TGE Strategy: A Step-by-Step Guide for Token Founders

A TGE strategy covers seven phases from token design to post-launch monitoring. This guide helps founders plan a token generation event that holds up.

Most founders treat the TGE as a launch date. It is not. It is the outcome of a multi-phase design, legal, and market-preparation process that starts months before any tokens hit a wallet, and continues for 90 days after.

A TGE strategy is a structured, pre-launch process that coordinates token design, legal classification, documentation, exchange setup, and community communication. Without that structure, the TGE date becomes a forcing function for rushed decisions that have real consequences: legal exposure, tokenomics designs that create predictable sell pressure, exchange listings that collapse within 24 hours, and investor relationships that sour at first unlock.

The token generation event is infrastructure for a business that must create real value. Without a revenue model underneath it, the TGE is a countdown timer. This post walks through a seven-phase framework for building TGE strategy from first principles.

If you want to understand what a tokenomics advisory engagement produces across the full launch lifecycle, what a tokenomics audit covers gives a clear picture of the diagnostic side of that work.

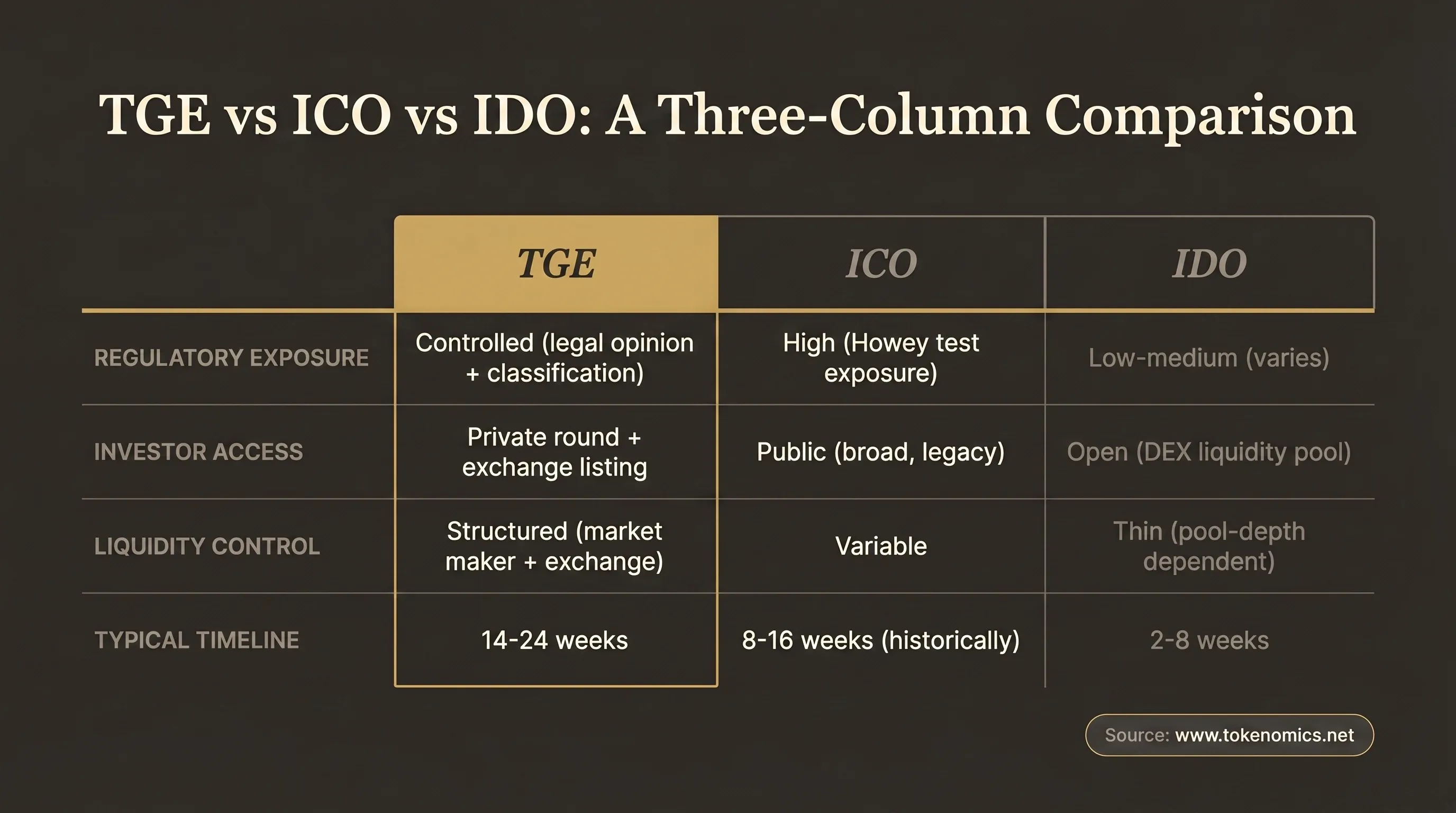

#What Is a TGE, and Why It Differs from an ICO or IDO?

A TGE (token generation event) is the moment tokens are created on-chain and distributed to initial holders. The technical event is simple: a smart contract executes, tokens are minted, and the initial distribution begins. The strategic scope around that event is where most of the work lives.

The term gets conflated with two related but distinct mechanisms:

ICO (Initial Coin Offering): The dominant fundraising format in 2017 and 2018. The project published a whitepaper, accepted BTC or ETH from the public, and issued tokens in return. The SEC's 2018 enforcement wave, using the Howey test to characterize many ICO tokens as unregistered securities, made pure public ICOs a legal liability in most jurisdictions. ICO-style mechanics still exist in private form (SAFT rounds, accredited-investor sales), but the broad public ICO is largely gone for legally-aware projects.

IDO (Initial DEX Offering): A DEX-native launch where the project lists directly on a decentralized exchange with a liquidity pool. Lower compliance overhead, but the tradeoffs are real: thin initial liquidity, high day-one price volatility, susceptibility to MEV bots, and limited control over who holds the token at launch. The IDO format persists for early-stage and community-native projects; institutional-grade launches typically pair a private round with a CEX listing.

TGE in current usage refers to the full distribution event: a combination of private round (SAFT or Token Purchase Agreement), exchange listing (CEX or DEX), and community distribution, rather than any single mechanism. The TGE is the moment the public token supply begins circulating.

The choice between these formats is a legal and market-structure decision before it is a technical one. The Howey test analysis, MiCA classification, the target exchange's listing requirements, and the geographic scope of the raise all constrain the mechanism before you design it. For context on how token distribution decisions fit within the broader design process, see our guide to token distribution model design.

#The Seven Phases of a TGE Strategy

We use what we call the Seven-Phase TGE Framework. It sequences the work in the order dependencies actually run: legal opinion before model finalization, model finalization before documentation, documentation before outreach, outreach before the exchange.

Most TGE failures we see trace back to one of two problems: phases executed in the wrong order, or phases skipped entirely. The seven-phase structure exists to make those dependency violations visible before they become launch-day crises.

Phase 1: Token Design and Supply Architecture

Define total supply, distribution allocation, vesting schedules, emission schedule, and incentive mechanics. This phase produces the token model: the quantitative design the legal team reviews, the documentation team documents, and the exchange's listing team evaluates. It must be grounded in the business's revenue model and capital requirements, not copied from an industry template.

Outputs: token model document, allocation table, vesting schedule, emission projections.

Phase 2: Legal Classification and Opinion

Commission a legal opinion from counsel with relevant token experience. The opinion analyzes the token against the Howey test (for US regulatory posture), MiCA classification (for EU regulatory posture), and applicable local-law frameworks. It answers the foundational question: is this token a security, a utility token, or something else, and what does that classification require?

This phase gates every downstream step. The token's classification determines what investor documentation you need, what KYC/AML infrastructure your exchange requires, and what community communication you can and cannot make.

Outputs: legal opinion letter, jurisdiction analysis, recommended token structure.

Phase 3: Exchange and Listing Strategy

Identify target exchanges, understand their listing requirements and timelines, select a market maker, and design the initial liquidity structure. A major CEX listing requires 3 to 6 months of preparation minimum. Set this phase early enough that the exchange timeline does not compress the upstream phases.

Outputs: exchange target list, listing timeline, market-maker term sheet, initial liquidity design.

Phase 4: Documentation Package

Build the full documentation set: tokenomics data room, investor deck tokenomics section, Token Purchase Agreement (or SAFT for pre-TGE private rounds), developer tokenomics specification, and a community-facing tokenomics summary. Each document serves a different audience with different needs.

Outputs: complete tokenomics data room, investor documentation, developer specification, community summary.

Phase 5: Investor and Community Positioning

Develop the narrative for each audience separately. The investor narrative leads with mechanism design, revenue model, and distribution structure. The community narrative leads with utility and participation mechanics. These are different documents with different frames; blending them produces a document that neither audience trusts.

Outputs: investor tokenomics narrative, community tokenomics narrative, communication calendar.

Phase 6: Launch Execution

Coordinate the smart contract audit, multi-sig key management, exchange listing, launch-day treasury deployment, and price-discovery window management. This phase has the highest coordination overhead and the narrowest margin for error. Under-resourcing it is the most common source of preventable launch-day crises.

Outputs: audit report, multi-sig setup, launch execution checklist, initial treasury deployment record.

Phase 7: Post-Launch Monitoring

Execute a 30/60/90-day distribution health monitoring program. Track concentration metrics (top-wallet percentages), velocity (token turnover rate), treasury deployment against plan, and community growth against projection. Projects that treat the TGE date as the end of the process regularly face predictable crises at the month-3 cliff when the first vesting events begin.

Outputs: 90-day monitoring plan, distribution health reports, cliff-event management protocol.

#Token Design as TGE Strategy: The Revenue-First Constraint

Most TGE guides frame token design as a question of allocation percentages and vesting schedules. Those are the outputs of token design. The inputs are: what the business produces, who captures value from it, and what the token's role in that value flow is.

A token model designed without a real revenue engine underneath it is a countdown timer.

Supply architecture (total supply, emission schedule, circulating supply curve) determines the token's FDV on day one and the sell pressure in months 2 through 18. These figures must be set with a revenue projection and a liquidity depth target as inputs. Setting total supply at a round number without that grounding produces a FDV that has no relationship to what the business can actually support.

Industry allocation norms (team 15 to 20 percent, investors 20 to 25 percent, treasury 15 to 25 percent, community and ecosystem 30 to 40 percent-plus) are starting points, not specifications. The actual split should reflect the business's capital requirements and the incentive design's functional needs. A treasury allocation calibrated to the business's 24-month operating runway is worth more to the token model than one that matches the median allocation in a comp-set of peer projects.

Vesting design is where most projects make the most visible errors. A 12-month cliff on team allocation is the post-2022 institutional expectation baseline. Eighteen to 24 months is what we see institutional investors request in term sheets today. If the team's cliff aligns with the exchange listing date, every institutional investor who reviews the cap table can see that. Whether it signals confidence or concern depends on the context, but the alignment is always noticed.

#The Legal Opinion Gate

The legal opinion is not insurance paperwork. It determines the token's infrastructure requirements for every phase that follows.

The opinion answers one foundational question: does this token design qualify as a security under the applicable regulatory frameworks? In the US, that analysis runs against the Howey test: investment of money, in a common enterprise, with an expectation of profits, from the efforts of others. In the EU, it runs against MiCA's classification schema: utility token, asset-referenced token, or e-money token. In Singapore, Hong Kong, the UAE, and most other jurisdictions, there are equivalent frameworks, each with different thresholds and consequences.

The token's classification determines what comes next. A utility token and a security token require entirely different exchange infrastructure, investor documentation, KYC/AML requirements, and community communication constraints. Running Phase 4 (documentation) before Phase 2 (legal opinion) means building the wrong documentation set and rebuilding it after the opinion arrives, at significant cost.

Compliance isn't something you bolt on after mechanism design. It's the foundation that determines which mechanisms are even possible.

What a legal opinion actually contains: analysis of the token against the applicable test, jurisdiction-specific classification recommendations, a summary of what regulatory registrations or exemptions apply, and guidance on what the token cannot do in each jurisdiction without triggering registration requirements.

Where to get one: token legal counsel with protocol-specific experience, not general corporate counsel. The firms doing this work in 2026 specialize in digital assets; general counsel who "also does crypto" is not the same engagement.

A note: whether your token is a security depends on the specific facts of your design and the jurisdiction of analysis. This framework describes the analysis process; it does not constitute legal advice. Get the legal opinion.

For more on how regulatory design affects tokenomics structure, see our post on tokenomics compliance.

#Exchange and Liquidity Strategy

Exchange and liquidity design is frequently treated as a late-stage logistics task. It belongs in Phase 3, not Phase 6, because the exchange's requirements and timelines shape how much time you have for every upstream phase.

A major CEX listing requires 3 to 6 months of preparation from the point of initial contact. The listing process includes due diligence on the project, technical review of the smart contract, tokenomics documentation review, and legal review. Projects that assume they can complete an exchange listing in 8 weeks regularly discover that assumption at month 6 of a 10-month launch plan.

CEX versus DEX: both are viable depending on the project's stage and token classification. A CEX listing provides institutional access and deeper liquidity but requires more preparation time and compliance infrastructure. A DEX launch is faster and requires less compliance overhead, but the initial price action is harder to manage: the typical DEX listing sees 60 to 80 percent price decline in the first 24 hours unless the listing price, initial circulating supply, and liquidity pool depth are sized as a coherent system.

Market-maker selection: the initial liquidity provider sets the market structure at launch. Market-maker agreements are financial relationships with real costs and real risk profiles. A poorly structured agreement (particularly one that gives the market maker wide discretion on inventory management) can create artificial price stability that gives way at predictable intervals. Review the terms carefully; this is one of the highest-leverage decisions in the launch process.

Setting the initial circulating supply is the most consequential supply architecture decision for day-one price action. The FDV at launch should be defensible against the business's actual stage and the comparable stage FDVs of peer projects. CryptoRank token market data provides historical FDV-to-circulating-supply ratios across comparable launches, which is useful for calibrating your own numbers. A FDV of $500MM at token launch for a project with $50K of monthly protocol revenue is not defensible. Investors who do the math will.

#Documentation and Investor Communication

The documentation layer is what investors, exchanges, legal teams, and regulators actually read. Every phase of the TGE generates a different document for a different audience.

The core documentation set for a TGE:

Legal opinion letter. The foundational document. Everything downstream depends on this one.

Tokenomics data room. The complete investor-grade documentation package: supply architecture, allocation table with vesting schedule, financial model (revenue projections, treasury runway, emission schedule), mechanism design specification, governance structure, and supporting legal and audit references. The whitepaper era is over. The data room era is here. Institutional investors expect a complete tokenomics data room with sourced claims, modeled projections, and audited references.

Investor deck tokenomics section. A distilled version of the data room designed for a 3 to 5 slide narrative. Not a replacement for the data room, but a summary that directs serious investors to the data room for depth.

Token Purchase Agreement or SAFT. The legal instrument governing pre-TGE private rounds. The appropriate instrument depends on the token's legal classification and jurisdiction. Get this from counsel, not from a template.

Developer tokenomics specification. The technical implementation reference for the engineering team. Separate from the investor documentation; written for developers, not investors.

Community-facing tokenomics summary. A plain-language summary of how the token works and what participants can do with it. This document leads with utility and participation, not FDV and allocation percentages.

The investor narrative and the community narrative serve different audiences. Most projects make the mistake of writing one document for both. That doesn't work. Investors need depth that would lose a community member. Community members need accessibility that would feel thin to an institutional investor. Write them separately.

Understanding what a complete documentation engagement requires is covered in our tokenomics audit checklist.

#Common TGE Strategy Mistakes and What They Cost

After advising 80+ projects through token launches and pre-launch planning, the failure patterns are predictable.

Starting with the exchange date, not the design. A CEX window arrives, the team accepts it, and suddenly a 14-week process has been compressed into 6 weeks. The documentation shows the rush. Investors read the documentation. The fix is to set your exchange timeline as a constraint that phases upstream work, not as the event that triggers it.

Treating the legal opinion as optional. This is not a compliance formality. The token's legal classification determines its exchange requirements, its investor documentation, and its community communication constraints. Projects that skip the legal opinion and discover the gap at Phase 4 face a documentation retrofit that takes longer and costs more than the original opinion.

Allocating by template, not by model. Copying a 20/20/20/40 allocation split from a peer project without running it against your business's capital requirements and incentive design produces a tokenomics model that looks standard but may create predictable problems. Industry norms are a starting point. The allocation table should be derived from the model.

Under-resourcing launch execution. Phase 6 is a multi-team coordination event: smart contract audit, multi-sig key management, exchange listing coordination, community communication, and price-discovery management all happen in a compressed window. Under-resourcing this phase produces preventable launch-day failures that are visible to the entire market.

No post-launch monitoring plan. The TGE date is not the end of the strategy. The first vesting cliff (typically at month 12 for team allocation) is the next high-risk event. Projects with no distribution health monitoring in place regularly face concentration or velocity problems at month 3 or month 12 that could have been anticipated from the launch-day data.

#The Regulatory Context for TGE Strategy in 2026

The regulatory environment for token generation events in 2026 is the most consequential design constraint in the process. Three frameworks shape the planning for any project with US or EU market exposure.

FIT-21 (US). The FIT-21 digital asset legislation passed the US House in May 2024. As of mid-2026, it is under Senate consideration in amended form. If enacted in its current framework, FIT-21 would provide a statutory distinction between digital commodities (subject to CFTC oversight) and digital securities (subject to SEC oversight), giving projects a clearer classification pathway than the current SEC-enforcement-led approach. The law is not final. Design to current applicable law. The Howey test analysis remains the operative framework for US token classification until FIT-21 passes and implementing regulations are issued. In our view, the most likely near-term outcome is a narrower version of FIT-21 that preserves SEC authority over tokens with profit-sharing or revenue-distribution mechanics.

Post-Coinbase enforcement landscape. The SEC's lawsuit against Coinbase, filed in June 2023, characterized multiple listed tokens as unregistered securities. While the case proceeds through the courts, the practical consequence has been to increase CEX compliance requirements on token listings: major exchanges now require more thorough tokenomics documentation review, more explicit legal classification analysis, and in some cases legal opinion letters before listing. This is a design-time constraint, not a post-launch discovery.

MiCA (EU). MiCA Phase 2 (covering asset-referenced tokens and e-money tokens) became applicable in December 2024. Utility token provisions under Title IV apply from June 2026. Q2 to Q3 2026 is the peak compliance window for EU-targeting projects. A TGE with EU investor participation, EU exchange listing, or EU community distribution must classify the token under MiCA and ensure the appropriate CASP (crypto-asset service provider) licensing or exemption is in place. The practical design implication: utility token classification under MiCA requires that the token have no profit-sharing or investment-return characteristics. Governance mechanics, fee discounts, and access-gating utilities are the MiCA-safe design patterns.

The regulatory context is not a post-design consideration. Which exchange will list your token, which investors you can accept, and what documentation you are required to produce are all downstream of your token's regulatory classification. Design with the legal opinion in hand.

#How Tokenomics Consulting Fits Into TGE Strategy

The Seven-Phase TGE Framework above represents the full scope of work a launch requires. Tokenomics consulting concentrates its value in four of those phases: Phase 1 (token design), Phase 2 (support and integration, not the legal opinion itself), Phase 4 (documentation), and Phase 7 (post-launch monitoring framework).

What a tokenomics consultant does: design the token model that the legal team reviews, build the documentation package that institutional investors examine, stress-test the distribution and vesting design against the business's revenue model and capital requirements, and establish the monitoring framework the team uses post-launch.

What a tokenomics consultant does not do: provide the legal opinion (that is legal counsel), conduct the smart contract audit (that is a security audit firm), or manage the exchange listing process (that is the project's business development function and, typically, a listing agent).

The most expensive tokenomics consulting engagements are retrofits. A project designed its own token model, launched, ran into distribution concentration problems or a regulatory question it did not anticipate, and engaged a consultant to help restructure a live token. The retrofit engagement is 3 to 5 times more expensive than a pre-launch design engagement, and the outcomes are more constrained: you are working with an existing on-chain structure rather than designing from first principles.

The optimal engagement point is before Phase 1. The project has a clear product and revenue model; the token's role in that model is being defined. At that stage, the design work integrates cleanly with every downstream phase.

The firm's revenue-first qualification applies here: we work with projects that have a real revenue model underneath the token. If the token is the product (meaning the project's value creation depends on token price appreciation rather than on an underlying business generating real revenue), that is not a fit for a tokenomics consulting engagement. We'll tell you that on the first call.

See what a tokenomics audit entails for more detail on how the diagnostic side of the advisory scope works in practice.

#Key Takeaways: TGE Strategy

- A TGE (token generation event) is the moment tokens are created on-chain and distributed. It is distinct from an ICO (public fundraising mechanism) and an IDO (DEX-native launch).

- A complete TGE strategy covers seven phases: token design, legal opinion, exchange and listing strategy, documentation, investor and community positioning, launch execution, and post-launch monitoring.

- The legal opinion is the gating item. It determines token classification (security vs. utility), which shapes every phase that follows: exchange requirements, investor documentation, KYC/AML infrastructure.

- Token design must start from the business's revenue model. Supply architecture, allocation split, and vesting schedules should be derived from the business's capital requirements and incentive design, not copied from templates.

- The Howey test (US) and MiCA classification (EU) are the two primary regulatory frameworks that shape TGE structure for projects with US or EU exposure.

- Major CEX listings require 3 to 6 months of preparation. Setting the TGE date before exchange requirements are understood compresses upstream phases.

- The most expensive tokenomics work is a retrofit. Projects that engage advisors before Phase 1 (token design) pay 3 to 5 times less than projects that retrofit after launch.

#Frequently Asked Questions: TGE Strategy

#What is a TGE strategy?

A TGE strategy is the structured multi-phase plan that coordinates all the work required before, during, and after a token generation event. It covers token design, legal classification, exchange and listing preparation, documentation, investor and community communication, launch execution, and post-launch monitoring. A TGE strategy is not just a launch date and a checklist: it is a sequenced process where each phase depends on the phase before it.

#What is the difference between a TGE, an ICO, and an IDO?

A TGE (token generation event) is the on-chain event where tokens are minted and distributed. An ICO (initial coin offering) was the 2017-2018 public fundraising format where the project accepted ETH or BTC in exchange for tokens. The SEC's enforcement wave using the Howey test made broad public ICOs a legal liability in most jurisdictions. An IDO (initial DEX offering) is a DEX-native launch where tokens list directly on a decentralized exchange via a liquidity pool. In 2026, most institutional-grade launches use a TGE that combines a private round (SAFT or Token Purchase Agreement) with a CEX or DEX listing, rather than a broad public offering.

#How long does it take to prepare for a TGE?

A complete TGE preparation timeline is typically 14 to 24 weeks for a project starting from a defined business model. The critical path runs through: token design (2 to 4 weeks), legal opinion (3 to 6 weeks), exchange listing preparation (3 to 6 months for major CEX), and documentation (4 to 6 weeks). These phases overlap but cannot be fully parallelized because the legal opinion gates the documentation and the exchange listing gates the launch date. Teams that begin preparation 8 weeks before their target TGE date are working with a compressed timeline on every phase.

#What documents are required for a TGE?

The core documentation set for a TGE includes: a legal opinion letter (token classification analysis), a tokenomics data room (supply architecture, allocation table, vesting schedule, financial model, mechanism specification), a Token Purchase Agreement or SAFT (for pre-TGE private rounds), an investor deck tokenomics section, a developer tokenomics specification, and a community-facing tokenomics summary. The legal opinion is the foundational document; the data room is the investor-grade reference package that exchanges and institutional investors review.

#What is the Howey test and why does it matter for a TGE?

The Howey test is the US Supreme Court's four-part test for determining whether an asset is a security: investment of money, in a common enterprise, with an expectation of profits, from the efforts of others. It is the primary framework the SEC uses to evaluate whether a token is an unregistered security. A token that satisfies all four prongs is likely a security and must be registered or sold under an exemption (Reg D, Reg S, Reg A+). The Howey test analysis is the central question in the legal opinion that gates every downstream TGE phase. Projects with EU exposure also require a MiCA classification analysis alongside the Howey analysis.

#When should a founder hire tokenomics consulting support for a TGE?

The optimal engagement point is before Phase 1 (token design) begins. At that stage, a tokenomics consultant can design a token model from first principles that integrates with the business's revenue model, calibrate the supply architecture and vesting design before the legal team reviews it, and build the documentation package that institutional investors will examine. The alternative is a retrofit engagement: commissioned after the token has launched and problems have emerged. Retrofit engagements are 3 to 5 times more expensive and produce more constrained outcomes because they work with an existing on-chain structure rather than designing from scratch.

#What a Fully Executed TGE Strategy Produces

The seven phases produce a launch that has been designed, not assembled. The token model integrates with the business's revenue model. The legal opinion determines the infrastructure. The documentation package serves each audience correctly. The exchange listing is prepared, not rushed. The post-launch monitoring program starts on day one.

The founders who execute TGEs well have one thing in common: they start the process early enough that no phase is compressed by the phase before it. Three to six months before the target TGE date is the correct window to begin Phase 1 and commission the legal opinion. Teams that begin the process 8 weeks before the TGE date are, in most cases, launching with compressed documentation, an incomplete legal opinion, and a distribution design that has not been stress-tested.

Get your house in order before you go to market. The TGE date is when the market starts watching. The work that earns institutional confidence happens before that date.

If you're building onchain and need your TGE strategy to hold up under investor and regulatory scrutiny, book a discovery call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.