LST Tokenomics: The Mechanics Behind Liquid Staking Token Design

LST tokenomics covers yield distribution, rebasing vs. exchange-rate models, slashing reserve design, and governance token structure. Here is how it works.

LST tokenomics governs how liquid staking protocols distribute yield, manage token supply mechanics, and design slashing reserves. The rebasing-versus-exchange-rate model fork is the primary design decision; exchange-rate tokens dominate DeFi because they preserve composability with AMMs and lending protocols.

LST tokenomics is the design of token models for liquid staking protocols, covering how staking yield is distributed, how token supply mechanics affect DeFi composability, and how slashing risk is absorbed without breaking the protocol's peg. The two primary design choices, rebasing tokens versus exchange-rate tokens, determine downstream composability across every lending protocol, AMM, and derivatives venue that integrates the LST. The governance token layer and slashing reserve architecture compound on top of those foundational choices. Getting LST tokenomics right means designing for a market that held more than $30 billion in TVL across liquid staking protocols by 2025 (Source: CryptoRank token market data), with institutional capital increasingly treating staked ETH derivatives as a balance-sheet asset. This guide covers the full mechanism: from the token model fork to yield architecture, slashing design, governance token value capture, and the failure patterns we see most often. For background on how DePIN tokenomics design handles adjacent incentive design problems at the infrastructure layer, that post covers the parallel mechanics.

#What Is an LST? The Token That Unlocks Staked Capital

LST tokenomics: the design of token models for liquid staking protocols, covering yield distribution architecture, token model selection (rebasing versus exchange-rate), slashing risk management, and governance token value capture.

Rebasing token: a liquid staking token whose holder balance adjusts automatically as staking rewards accrue, growing the token supply to distribute yield. Example: Lido's stETH.

Exchange-rate token: a liquid staking token whose holder balance remains fixed while the token appreciates in price relative to the underlying asset as rewards accrue. Example: Lido's wstETH, Rocket Pool's rETH.

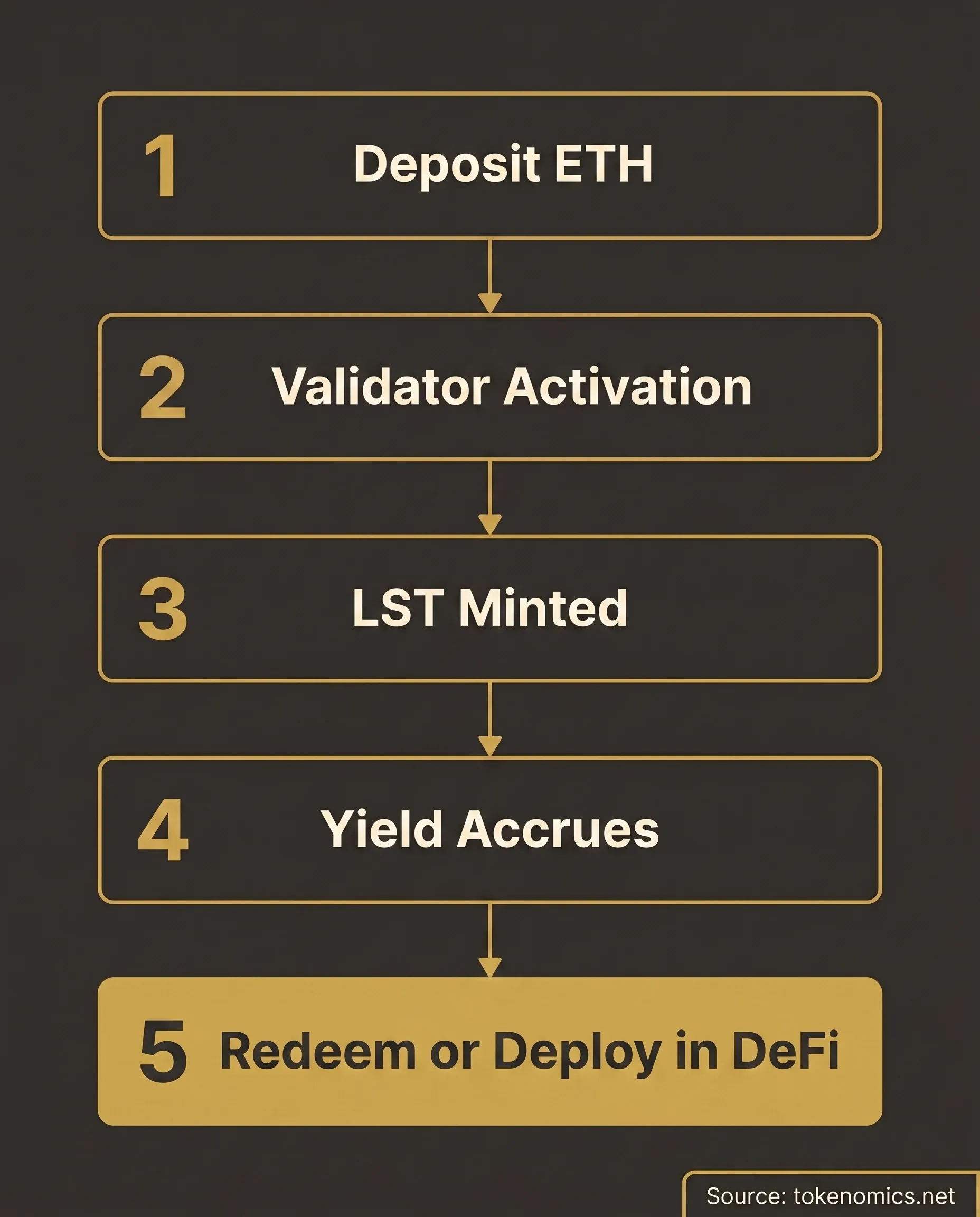

Liquid staking tokens represent staked positions in a proof-of-stake network. When you deposit ETH into a liquid staking protocol, you receive an LST that tracks your staked ETH plus accruing rewards. The underlying ETH keeps earning consensus rewards. The LST can be deployed across DeFi while that happens.

That is the core mechanic: converting illiquid staked capital into a composable DeFi asset. Without LSTs, ETH staked for network security sits locked until withdrawal. With LSTs, that capital earns yield AND moves through lending protocols, AMMs, and derivatives markets simultaneously.

Two token models implement this mechanic, and the choice between them shapes everything downstream.

Rebasing tokens (the canonical example is Lido's stETH) adjust the holder's balance automatically as rewards accrue. If you hold 10 stETH today and the protocol earns 3% annually, you will hold 10.3 stETH in a year without any transaction. The token supply grows to distribute yield.

Exchange-rate tokens (wstETH, Rocket Pool's rETH) keep the holder's balance fixed. The token itself appreciates in price relative to the underlying asset. You hold 10 wstETH today and still hold 10 wstETH in a year, but each wstETH is now redeemable for more ETH than before.

Most of the DeFi market runs on exchange-rate models now. The reason is composability: AMM pricing algorithms, lending protocol collateral calculations, and options pricing models all assume static balances per position. Rebasing tokens break those assumptions.

#How LST Yield Distribution Works

Three yield sources flow into every LST protocol: consensus layer rewards (base staking returns, historically 3-4% APY on ETH), MEV capture (Maximal Extractable Value from transaction ordering), and execution layer priority fees (tips paid by users for faster transaction inclusion). The mix varies by protocol architecture and market conditions.

The protocol fee is the revenue architecture. Most LST protocols extract 5-15% of gross staking rewards as a fee, then split that fee between node operators (who run validators) and the protocol treasury (which funds development, slashing reserves, and DAO grants). Lido, for example, takes a 10% fee split evenly between its node operator set and the DAO treasury (Source: Lido Finance protocol parameters, on-chain governance records).

Rocket Pool operates differently. Node operators in the Rocket Pool system must bond both ETH and RPL tokens as collateral, and they earn a commission from the shared ETH pool on top of their own staking rewards. That commission rate compresses and expands based on market demand. The tokenomics here build operator alignment directly into the fee structure: operators have skin in the game because their RPL collateral is at risk if the protocol suffers losses (Source: Rocket Pool documentation, validator collateral specifications).

Revenue-first framing matters here. The protocol fee architecture IS the tokenomics. The yield split determines what the governance token can fund, what the slashing reserve can absorb, and whether the treasury compounds or depletes over time. All other design decisions, governance token mechanics, insurance structures, growth incentives, are secondary layers built on top of the yield engine.

For context on how LST fee structures fit into broader token velocity problem dynamics in DeFi, the token velocity post covers how fee extraction rate interacts with holder incentives across protocol types.

#Rebasing vs. Exchange-Rate Models: The Design Fork

The dominant instinct when building an LST is to show users their rewards accumulating in real time. That points toward rebasing. The wallet balance grows visibly. Users see yield without any action on their part. It feels intuitive.

That doesn't work for DeFi composability.

Lending protocols calculate collateral ratios based on token balances at the time of deposit. AMMs price swaps based on pool reserves. If the token balance in a pool or a collateral account grows every day without a transaction, the math breaks. Protocols that integrated stETH directly discovered this and had to build workarounds.

Lido's solution was to wrap stETH into wstETH, an exchange-rate token that holds stETH inside and appreciates in price while balance stays fixed. Most protocols that interact with Lido's staking position do it through wstETH now, not stETH directly.

The exchange-rate model also has an advantage in jurisdictions where rebase events may trigger tax liability. Under some legal frameworks, each automatic balance increase is a taxable receipt of new tokens. An exchange-rate token that simply appreciates in price defers realization until sale. This is not tax advice; it is a design consideration that legal teams at protocol projects routinely flag when evaluating token model choices. Founders should get their own legal opinion before relying on this distinction.

New LST protocols launching today almost universally choose the exchange-rate model or offer an exchange-rate wrapper from day one. The rebasing-versus-exchange-rate debate is largely settled in favor of exchange-rate for DeFi-native deployments.

#Slashing Risk and Insurance Reserve Design

Validators can be penalized for protocol violations: double-signing (signing two conflicting blocks), extended downtime, and other infractions. When a validator in a liquid staking protocol is slashed, every LST holder in that pool absorbs the loss proportionally. The protocol's ability to absorb that loss without breaking the peg to underlying ETH is the slashing reserve design problem.

Rocket Pool addresses this through mandatory operator collateral. Operators must bond RPL worth at least 10% of their ETH value when joining the protocol (Source: Rocket Pool documentation, node operator minimum collateral requirements). If a Rocket Pool operator is slashed, their RPL collateral is liquidated first to compensate the pool, before any loss reaches LST holders. This makes slashing liability proportional to the party who caused it.

Lido uses a different model. Its larger validator set (500+ node operators as of 2025) reduces the statistical likelihood of correlated slashing events, while the DAO treasury serves as a backstop. Lido has also been developing a staking router system to decentralize validator selection further, which reduces single-point slashing exposure (Source: Lido Finance governance forum, staking router proposals).

The reserve design principle: a protocol extracting 10% of gross yield in fees should route a defined percentage of that fee to slashing reserves before any other treasury use. A protocol optimizing for competitive APY by redirecting all fee income to governance token buybacks or liquidity incentives while holding zero reserves is taking an unquantified tail risk with its depositors' capital.

The structural design of governance tokens in DeFi protocols intersects with tokenomics compliance requirements in the post-FIT-21 regulatory environment, particularly for protocols with governance tokens that resemble profit-distribution rights.

#The Governance Token Layer: When LDO or RPL Matters

Most LST protocols have a governance token alongside the LST itself. LDO for Lido, RPL for Rocket Pool, FXS for Frax (which governs sfrxETH allocation). Understanding what these tokens actually control determines whether they have durable value or are purely speculative overlays.

LDO holds governance rights over one of the largest validator sets in Ethereum. The Ethereum Foundation has published analysis noting that Lido's share of total staked ETH approaching 33% would represent a systemic risk to Ethereum's consensus mechanism. The governance token that controls that validator set is, structurally, a governance token that controls infrastructure that Ethereum itself depends on. That creates both value and responsibility (Source: Ethereum Foundation, notes on liquid staking concentration risks).

RPL's design is materially different. It is both a governance token and mandatory operator collateral. Node operators must hold RPL to participate in the Rocket Pool system. That creates organic, use-case-driven demand that does not depend solely on fee speculation or governance participation rates.

The lesson: a governance token for an LST protocol should control a structural chokepoint, validator onboarding criteria, upgrade authorization, fee parameter bounds, not merely vote on treasury allocation. A governance token that only determines where treasury funds go is competing with the LST itself on yield and has limited non-speculative demand.

#Common LST Tokenomics Mistakes

After working through the mechanism design on dozens of DeFi protocol engagements, the failure patterns are predictable.

Launching a rebasing token for composability. The team wants users to see yield accrue in their wallet. They choose a rebasing model without mapping out which lending protocols, AMMs, and yield aggregators they need to integrate with. Six months later, half of their target DeFi integrations require a wrapped variant and the team is maintaining two token contracts with fragmented liquidity.

No slashing reserve with a competitive fee structure. The protocol routes all fee income to governance token buybacks or liquidity incentives to compete on APY. There is no reserve buffer. A correlated slashing event, a client bug hitting 5% of validators simultaneously, results in a peg break, not a minor NAV adjustment.

Governance token with no structural use case. The governance token votes on fee parameters and treasury grants. It does not control validator onboarding or upgrade authorization. There is no required-hold use case. The token's price tracks protocol TVL in a bull market and decouples entirely in a bear market. "The governance token that controls nothing of value is worth nothing over time."

Fee compression without a treasury floor. The protocol cuts its fee from 10% to 5% to attract TVL during a competitive staking environment. There is no minimum treasury reserve requirement in the governance framework. The treasury depletes, development slows, and slashing reserves sit at zero when the stress test arrives.

Single-client validator dependence. The protocol's node operators overwhelmingly run one execution client and one consensus client. The tokenomics do not include incentives for client diversity (higher rewards for operators using minority clients, for example). A bug in the majority client can trigger mass correlated slashing. This is not theoretical risk: client diversity has been a live concern in the Ethereum validator community since the Merge. Coinbase has published guidance on validator client distribution and correlated slashing risk for institutional staking participants.

#How to Evaluate an LST Protocol's Tokenomics

We use what we call the LST Design Audit to evaluate an LST protocol's tokenomics. Five questions structure the review.

What is the token model? Rebasing or exchange-rate? If rebasing, is there a wrapped variant and which DeFi protocols have integrated through which model? The answer tells you about composability risk and where liquidity is likely to fragment.

Where does yield come from, and what is the protocol fee rate? Is the fee split documented in on-chain governance? How is it allocated between operators, treasury, and reserves? A protocol that cannot answer this question in a governance proposal with specific percentage breakdowns is operating without a revenue architecture.

How is slashing risk absorbed? What is the slashing reserve size, and is there a trigger threshold (minimum reserve level below which protocol fees cannot be distributed to any other use)? Operator collateral and DAO treasury backstops are both valid structures, but the coverage ratio should be published and auditable.

What does the governance token control? Validator onboarding criteria, fee bounds, upgrade authorization, or treasury allocation only? The answer tells you whether the governance token has structural demand or is purely speculative.

What is the validator set composition? Is client diversity tracked and disclosed? Is operator concentration disclosed (what percentage of total stake is held by the top 5 operators)? These are the systemic risk disclosures that institutional integration teams will ask for.

#Frequently Asked Questions

What is LST tokenomics? LST tokenomics is the design of token models for liquid staking protocols. It covers how staking yield is distributed between depositors, node operators, and the protocol treasury; how the token supply model (rebasing or exchange-rate) affects DeFi composability; how slashing risk is absorbed through insurance reserves and operator collateral; and how the governance token captures structural demand beyond speculation.

What is the difference between stETH and wstETH? stETH is Lido's rebasing token: holder balances grow automatically as staking rewards accrue, with new tokens minted to represent the yield. wstETH is Lido's exchange-rate wrapper: holder balances stay fixed while each wstETH appreciates in price as the underlying stETH accrues rewards. Most DeFi integrations use wstETH because static balances are composable with AMMs, lending protocols, and derivatives markets.

How do LST protocols handle slashing risk? Protocols use two main models. Rocket Pool requires node operators to bond RPL collateral worth at least 10% of their ETH value; slashing penalties liquidate operator collateral before touching depositor funds. Lido operates a larger, vetted node operator set with DAO treasury backstop. Both approaches aim to ensure that no individual validator failure cascades to a full peg break.

Why does the governance token matter for LST tokenomics? Governance tokens that control structural chokepoints, validator onboarding criteria, upgrade authorization, and fee parameter bounds have use-case-driven demand beyond speculation. Tokens that only vote on treasury allocation compete with the LST itself on yield and have limited non-speculative demand. The RPL model, which makes operator collateral mandatory, is a stronger structural design than a governance-only token.

What is the biggest risk in LST tokenomics design? Launching with inadequate slashing reserves while optimizing for competitive APY is the highest-frequency failure pattern. Protocols that route all protocol fee income to governance token buybacks or liquidity incentives with zero reserve buffer take on tail risk proportional to their validator set size. A correlated slashing event, such as a majority client bug, produces a peg break rather than a recoverable NAV adjustment.

Are LSTs composable with lending protocols? Exchange-rate LSTs (wstETH, rETH) are broadly composable with major lending protocols because their balances are static. Rebasing LSTs (stETH) require special handling or wrapping before most lending protocols can accept them as collateral, because rebasing balance increases disrupt collateral ratio calculations. This is why most new LST designs launch as or wrap into exchange-rate tokens.

What should a DeFi integration team ask about an LST before integrating? The five questions are: What token model is it (rebasing or exchange-rate)? What is the protocol fee rate and how is it allocated? What is the slashing reserve structure and coverage ratio? What does the governance token control? What is the validator client diversity and operator concentration disclosure? These questions address composability risk, tail risk, and governance risk simultaneously.

Slashing reserve: a capital buffer maintained by a liquid staking protocol to absorb validator penalty losses before they reach depositor funds. May be funded through operator collateral (Rocket Pool model) or DAO treasury (Lido model).

If you are building onchain and need your LST tokenomics to hold up under institutional scrutiny, book a discovery call. We will assess your protocol design and tell you whether we are the right fit. Sometimes we are not. We will tell you that too.

If you need a systematic review of your full token model, the complete data room is where that work gets done.