked Questions

#What are the most common tokenomics mistakes?

The seven structural errors we see most often across 80+ projects are: designing supply without a revenue model, allocation that front-loads insiders, vesting designed for optics rather than mechanics, token utility that doesn't create holding demand, governance without economic consequence, no compliance architecture at the design stage, and ignoring the post-TGE maintenance requirement. Each is a design-layer problem, not a market-conditions problem, and each is identifiable before TGE.

#Why do most tokenomics designs fail?

Most tokenomics designs fail because the token is treated as the product rather than as infrastructure for a business that generates real value. The design optimizes for the TGE narrative (supply caps, distribution tables, emission curves) without answering the foundational question: where does demand come from once the initial distribution is complete? Revenue comes first. Compliance comes second. Everything else follows.

#How do you fix bad tokenomics?

Three steps. First, diagnose the failure mode against the seven structural errors above. Most bad tokenomics have two or three of the errors present simultaneously; identifying which ones are active determines the order of remediation. Second, run Monte Carlo stress testing on the current supply model against real liquidity depth assumptions. This surfaces the vesting cliff problem and the token velocity problem in quantitative terms. Third, engage a legal opinion if token classification is unclear or was established before the current enforcement environment. Redesign around the compliance architecture the legal review establishes, not the other way around.

#What is the difference between tokenomics mistakes and market volatility?

Structural tokenomics mistakes are predictable and avoidable. They produce specific, identifiable failure modes at known points in the project lifecycle: the 12-month unlock cliff, the post-emission demand cliff, the listing committee's legal review. Market volatility is external; it accelerates or delays when these failure modes surface, but it doesn't create them. The distinction matters for founders because market volatility is outside your control. Tokenomics design is not.

#The Standard Has Risen

Institutional investors, exchange listing committees, and regulators are all looking more carefully than they were three years ago. The projects that arrive with the seven structural errors embedded in their model don't get a second meeting. The projects that arrive with Revenue-First Design documentation, compliant architecture, and a maintenance plan get a different conversation.

The audit process exists to find these errors before the market does.

If you're building onchain and need your tokenomics to hold up under institutional scrutiny, book a discovery call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.