DePIN Tokenomics: Incentive Design for Decentralized Physical Infrastructure

DePIN tokenomics designs token incentives for decentralized physical infrastructure. Learn the Three-Layer Incentive Stack and Revenue-First Design framework.

DePIN tokenomics designs token incentive systems for decentralized physical infrastructure protocols, coordinating hardware node operators through cryptographic rewards. A sound DePIN token model balances operator unit economics, supply sustainability, and demand-side revenue transition across a multi-year bootstrap period before the network can self-fund through real service revenue.

DePIN tokenomics is the discipline of designing token incentive systems for decentralized physical infrastructure networks: protocols that coordinate real-world hardware through cryptographic rewards. These protocols span wireless networks (Helium), distributed compute (Render, NOSANA), distributed energy (Glow, Arkreen), mobility and mapping (Hivemapper), and environmental sensors. DePIN token design must accomplish something DeFi tokenomics never has to: pay node operators enough to cover real capital costs, including hardware, connectivity, power, and maintenance, while keeping total supply sustainable over a multi-year bootstrap period.

The failure mode is predictable. Front-loaded emissions attract mercenary hardware operators who deploy equipment, collect rewards, and dump tokens the moment yield compresses. What remains is empty infrastructure with no demand side and a token supply that can't sustain further operator acquisition. If the protocol's revenue model doesn't generate enough demand-side income to fund operator rewards eventually, the token is the only source of payment. That math compounds against you. If you're evaluating this for your own protocol, book a strategy call before locking in the supply schedule.

#What DePIN Tokenomics Has to Solve (The Core Design Challenge)

DePIN tokenomics: the design discipline for token incentive systems that coordinate decentralized physical infrastructure networks, balancing operator economics, supply sustainability, and demand-side revenue transition across a multi-year deployment horizon. Sound DePIN tokenomics begins with operator unit economics, not with token price targets.

DePIN operators make capital investments before any token income arrives. A Helium hotspot operator spent $400 to $600 in hardware before earning the first HNT. A NOSANA compute contributor configures and runs a GPU node against an uncertain demand fill rate. That upfront commitment changes the incentive calculation entirely.

DeFi liquidity providers add capital with zero physical friction. A DePIN node operator adds a physical asset with significant setup friction, ongoing operating cost, and an exit cost if the protocol underperforms. This is why DePIN tokenomics cannot be modeled on DeFi liquidity mining. The DePIN reward mechanisms that work are fundamentally different from yield-farming incentive loops.

Proof-of-Coverage: a cryptographic mechanism used by DePIN protocols to verify that a node operator is providing genuine infrastructure coverage in a declared geographic area, typically using GPS coordinates, radio signal attestations, or peer-witness validation recorded on-chain.

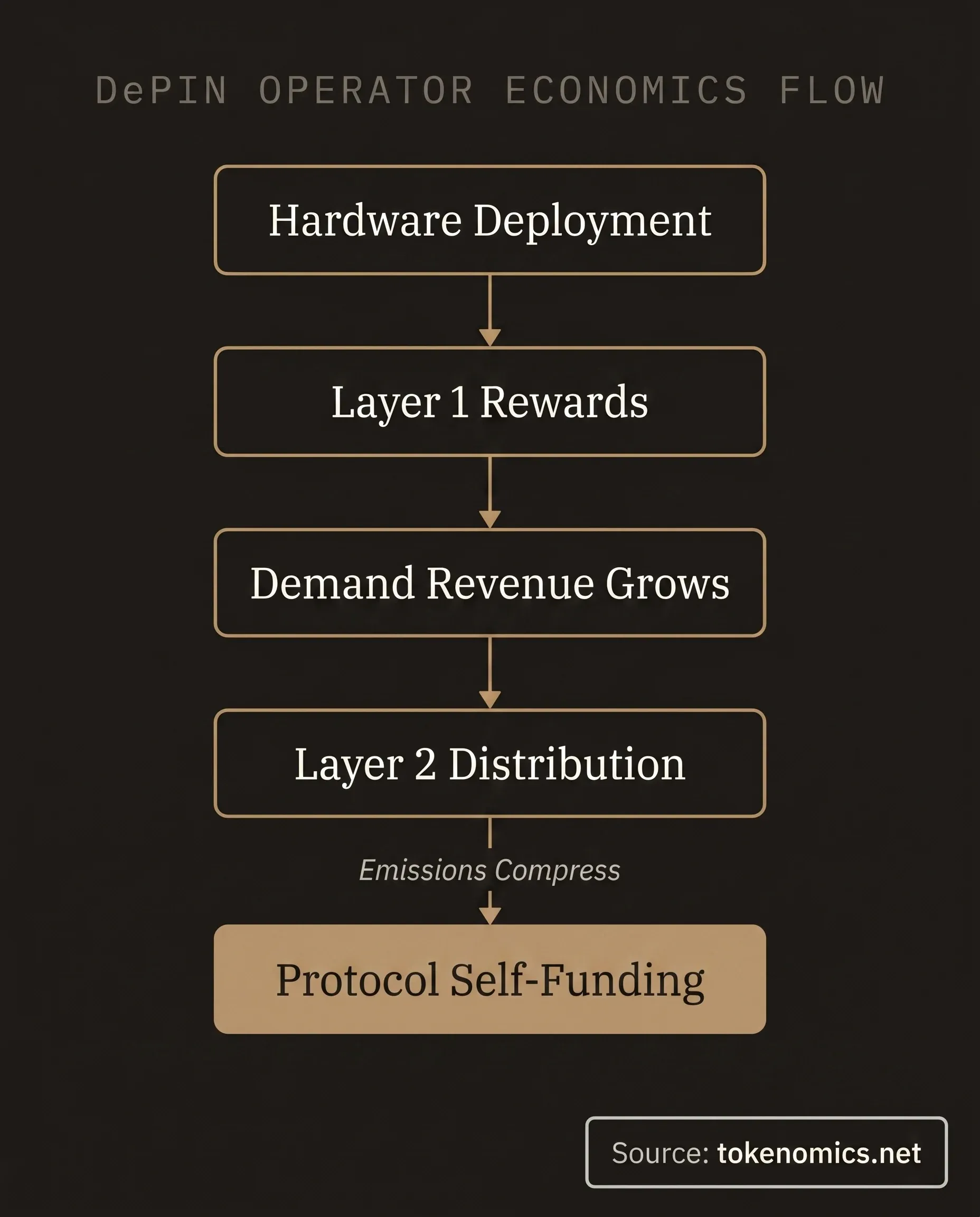

The design challenge has three simultaneous requirements. First, rewards must be high enough at launch to attract initial hardware deployment, covering the gap between what operators earn from demand-side activity and what they actually spend running the node. Second, rewards must compress over time as demand-side revenue grows. Emissions are a bootstrap subsidy, not a permanent income stream. Third, the transition from emission-subsidy to revenue-funded reward must not produce a cliff that triggers mass operator exit in the same epoch.

The DePIN sector passed $20 billion in projected market value in 2024, with over 650 active DePIN protocols across compute, wireless, energy, and sensing categories (Source: Messari DePIN Sector Report). Most are still in bootstrap phase. Decentralized physical infrastructure tokenomics is a young discipline, and most of the frameworks being applied were borrowed from DeFi without modification. The protocols that survive will be the ones that adapted the design to the physical infrastructure cost structure from the start.

#The Three-Layer DePIN Incentive Stack

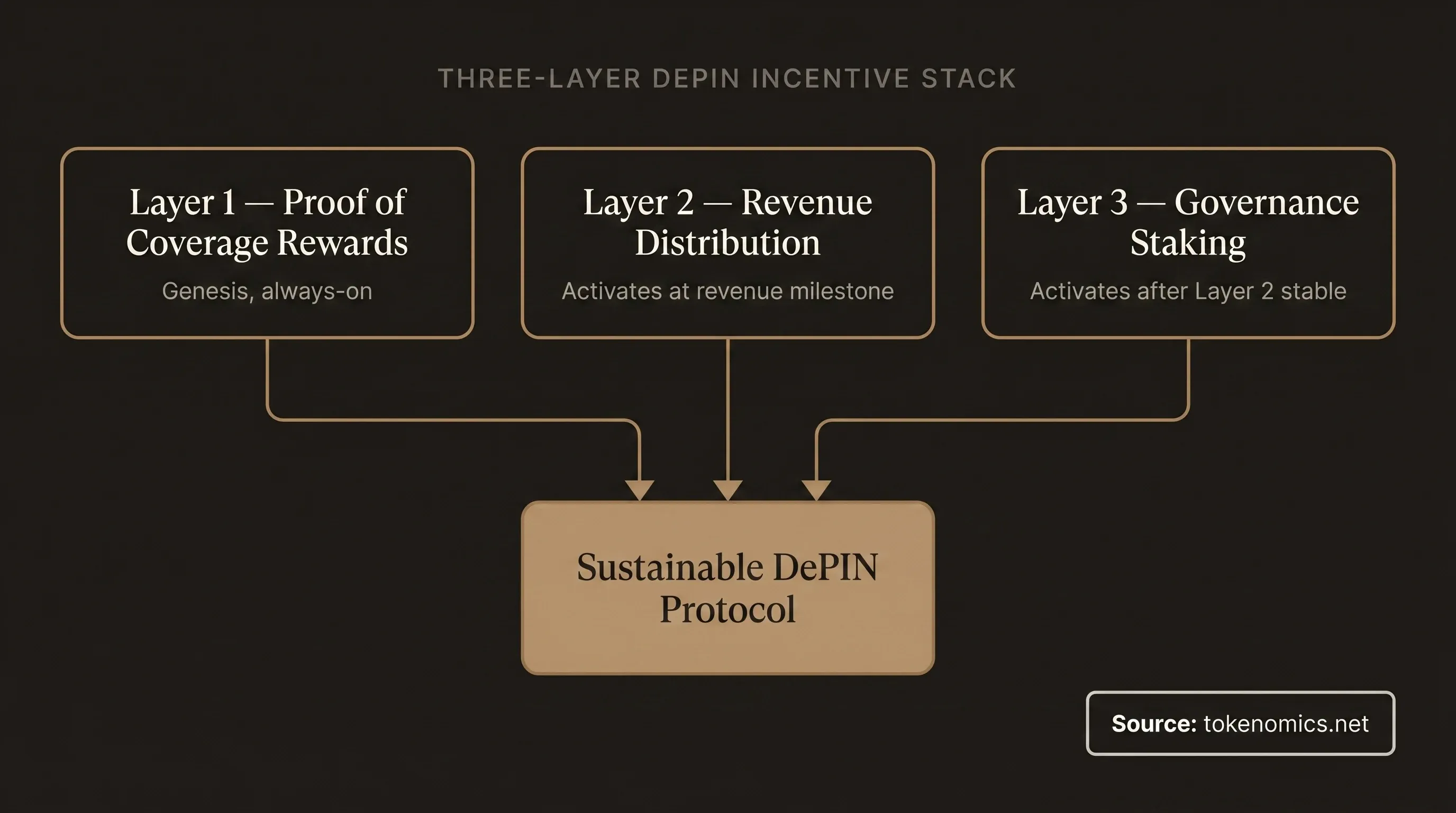

Every DePIN tokenomics model we've built from scratch uses what we call the Three-Layer DePIN Incentive Stack. This is the core framework we apply when a DePIN tokenomics engagement starts: before the whitepaper, before the legal opinion, before the supply schedule. The layers are not simultaneous from day one. They're sequential. Getting the sequencing wrong is one of the most consistent failure patterns we see.

Layer 1: Proof-of-Work / Proof-of-Coverage reward. The base reward for providing infrastructure availability, measured on-chain. This layer goes live at genesis. Operators earn tokens for being online, in coverage, and verified by the oracle. Design considerations for this layer: oracle quality and manipulation resistance, sybil-attack prevention (GPS spoofing, heartbeat faking), coverage-map weighting vs. actual demand weighting, and epoch duration. A key decision: should Proof-of-Coverage rewards be denominated in the native token or in a stablecoin-indexed unit? Indexing to a stable unit protects operators against token price volatility in the bootstrap phase but introduces currency-conversion mechanics the protocol must fund.

Layer 2: Demand-side revenue distribution. When the network generates real revenue, whether data buyers, compute buyers, or energy consumers paying for network services, that revenue flows back to active operators as supplemental reward. Layer 2 goes live when demand-side revenue is non-trivial. This is the sustainability layer. It is what transitions the protocol from emission-dependency to a self-funding model. The design questions: what fraction of gross revenue goes to operators vs. the treasury vs. the protocol development fund? How is revenue attributed to specific operators vs. pooled across the network? How often is it settled?

Layer 3: Governance and staking rewards. How long-term aligned capital earns yield in exchange for protocol governance participation and providing economic security through staked deposits. This layer scales as the protocol matures. Design choices: ve-tokenomics (vote-escrow) with lock-period multipliers, or simple staking with a flat APY?

ve-tokenomics (vote-escrow tokenomics): a governance model in which token holders lock tokens for a fixed period (typically 1 week to 4 years) in exchange for voting power proportional to lock duration and quantity. Longer locks earn higher multipliers on both governance weight and reward distributions, aligning long-term holders with protocol outcomes. Delegation mechanisms? Revenue-share split between Layer 2 (operators) and Layer 3 (stakers)?

The sequencing rule: Layer 1 is always-on. Layer 2 activates on a governance-triggered milestone (revenue threshold, not a calendar date). Layer 3 launches after Layer 2 is stable, so staking yields are backed by real revenue rather than emissions alone. Most DePIN projects launch all three simultaneously, creating competing incentive signals and unnecessary governance complexity from day one. That doesn't work. Poor sequencing is the second most common DePIN tokenomics mistake we see after unit-economics mismodeling. For more on incentive design across token categories, see all articles on the Tokenomics.net blog.

#Supply Architecture in DePIN Tokenomics

Most DePIN projects set emissions based on what looks attractive to early hardware operators, not on the protocol's long-term cost basis. This is the most common DePIN tokenomics failure we see in the supply architecture phase. A round-number APY ("100% APY for year-one nodes") gets picked in a committee, approved as a headline number for the whitepaper, and then interacts with supply dilution, token price volatility, and operator exit behavior in ways the committee didn't model. The result is either hyperinflation or rapid operator turnover in months 12 to 18.

The right starting point is operator unit economics.

Node operator unit economics: the per-node monthly cost-and-revenue calculation for a DePIN protocol, including hardware amortization, connectivity, power, and maintenance costs on the expense side, and demand-side service revenue plus token rewards on the income side. The gap between these two figures is what the protocol's emission budget must cover during the bootstrap phase.

What does it cost to run one node per month? Broken down by hardware amortization, connectivity, power, and ongoing maintenance. That's your emission floor for one node. Multiply by target network size. Subtract projected demand-side revenue. What remains is the emission budget that the token supply must fund across the bootstrap phase.

Total supply design follows from that math. DePIN protocols typically benefit from larger total supply relative to DeFi protocols because node rewards must be sustained for years before demand-side revenue closes the gap. A five-to-seven-year bootstrap horizon is the practical target. If the protocol's emission schedule hits the terminal supply cap before year five, and demand-side revenue hasn't covered the gap, the model breaks.

Inflation rate management: the standard approach decreases emissions by 20-33% per epoch, similar to Bitcoin's halving logic, giving operators predictable planning horizons (Source: Helium Foundation epoch reward design documentation). Hard cap vs. perpetual low inflation is a genuine design decision for DePIN. Protocols with ongoing physical infrastructure costs often choose perpetual low inflation at 1-2% annually rather than a hard cap, because operators need a guaranteed subsidy floor if demand-side revenue remains insufficient in specific geographies or network segments.

Vesting and insider allocation: team and investor tokens should vest on the same timeline or longer than the operator reward ramp. If team tokens unlock in year two and the demand thesis hasn't been proven yet, the market reads that unlock as insider exit pressure. Standard for DePIN: 12-month cliff, 4-year linear vest for team and investors. Operator rewards vest immediately on distribution (no vesting on earned rewards) but are subject to slashing if fraud is detected.

DePIN-specific supply risk: Proof-of-Coverage gaming inflates rewards without delivering infrastructure value. Operators who spoof GPS coordinates, fake heartbeats, or run collusion rings between controlled hardware nodes extract rewards from the supply without contributing to network utility. Circuit-breaker mechanisms include oracle stake (operators put up collateral that is slashed on fraud detection), fraud-proof periods before rewards settle, and coverage randomization that makes collusion geographically harder. These mechanisms add operational overhead but are non-optional for any Proof-of-Coverage model operating at scale. To learn more about the firm that builds these models, see the book a strategy call.

#Common DePIN Tokenomics Mistakes (Pattern Recognition From 80+ Projects)

After advising 80+ projects across DeFi, RWA, and DePIN categories, the failure patterns in DePIN tokenomics are predictable. Here's what kills DePIN protocols in the first 12 to 24 months.

Emission rate set by committee, not by unit economics. Teams pick a headline APY without modeling how that rate interacts with supply dilution and token price. When token price drops 70% (a normal DePIN bootstrap-phase event), the dollar-denominated operator reward drops with it. Operators who modeled a $400/month return are now earning $120. Exit rate spikes. Coverage collapses. The network fails not from bad technology but from a tokenomics model that never accounted for denominator risk.

No demand-side revenue model. The protocol plans to monetize "eventually," with no pricing, no customer commitments, and no revenue timeline. Emissions are running on a schedule. Demand is aspirational. The token becomes a countdown timer. A token without sustainable revenue mechanics is a countdown timer. This isn't hypothetical risk. It's the most common pattern across DePIN protocols that launched with strong hardware metrics and then hit a wall when emissions compressed.

Coverage weighted over demand. The protocol rewards operators for being online in any covered area, not for serving actual network traffic. Mercenary operators cluster in easy-to-cover zones. High-demand zones with harder hardware logistics remain underserved. The coverage map looks full. Actual network utility gaps persist. The fix is demand-weighted reward: operators in high-utilization zones earn more than operators in low-utilization zones, even if their coverage area is the same.

Sybil resistance underinvested. Proof-of-Coverage protocols that rely on GPS coordinates and periodic heartbeat pings are gameable. One sophisticated bad actor with 20 devices in a warehouse can generate spoofed coverage reports and extract rewards at scale before detection. By the time the protocol identifies and slashes the fraudulent nodes, the economic damage is done. Oracle stake and fraud-proof settlement periods are table-stakes for any production DePIN Proof-of-Coverage system.

Governance token decoupled from infrastructure operations. When the governance token floats separately from the operational reward token, stakers can vote on protocol parameters with no skin-in-the-game accountability for the physical infrastructure they're governing. The mismatch produces governance outcomes that optimize for token price rather than for network utility. Operators who understand the ground truth of running hardware get outvoted by capital holders who have never deployed a node.

These aren't edge cases. They're the patterns we see on DePIN projects that fail in the first 12 to 24 months.

#How to Build a DePIN Tokenomics Model: The Six-Step Process

The DePIN tokenomics design process follows a specific sequence. Running these steps out of order produces the failure patterns above.

Step 1: Map node operator unit economics. Cost per node per month, broken down by hardware amortization, connectivity, power, and maintenance. This is your emission floor. You cannot design a reward schedule that falls below this number for an extended period without losing your operator base.

Step 2: Model the demand-side revenue curve. At what network penetration does demand-side revenue cover 50% of operator cost? 100%? Build three scenarios: bear (demand adoption takes 5 years), base (3 years), bull (18 months). Run Monte Carlo simulations across 10,000 iterations with variable demand growth rates and token price assumptions. The output is a distribution of outcomes for your supply model, not a single projection (Source: Monte Carlo methodology per Tokenomics.net standard framework).

Step 3: Set the emission budget per epoch. Emissions per epoch = (operator cost per node per epoch - demand revenue per node per epoch) x target node count. Build in an emission-adjustment mechanism the protocol can invoke via governance without a contentious vote. The adjustment trigger should be metric-based (network utilization rate, not token price).

Step 4: Design the supply schedule. Total supply, initial circulating supply, unlock cliffs for team and investors, halving epochs for operator rewards. Stress-test the fully diluted valuation at TGE: if circulating supply multiplied by target token price implies a demand-side revenue multiple no comparable DePIN protocol has achieved at that network scale, the model is broken. Bring the emission schedule in line before launch.

Step 5: Choose token standard and architecture. DePIN protocols typically deploy utility tokens on ERC-20 compatible chains or native chains built on Solana, Cosmos, or Polkadot substrate. If reward tokens flow across L2s or rollups, design the bridge architecture before finalizing the token standard. A cross-chain reward token that requires a custom bridge adds audit surface and introduces a centralization risk point that regulators and institutional investors will flag.

Step 6: Define governance token mechanics. If using a separate governance token or ve-token layer for Layer 3: design lock durations, boost multipliers, delegation mechanisms, and the revenue-share split between Layer 2 (operators) and Layer 3 (stakers). The ve-tokenomics model (popularized by Curve Finance, described in the Curve DAO voting-escrow specification) creates long-term alignment but introduces liquidity lock-up friction that can suppress participation in early-stage protocols. Simpler staking models may be the right call for DePIN protocols with a less developed secondary market.

The full DePIN tokenomics model should include financial projections across all three scenarios and a token supply chart that shows the circulating supply trajectory over five years under each scenario. Investors and exchanges will ask for this. Build it before you need it.

#DePIN Tokenomics and the Regulatory Horizon for Token Classification

DePIN tokens are typically structured as utility tokens. The rewards are denominated in the protocol's native token in exchange for providing network services, not as investment returns on a passive capital stake. That structural distinction matters for how legal teams approach DePIN tokenomics classification in the U.S. context under the Howey test and in the EU context under MiCA (Markets in Crypto-Assets).

That said, "structured as a utility token" is not a compliance conclusion. It's the starting point for a compliance analysis. Whether a specific DePIN token qualifies for a utility-token treatment depends on the token's design, the protocol's degree of decentralization, the nature of the investor relationship, and the jurisdiction. Protocols that sell tokens at a discount to early investors, with locked rewards that appreciate as the network grows, are closer to the investment contract pattern than protocols that distribute rewards exclusively to active operators who provide ongoing services.

Get the legal opinion before finalizing token design. The compliance architecture is easier to build into the DePIN tokenomics model from day one than to retrofit after tokens are issued and trading.

#Frequently Asked Questions

How do I calculate the emission budget for a DePIN protocol?

Start with node operator unit economics: the cost per node per month broken down by hardware amortization, connectivity, power, and maintenance. Subtract the projected demand-side revenue per node at your target network size. The difference is your emission floor for one node. Multiply by the target node count and the bootstrap horizon in epochs to get the total emission budget. Run this calculation across bear, base, and bull demand scenarios, not a single projection.

What happens if a DePIN protocol's demand-side revenue never covers operator costs?

The protocol enters a perpetual emission dependency. If the emission schedule is time-bound (a hard total supply cap), the protocol runs out of subsidy before reaching self-sufficiency. Operators exit. Coverage collapses. The token has no remaining source of reward and the network fails. If the emission schedule is perpetual (no hard cap), the protocol survives but dilutes indefinitely, eroding token value for all holders. Neither outcome is acceptable. A credible demand-side revenue model is a prerequisite for DePIN tokenomics design, not an afterthought.

Can a DePIN token be classified as a utility token and avoid securities law?

DePIN tokens are typically structured as utility tokens, earned in exchange for providing an active infrastructure service. That structure is a starting point for compliance analysis, not a conclusion. Whether a specific token avoids securities treatment depends on the token's design, the protocol's degree of decentralization, whether tokens are sold to passive investors expecting profit from others' efforts, and the jurisdiction. In the U.S., the Howey test is the analytical framework. In the EU, MiCA (Markets in Crypto-Assets) governs. Get legal counsel with DePIN and digital asset experience before launching any token offering.

How does Proof-of-Coverage fraud affect DePIN tokenomics?

Fraudulent Proof-of-Coverage reports inflate rewards without delivering infrastructure value. When operators fake GPS coordinates, heartbeat signals, or peer-witness attestations, they extract token rewards from the supply without contributing to network coverage. The economic effect is unearned dilution: legitimate operators and token holders absorb the cost. At scale, Proof-of-Coverage fraud can make emission rates unsustainable and undermine operator trust in the reward system. Mitigation requires oracle stake (collateral subject to slashing), fraud-proof settlement periods, and coverage randomization.

What is the difference between the three layers in DePIN incentive design?

Layer 1 (Proof-of-Coverage / Proof-of-Work rewards) pays operators for providing infrastructure availability. It activates at genesis and is always-on. Layer 2 (demand-side revenue distribution) routes real service revenue back to active operators as supplemental income. It activates when the network generates non-trivial revenue. Layer 3 (governance and staking rewards) compensates long-term aligned capital that participates in protocol governance. It activates after Layer 2 is stable, so staking yields are backed by real revenue. The sequencing is non-negotiable: launching all three simultaneously creates competing incentive signals before the protocol has proved its demand thesis.

When should a DePIN protocol launch its governance token?

After the demand-side revenue layer (Layer 2) is live and stable. Launching governance before Layer 2 means staking yields depend entirely on emissions, which ties governance incentives to the same supply pressure the operator rewards are creating. The governance token's value case is strongest when holders have evidence that the protocol generates real revenue and that staking yields are partially backed by that revenue rather than solely by emission inflation.

What vesting schedule should DePIN team and investor tokens follow?

The standard for DePIN protocols is a 12-month cliff followed by 4-year linear vesting for both team and investor allocations. This schedule ensures that insider tokens unlock on a timeline comparable to or longer than the protocol's demand-side revenue ramp. If team tokens unlock in year two and the demand thesis hasn't been validated, the market reads that unlock as insider exit pressure regardless of the team's actual intentions. Align token unlocks with demand milestones, not calendar dates, whenever possible.

#Conclusion

DePIN protocols are building the infrastructure layer of the decentralized economy. Compute, wireless, energy, mobility, and sensing capacity delivered through cryptographically coordinated hardware networks. The token model is what decides whether that infrastructure survives the bootstrap phase or becomes abandoned hardware with a dead token.

The Revenue-First Design frame is what separates DePIN protocols that make it to demand-side sustainability from the ones that spend their emission budget and collapse. Start with operator unit economics. Model the demand-side revenue curve before setting the emission schedule. Sequence the three incentive layers correctly. Design Proof-of-Coverage fraud resistance before it becomes a production crisis. That sequence is the discipline behind sound DePIN tokenomics.

The standard for DePIN tokenomics is getting more specific as institutional capital enters the category. Investors who funded the first wave of DePIN protocols have a clear picture of what caused failures. The next wave of DePIN projects will be evaluated against that track record.

If you're building a DePIN protocol and need your DePIN tokenomics to hold up under institutional scrutiny, book a strategy call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.