Token Allocation Strategy Framework: Benchmark Ranges and Decision Criteria

Token allocation strategy explained: the four-bucket model, benchmark allocation percentages, and per-bucket decision criteria founders need before launch.

Token allocation strategy is the process of deciding how your total token supply is divided across the people and entities who hold it: team and advisors, investors, the protocol treasury, and the community. It also sets the terms, meaning the vesting schedule and unlock cliffs that govern when each group's tokens enter circulation. This post gives you the four-bucket framework, the benchmark percentage ranges, the decision criteria that should drive each bucket's size, and the failure patterns we see in data room reviews.

Every percentage you set is a permanent signal. Investors read team allocations as a commitment indicator. A community number that lands in a handful of wallets undercuts any decentralization argument you make later. A thin treasury caps how long the protocol can operate without raising again. Get the allocation wrong and no clever vesting schedule fixes it after launch, because allocation is the first thing that determines whether the underlying business has the runway to create value at all.

The four-bucket model is the spine. We will walk through benchmark ranges, the decision criteria per bucket, how the buckets interact as a system, and the mistakes that look reasonable on a slide and break in month 12. This is the design layer that sits above the broader token distribution model.

#What Is Token Allocation Strategy? The Four-Bucket Model

Token allocation strategy is not a spreadsheet exercise. It is a stakeholder design decision with legal, financial, and protocol-design consequences. The percentages you choose shape who controls governance, how long the treasury funds operations, and how investors read your alignment.

Token allocation strategy: the process of distributing a protocol's total token supply across Team and Advisors, Investors, Protocol Treasury, and Community and Ecosystem buckets, with explicit percentage targets and vesting parameters for each stakeholder group.

Token distribution model: the complete system governing how a protocol's token supply is allocated across stakeholder buckets, released over time through vesting schedules, and introduced into circulation via an unlock calendar spanning the full token lifecycle.

We use what we call the Four-Bucket Allocation Model. Four canonical buckets, each with a different job:

- Team and Advisors. Retention and alignment. This is the incentive that keeps the people building the protocol building it.

- Investors and Early Backers. Early-stage capital formation. This is what the project sold to fund the work.

- Protocol Treasury. Sustainability and operational runway. This is the protocol's working capital.

- Community and Ecosystem. Network adoption and the decentralization signal. This is the largest and most heterogeneous bucket.

Total has to equal 100%. The allocation game is zero-sum: every point you add to one bucket comes out of another. That constraint is the whole reason this needs a framework rather than a wish list.

Naming the buckets matters more than it looks. Vague categories like "partnerships," "reserve," or "future use" are a data room red flag. Investors read undifferentiated buckets as deferred dilution and hidden team allocation. There is also a fifth implicit bucket worth deciding on early: the public sale or TGE allocation. Many projects keep it separate from community because price discovery at launch is a distinct function from long-term ecosystem incentives. Decide whether you treat public sale as its own bucket or a sub-bucket of community before you set any other number.

#Benchmark Allocation Percentages: What the Data Shows

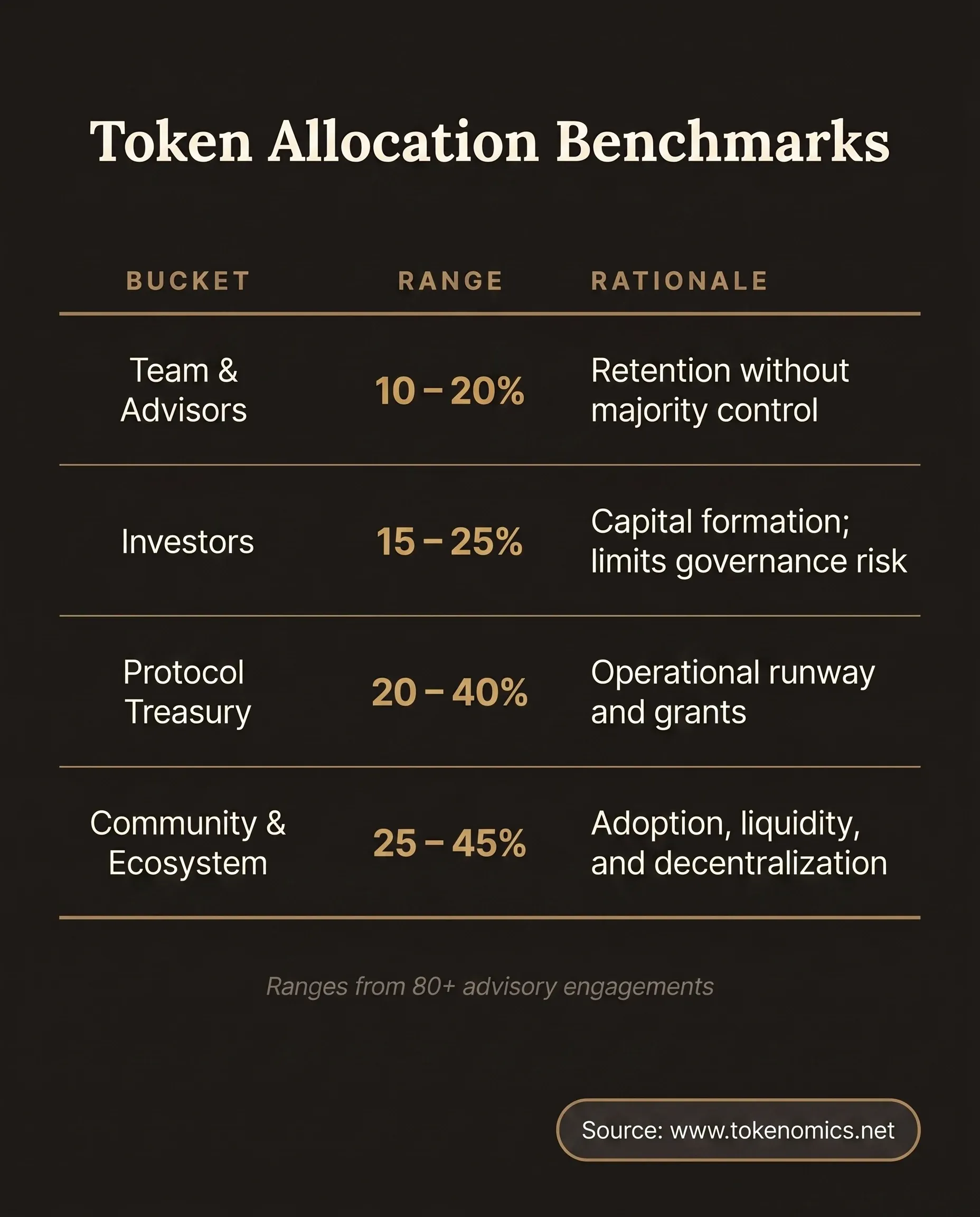

Benchmark ranges are not rules. They are the reference point from which a defensible deviation requires an explicit argument. Every project that moves significantly off these ranges should be able to document why. The ranges below come from pattern recognition across 80+ advisory engagements, cross-checked against public tokenomics data (Source: CryptoRank token market data) and onchain distribution dashboards (Source: Dune Analytics).

| Bucket | Typical Range | Rationale for Range |

|---|---|---|

| Team and Advisors | 10-20% | Retention incentive; meaningful skin-in-the-game without majority control |

| Investors (Seed + Series A) | 15-25% | Capital formation; concentration above 30% creates governance and liquidity risk |

| Protocol Treasury | 20-40% | Operational runway, grants program, protocol upgrades |

| Community and Ecosystem | 25-45% | Adoption, liquidity incentives, airdrops, grants, public sale |

The ranges are wide because stage matters. A pre-launch seed project with a three-person team needs more investor allocation to fund the build. A protocol at testnet with an active community sits in the middle. A protocol with product-market fit launching to an existing user base can push more into community because there are real users to distribute to. Same framework, different defensible numbers.

One thing these tokenomics allocation percentages are not: a way to size the treasury by subtraction. Treasury is not a savings account. It is operating capital. Size it from 24 to 36 months of runway at your expected burn rate, then fit the other buckets around it. We will come back to why treating treasury as the residual is one of the most common ways a token distribution model breaks.

the most common tokenomics design mistakes

#Team and Advisor Allocation: Decision Criteria

The primary decision variable for the team bucket is team size and tenure horizon. A three-person founding team with a ten-year vision needs a different allocation than a fifteen-person team on an eighteen-month roadmap. The per-person allocation should represent meaningful ownership without creating a perceived majority-control concentration that investors will flag.

Advisor allocation is the line item projects most often overallocate. The norm is 1-5% total for advisors, not 10% and up. Every point above 5% needs a documented, time-bound deliverable behind it. Advisors holding large allocations with no clear deliverables read as deferred team allocation in due diligence, and that costs you in the next round.

The vesting non-negotiable for team. Team tokens with no vesting, or a very short token vesting schedule under 12 months, are a counter-signal to investors. The standard is a 12-month cliff followed by linear monthly vesting over 36 to 48 months. Anything under four years total for a founding team gets scrutinized now. (Industry norm reference: Messari State of Crypto 2023; CoinList token vesting survey data.)

Token vesting schedule: a contractual timeline governing when allocated tokens become transferable, typically structured as a cliff period during which no tokens unlock followed by linear or milestone-based release over a defined duration measured in months.

Here's what most founders get wrong: allocating the entire team bucket to the founding team. Reserve 30-50% of the bucket for future hires and employee grants. Run out of team allocation in year two and you are choosing between dilutive re-allocation and losing the engineer or CMO you need. One signals an unstable cap table. The other costs you the hire.

One more check. Does the team bucket vest on time alone, or against protocol milestones? Time-only vesting aligns the team to the calendar. Milestone triggers, mainnet launch or a defined user or TVL threshold, add accountability without the legal complexity of conditional securities. Use them where the milestones are clean.

#Investor Allocation: Decision Criteria

The investor bucket usually spans multiple rounds, each with its own token price, valuation, and lockup expectation. Decide the total investor bucket size first, then sub-allocate across pre-seed, seed, and Series A. Working the other direction, summing round-by-round demand into whatever total it produces, is how projects drift past a defensible concentration.

The concentration problem is the reason the 15-25% benchmark exists. Investor buckets above 25-30% create two risks at once. Governance risk: if governance is token-weighted, large investors can block protocol upgrades. Liquidity risk: large investor unlock events drop concentrated sell pressure into the market on a known date. The benchmark balances capital access against both.

Vesting standard for investors. The market norm for seed investors is no cliff or a 3-6 month cliff with 12-18 months of linear vesting. Protocols seeking to demonstrate alignment increasingly negotiate longer lockups, a 12-month cliff with 24-month linear. Shorter than a 6-month linear with no cliff is a due diligence concern, because it signals investors who want out fast.

A note on documentation. Simple Agreements for Future Tokens (SAFTs) and token warrants are a common document structure for pre-TGE investor agreements. (SAFTs originated from the Cooley/Protocol Labs SAFT whitepaper, 2017; their enforceability varies by jurisdiction and remains an active area of securities law development.) They change when investor tokens vest relative to the TGE and how the allocation is recorded. Whether any specific structure is compliant in your jurisdiction is your legal team's call, not a tokenomics question. What the allocation model must do is account for the fully diluted SAFT and warrant conversion, not just the tokens already issued. Miss that and your real investor percentage is higher than your table says.

Watch the "strategic investor" trap. Projects routinely over-allocate to investors labeled strategic on the promise of ecosystem support that never materializes. Tie each strategic allocation to a specific commitment, an exchange listing, an integration, co-marketing, with a clawback if the commitment is not met inside a defined window.

what a tokenomics audit covers

#Protocol Treasury Allocation: Decision Criteria

Protocol Treasury: the share of token supply held by the protocol itself to fund operations, ecosystem development, and liquidity, governed by an explicit disbursement mechanism rather than distributed to any external stakeholder.

Treasury is the protocol's operational capital, and it should be sized from first principles, not from what is left over. Three inputs drive the number. Operational runway: 24 to 36 months of team costs, infrastructure, and audits at expected burn. Grants program target: the ecosystem development budget needed to hit your protocol milestones. Liquidity provisioning: what it takes to seed DEX liquidity at TGE.

Sub-categorize the treasury inside the allocation model. A single undifferentiated "treasury" bucket obscures purpose and invites misalignment. We recommend four sub-categories: Operational Reserve, Grants and Ecosystem Development, Liquidity Provisioning, and a Strategic Reserve held unallocated for opportunities. Each one then gets its own lockup logic.

The underallocation failure. Founders who size treasury as the residual, whatever is left after team, investors, and community, routinely end up unable to fund 12 months of operations. The treasury should be the first bucket sized, not the last. A protocol that runs out of treasury in year one is not community-owned. It is community-abandoned.

Two governance decisions sit on top of the number. First, who controls treasury spending. Early protocols often use a founding-team multisig; mature protocols move to DAO-governed disbursement. Document the mechanism in the allocation model. Second, treasury token lockups. Treasury tokens left unlocked from day one create a supply overhang. Lock them on a schedule tied to the operational sub-categories instead.

Some teams ask about deploying treasury tokens to earn yield through staking or DeFi protocols. That is a governance decision with real risk attached, smart contract exposure and potential regulatory characterization if yield is distributed to holders. It is not a default, and it is not something we recommend as a line item. Decide it deliberately or not at all.

#Community and Ecosystem Allocation: Decision Criteria

The community bucket is the largest, and it is not a single decision. It is four or five sub-decisions: public sale or TGE allocation, ecosystem grants and developer incentives, liquidity incentives, airdrop, and ongoing staking or protocol rewards. Treat each as its own line with its own logic.

The decentralization signal lives here. A community allocation that lands in a small number of wallets at launch undermines every decentralization argument the project makes later. Airdrop and distribution design should target Gini reduction explicitly. A 30% community allocation that lands in 100 wallets is not community distribution. It is investor-adjacent concentration with a different label, and a regulator or an exchange listing team will read it that way.

Emissions design versus one-time allocation. Community tokens that fund ongoing rewards need an emissions schedule, not just a percentage. The emissions rate determines sell pressure over time. A large community bucket on an aggressive emissions curve is more inflationary than a smaller bucket on a controlled one. The percentage tells you almost nothing without the curve.

Liquidity incentives are where the rule is sharpest: size for the TVL you need, not the TVL you want. Overallocate to liquidity mining and you get mercenary capital, TVL that spikes at launch and collapses when rewards dry up. Size the liquidity sub-bucket to sustain target TVL for 12 to 18 months, with a mechanism to adjust rewards against actual TVL.

Token supply distribution: the allocation of a protocol's total token supply across all stakeholder categories at a point in time, typically expressed as percentages of total supply and measured against the circulating supply to determine the fully diluted valuation multiple at launch.

One boundary. Token allocation strategy sets the airdrop bucket size. Airdrop design, eligibility, sybil resistance, cliff and vesting on the airdropped tokens, is a separate discipline. Do not conflate the two, and do not let the bucket size stand in for a distribution plan.

#Bucket Interaction Effects: The Allocation Is a System

Optimize one bucket in isolation and you create a problem in another. This is the section most allocation guides skip, and it is where the design work actually lives.

Team plus investor concentration creates control risk. If team holds 20% and investors hold 25%, that founding coalition controls 45% of supply. In a token-weighted governance system with no supermajority requirement, they can pass any proposal without community consent. That is a data room flag, and increasingly a flag in decentralization analysis. Whether any specific structure clears a given regulatory test is fact-specific and jurisdiction-specific; the point here is that the concentration is visible to anyone who adds the two buckets together.

Treasury versus community is a sustainability tradeoff. Moving percentage from treasury to community to strengthen a "community-owned" narrative reduces operational runway. The protocol that runs out of capital in year one to look more decentralized on launch day did not become community-owned. It became community-abandoned.

Community emissions collide with investor unlocks. If community rewards unlock in months 6 through 12 and the investor cliff clears at month 12, the cumulative sell pressure can overwhelm market depth on a single date. You only see this if you model the unlock calendar across all buckets at once.

The public sale sub-bucket then sets your circulating supply at launch, which sets initial market cap and the implied FDV multiple. Founders who minimize circulating supply at TGE to chase a high FDV build a structural unlock overhang into months 12 to 24. The design principle that ties this together: build the pro-forma unlock schedule across all four buckets before you finalize any single bucket percentage. The only correct unit of analysis for a token supply distribution is the full schedule across 48 to 60 months.

token allocation and vesting design

#Common Token Allocation Mistakes

After advising 80+ projects, the failure patterns are predictable. Five show up most.

1. Over-allocating to advisors with no deliverable requirements. Advisor allocations above 5% total with no documented, time-bound deliverables. Investors read it as deferred team allocation. The cost is due diligence friction and investor discounts at the next round.

2. Treating treasury as the residual bucket. Filling team, investors, and community first and accepting whatever is left as treasury. The result is undercapitalized operations inside 12 to 18 months of launch. The treasury should be the first bucket sized, not the last.

3. No reserve for future hires. Allocating 100% of the team bucket to the founding team. By month 18 the protocol needs to hire and has no token budget, which forces a re-allocation that signals to existing holders that the cap table is not stable.

4. Routing all of community through one emission program. Assigning 30% to community and pushing all of it through a single liquidity mining program. You get mercenary capital at launch, a TVL collapse when rewards taper, and zero capital left for grants or developer incentives.

5. Ignoring the unlock calendar across buckets. Modeling each bucket's vesting in isolation and never charting the aggregate. Months 12 to 18 is the most common danger window, where team, seed investor, and community unlocks converge into a supply shock the market's liquidity depth cannot absorb.

None of these are edge cases. They are the most common ways a reasonable-looking allocation becomes a structural problem at launch.

#Token Allocation Audit Checklist

Use this to audit an existing allocation or pressure-test a new one. Eight questions.

- Are all four buckets defined and labeled with explicit percentage targets, with no undifferentiated "reserve" or "future use" bucket?

- Does the team bucket reserve at least 30-50% for future hires?

- Does the advisor allocation have per-advisor deliverable documentation and a vesting schedule with a cliff?

- Is the treasury sized from operational runway first principles, not as a residual?

- Are the treasury sub-categories defined: Operational Reserve, Grants, Liquidity, Strategic Reserve?

- Does the community bucket have explicit sub-allocation across public sale, grants, liquidity rewards, and airdrop?

- Is the expected wallet distribution at TGE tracked, including a Gini read on concentration?

- Is the combined unlock schedule across all four buckets charted monthly for 48 to 60 months, showing aggregate new supply entering circulation?

If you can answer all eight with documentation, the allocation will hold up under institutional scrutiny. If you cannot, you have found your next piece of work.