Token Vesting Design: Schedules for Team, Investors, and Advisors

Token vesting design: cliff and linear schedules for team, investors, and advisors that control sell pressure and pass investor diligence.

Token vesting design is the process of structuring the schedule by which allocated tokens become transferable, defining the cliff period before any tokens release and the cadence of linear releases afterward. For each stakeholder group (team, investors, and advisors), the schedule should reflect that group's relationship with the business and its accountability for ongoing contribution.

Most founders treat vesting as a legal formality. That's the wrong frame. Vesting is your primary tool for managing circulating supply growth and the sell pressure that comes with it. Get the schedules right and your token's market structure has room to build alongside the underlying business. Get them wrong and every unlock event becomes a capital markets problem.

Token vesting design: the process of structuring cliff periods and linear-release schedules that govern when each stakeholder group's token allocation becomes transferable.

#What Token Vesting Actually Does (and Why Getting It Wrong Is Expensive)

Token vesting design controls how quickly your circulating supply grows after TGE. Every allocation bucket (team, investors, advisors, treasury, community) has its own release schedule, and the interaction of those schedules determines how much supply hits the market at any given time.

The mechanics are straightforward: a cliff defines the minimum lock-up period before any tokens release. After the cliff, tokens release linearly, typically monthly or quarterly, until the full allocation vests. A four-year vest with a one-year cliff means the first tokens release at month twelve, then a portion releases each subsequent month through month forty-eight.

What happens when this is designed poorly? Concentrated unlock events. We've worked with founders who aligned team and investor cliffs on the same month. The result was a spike in circulating supply that coincided with a thinly traded market, exactly the conditions that compress price.

The business consequence is real. Institutional investors model vesting schedules before they commit capital. If your schedule shows a 30% circulating supply jump at month twelve because three stakeholder groups hit their cliffs simultaneously, that is a red flag in diligence, not a minor technical detail.

#The Three-Schedule Problem: Team, Investors, and Advisors Are Not the Same

Most projects make the mistake of applying a single vesting template to all stakeholder groups. That doesn't work.

Each group has a different relationship with the token and a different accountability structure. Team members have ongoing employment obligations. Investors provided capital at a specific FDV and have a contractual expectation about their liquidity window. Advisors contributed specific deliverables over a defined period and, in most cases, front-load their contribution in the first twelve months.

Applying a four-year team schedule to advisors is too generous for the contribution. Applying an investor schedule to team creates misaligned incentives around commitment. The schedules need to reflect the actual accountability structure of each group.

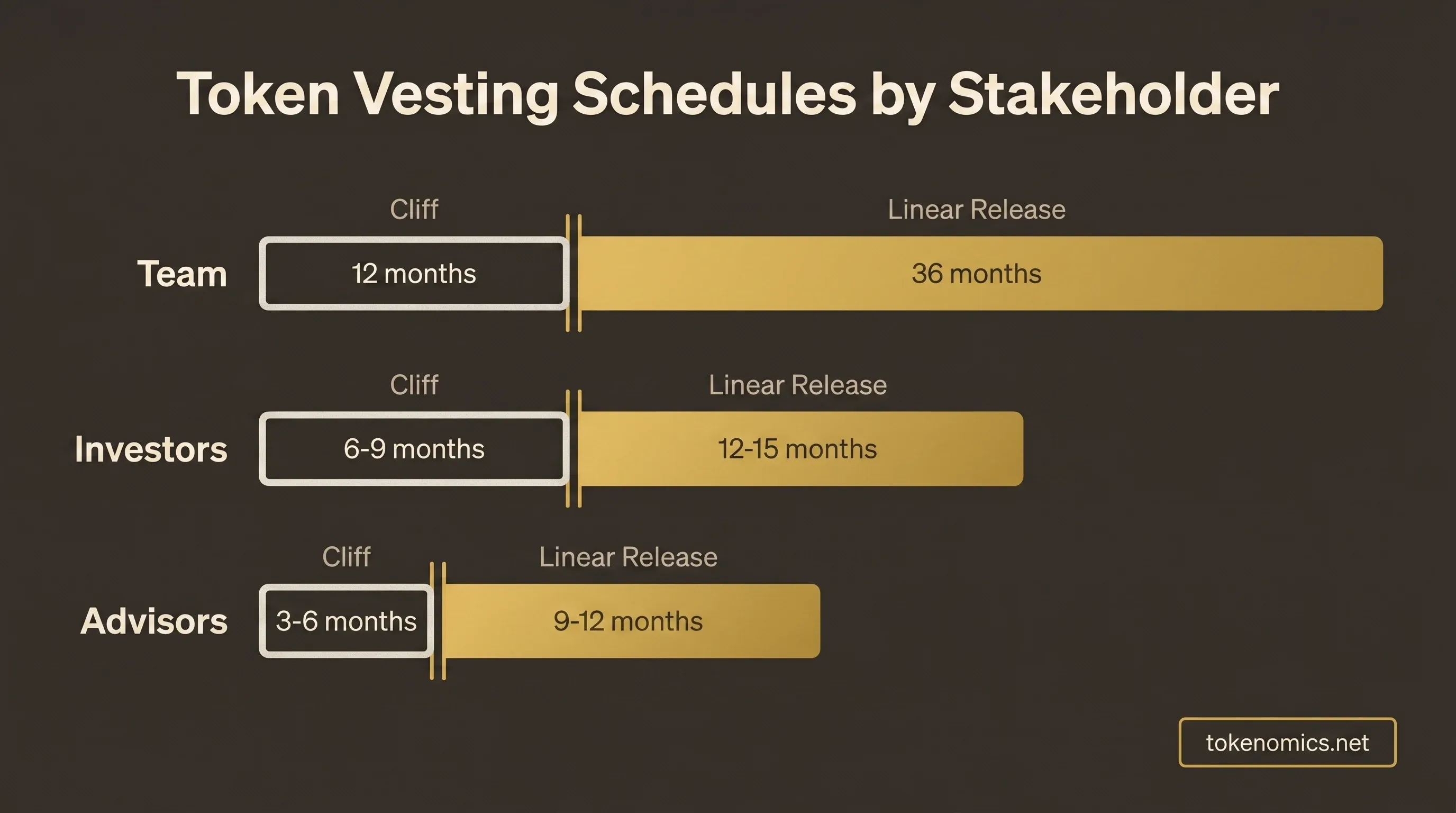

#Team Token Vesting: The Standard and Why It Exists

The industry benchmark for team vesting is four years with a one-year cliff. This structure is not arbitrary. It maps to the minimum period institutional investors expect to see founders committed to the project before they can exit their position.

The one-year cliff prevents the failure mode we see repeatedly across early-stage projects: a core team member who receives tokens, contributes for six months, and exits before launch. Without the cliff, that exit is clean. With a one-year cliff, they leave before any tokens vest.

After the cliff, monthly release is the most common structure. Quarterly is cleaner for accounting and payroll-style administration, but monthly is the default expectation for most institutional diligence checklists.

Founder vesting vs. early employee vesting. Founding teams often hold a pre-formation allocation distinct from their employment-grant allocation. The pre-formation tokens typically carry a separate lockup reflecting the founders' founding contribution. Employment-grant tokens vest alongside the broader team schedule. Keep these as separate allocations in your vesting contract and your documentation.

The signal function of team vesting matters beyond the mechanics. A founding team with a six-month cliff signals to every institutional investor reading your data room that the founders could be liquid before the project has had time to prove itself. We've seen projects lose term sheets over this. The standard is four years with a one-year cliff, and deviating downward requires a compelling explanation.

#Investor Token Vesting: Aligning Capital With Business Milestones

Investor vesting ranges more than team vesting and should. Seed-round investors who took the earliest risk often accept twelve to twenty-four month schedules. Strategic investors, who typically come in at higher valuations with strategic value beyond capital, often negotiate shorter schedules or higher TGE unlock percentages.

The TGE unlock percentage is where founders often make the first mistake. Giving seed investors 25% at TGE means 25% of your seed allocation hits the market on day one. That creates immediate sell pressure at the moment when your market structure is most fragile.

The pattern we see hold up best: 5-10% TGE unlock for seed-round investors, with the remainder releasing linearly over twelve to eighteen months after a six-to-nine month cliff. The TGE unlock gives investors a liquidity signal without creating an outright sell event.

Round-level differentiation matters. Seed investors, strategic investors, and public sale participants should not be on the same schedule. Strategic investors who are contractually contributing value (exchange relationships, ecosystem integrations) may warrant a shorter total vest in exchange for a demonstrably lower TGE unlock. Public sale investors typically receive shorter vests (six to twelve months) because they entered at higher prices and at lower information asymmetry.

The guardrail: whatever you put in your whitepaper or data room needs to match your on-chain vesting contract exactly. Inconsistency between the document and the contract is a diligence-fail and, depending on jurisdiction, a disclosure problem.

#Advisor Token Vesting: The Most Frequently Misdesigned Schedule

Advisors are typically 1-2% of total supply. The vesting design for that 1-2% matters more than the percentage.

The most common mistake: applying a four-year team schedule to advisors. We've seen this across dozens of projects, and it creates a predictable problem. Advisor contribution front-loads in the first six to twelve months. An advisor who was genuinely active in year one and then largely absent is still vesting in year four under a team-equivalent schedule. The incentive structure is misaligned.

The recommended structure: twelve to eighteen months total vest with a three-to-six month cliff. Shorter than team because advisor contribution front-loads. The cliff exists to prevent the "advisory board" name from vesting nothing while contributing nothing.

Milestone-based vesting is the alternative. Instead of time-based release, advisors vest against specific deliverables: introductions completed, integrations facilitated, governance participation. This is more defensible from an accountability perspective but operationally more complex. It requires legal documentation of what constitutes delivery of each milestone.

Here's what most founders miss: advisor vesting terms are negotiable, and sophisticated advisors expect them to be shorter than team terms. If an advisor pushes for a four-year vest, that is a signal they are optimizing for token accumulation, not contribution. Structure the schedule to reflect the contribution, not the desired accumulation.

#Cliff Design: Why the Timing of Your First Unlock Is a Capital Markets Event

The cliff date is public information. Any investor, analyst, or market participant who reads your whitepaper or on-chain vesting contract knows exactly when your first major unlock happens. That date gets modeled into expectation.

What creates problems is a cliff stack: multiple stakeholder groups hitting their cliffs in the same calendar month. Team at twelve months. Investor at twelve months. Advisor at three months extended by a nine-month delay. Three groups unlocking in month twelve means a significant circulating supply increase at a single point.

The pattern that works: stagger the cliffs by stakeholder type. Team cliff at twelve months. Investor cliff at six to nine months. Advisor cliff at three to six months. Each group's first unlock falls at a different time, distributing circulating supply growth across several windows rather than concentrating it.

This matters beyond optics. Sophisticated buyers and market makers look at vesting schedules before they commit liquidity to your token. A staggered cliff structure is a positive signal. A cliff stack is a known risk that sophisticated capital discounts.

One more consideration: if your TGE has a public sale component, the public sale tokens are typically fully unlocked at TGE. That creates an immediate circulating supply baseline. Your private-round cliff dates determine how quickly that baseline grows. Model the circulating supply month by month before you finalize the schedule.

#Smart Contract Implementation: Making the Schedule Match the Documentation

Vesting schedules have to be enforceable on-chain. The whitepaper claim and the contract must match exactly.

The parameters you need to specify for every allocation group before your developers write a single line of code: the cliff period (in seconds or block numbers), the total vesting duration, the release cadence (monthly vs. quarterly), and whether vesting is revocable for departing team members or irrevocable for investors.

Revocable vs. irrevocable is not a technical detail. Team vesting should be revocable so that unvested tokens return to treasury when someone leaves. Investor and advisor vesting is typically irrevocable once agreed. If your contract is set to irrevocable for team members and a co-founder exits in month three, you have no mechanism to recover their unvested allocation.

Standard implementations include Gnosis Safe paired with a custom vesting contract or third-party vesting platforms. Whichever you use, the contract address and the audit report need to appear in your data room documentation. The common failure mode: a well-designed vesting schedule specified in a whitepaper with no on-chain implementation reference. Institutional investors cannot verify what they cannot inspect.

#How Vesting Design Feeds Your Data Room and Investor Diligence

Every institutional investor reviews vesting schedules as part of tokenomics diligence. This is not a backroom document. It is one of the first things a serious investor asks for after reviewing your token model overview.

What institutional-grade vesting documentation includes: a per-stakeholder schedule table with cliff dates, TGE unlock percentages, total allocation amounts, and vesting duration for each group. A month-by-month circulating supply projection derived from those schedules. Contract addresses and audit references for the on-chain implementation.

The circulating supply schedule is where most early-stage projects have a gap. The schedule quantifies exactly how much supply will exist at month one, month six, month twelve, and at full dilution. This is the document your legal team needs for the Token Legal Opinion, your development team needs for liquidity planning, and your finance team needs for treasury projections.

Vesting design is one component of a complete tokenomics data room. Every stakeholder group's schedule, the circulating supply projection, and the on-chain implementation documentation all need to be present and internally consistent for the data room to hold up under scrutiny.