LRT Tokenomics: Mechanism Design for Liquid Restaking Protocols

LRT tokenomics covers restaking yield composition, multi-AVS slashing risk, fee layering, and governance token design. Here is how the mechanism works.

LRT tokenomics is the mechanism design governing liquid restaking protocols. It covers how restaking yield is composed from base staking plus AVS operator fees, how slashing risk is structured across independent validation duties, and how the protocol's fee layers interact with the underlying staking yield.

LRT tokenomics is the design of token models for liquid restaking protocols, covering how restaking yield is composed and distributed, how slashing risk is structured across multiple validation duties, and how the restaking fee layer interacts with the underlying staking yield. An LRT, or liquid restaking token, takes a staked position (ETH or an LST) and pledges it to secure additional networks beyond Ethereum, then wraps that position into a liquid, transferable token. That single move stacks new yield on top of base staking, and it stacks new risk on top too.

The design question is not just how to distribute yield. It is how to distribute risk. And underneath both sits the harder question: whether the protocol's revenue model actually holds up, because the entire value proposition depends on AVS fees materializing at the rate the yield stack promises. Liquid restaking opened a new yield category on top of Ethereum staking. It also layered in new slashing vectors, operator concentration risk, and fee-stacking complexity that pure liquid staking design never had to address. A protocol that gets the yield story right and the risk story wrong is a countdown timer.

This post covers the restaking-specific mechanics. For the staking fundamentals underneath (rebasing versus exchange-rate models, base staking yield, slashing reserve basics) the LST tokenomics post covers the layer below. This guide builds on top of that foundation.

#What LRT Tokenomics Is: Definition and Core Design Problem

LRT tokenomics: the token economics of liquid restaking protocols, covering restaking yield composition (base staking plus AVS operator fees), multi-AVS slashing risk architecture, protocol fee layering, and governance token structural design.

Actively Validated Service (AVS): a network or service that buys security from a restaking marketplace. Operators validate the AVS using staked collateral and earn a fee for the guarantee. Each AVS sets its own slashing conditions.

Liquid restaking token (LRT): a transferable token representing a restaked ETH position pledged to secure one or more Actively Validated Services, combining base Ethereum staking yield with AVS operator fees while exposing the holder to multi-vector slashing risk.

An LST represents staked ETH earning consensus rewards from Ethereum's validator set. One obligation, one yield source, one slashing vector. The staked ETH secures Ethereum and nothing else.

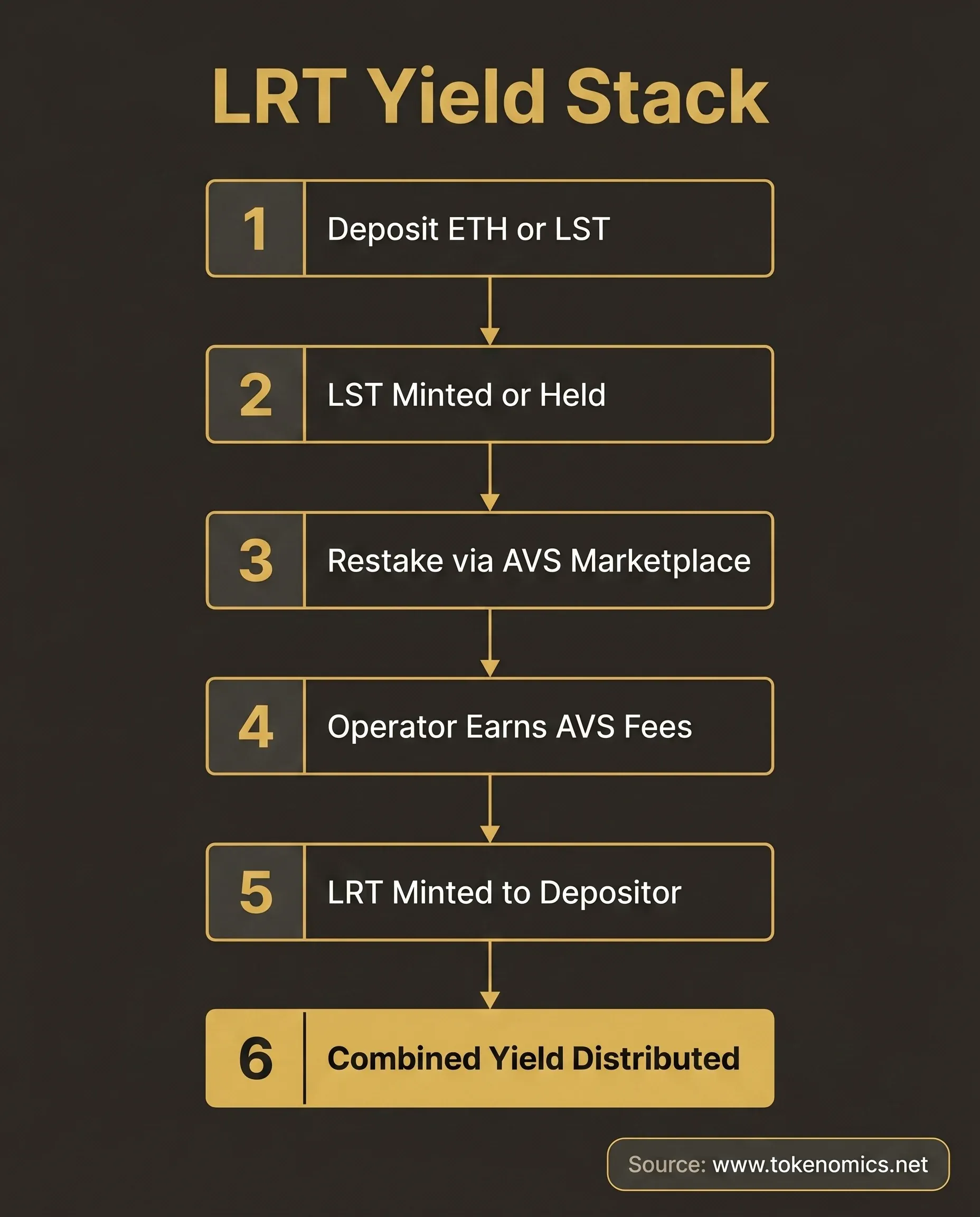

An LRT represents restaked ETH, or an LST, pledged to secure additional networks on top of Ethereum. Those additional networks are AVSes. The same collateral now backs multiple security obligations at once. Multiple obligations, compounded yield sources, multiple potential slashing vectors.

EigenLayer is the canonical restaking marketplace: stakers opt in to validate additional services using the same staked ETH as collateral, and the LRT wraps that position into a liquid token (Source: EigenLayer whitepaper). It is not the only model. Karak and Symbiotic run non-EigenLayer restaking architectures with distinct security and fee designs (Source: Karak documentation; Symbiotic documentation). Do not conflate every LRT protocol with EigenLayer specifically.

The key design difference is structural. An LST protocol manages one security obligation: Ethereum consensus. An LRT protocol manages N security obligations simultaneously, each with independent slashing conditions. Every dimension of the tokenomics scales with that N.

#Restaking Yield Composition: Where LRT Returns Actually Come From

Restaking yield: the combined return earned by an LRT holder, composed of base Ethereum staking rewards (consensus layer, MEV, execution fees) plus AVS operator fees paid by each Actively Validated Service the operator secures.

Restaking yield is not a single rate. It is a composite of streams that stack on top of each other, and the LRT holder earns the sum.

Layer 1: Ethereum staking rewards. Consensus layer rewards (historically 3-4% APY on ETH), MEV capture, and execution layer priority fees. This is the foundation, the same yield source as any LST. It exists whether or not a single AVS is live.

Layer 2: AVS operator fees. Each AVS the operator validates pays a fee for the security guarantee. The LRT protocol collects these fees and, after its own protocol take, distributes them to LRT holders. Fee rates vary by AVS because an active restaking market sets the price of security through supply and demand.

The LRT holder earns the base staking yield plus the aggregate of all AVS fees allocated to their position. In principle this looks like yield compounding. In practice it depends entirely on AVS adoption, fee rates, and allocation efficiency.

That dependency is the bootstrapping problem. Early-stage restaking protocols face a hard reality: AVS fees are negligible when few AVSes have launched. The yield story is partially prospective. The design principle is blunt. Do not build tokenomics that depend on AVS yield materializing before the AVSes are live.

This is where revenue-first design applies to restaking. The yield stack is the protocol's revenue model. If AVS fees don't materialize at the rate the yield model assumes, the LRT's value proposition collapses back to plain staking yield, which the LST market already delivers more efficiently and with one fewer layer of risk.

#The LRT Fee Architecture: How Protocol Fees Layer Across Restaking

Restaking fee architecture: the multi-layer fee structure of a liquid restaking protocol, comprising the underlying staking protocol fee, the AVS-to-operator fee split taken by the restaking marketplace, and the LRT protocol's own fee on aggregate yield distributed to holders.

The fee structure is the tokenomics. An LST has a single fee layer. An LRT protocol may have fees at two or three levels, and each layer takes a cut before the holder sees yield.

The stack has three tiers. First, the underlying staking protocol fee, for example a fee on consensus rewards taken by the LST the protocol restakes. Second, the AVS fee split between the operator and the restaking protocol. Third, the LRT protocol's own fee on aggregate yield. Stacking fees this way means LRT holders receive a smaller fraction of total generated yield than the gross rate suggests.

The fee split is the central tokenomics variable. How the protocol allocates AVS fees between node operators, the treasury, and LRT holders determines whether the system holds together. Allocate too much to treasury and operator incentives thin out. Allocate too much to operators and the treasury can't fund a credible slashing reserve. As a design reference, Ether.fi's eETH routes 90% of protocol revenue to stakers and 10% to the protocol treasury (Source: Ether.fi documentation). That is a mechanism description, not an endorsement.

The tradeoff: stacked fees create a drag the depositor often can't see. The design principle is to publish effective net yield, not gross yield. A protocol that shows depositors the gross stack (base staking plus all AVS fees before any fee take) without disclosing what lands after every layer is setting up a trust collapse when the real number surfaces.

The LRT market may also inherit the LST market's fee-compression dynamic, where protocols compete on yield by cutting their take. Establish a treasury floor before competing on yield. The governance token's most important job is often controlling these fee parameters, which is the structural use case that gives the token non-speculative demand.

For how fee extraction interacts with holder incentives across protocol types, the token velocity post covers the adjacent dynamics.

#Slashing Risk Architecture: When Multiple AVSes Create Correlated Risk

AVS slashing risk: the probability and magnitude of collateral loss imposed on a restaker by an Actively Validated Service's slashing conditions. In a multi-AVS restaking position, slashing events from independent AVSes can occur simultaneously, creating correlated loss exposure that is not simply additive.

Operator concentration: the degree to which a small number of node operators dominate AVS validation within a restaking marketplace. High operator concentration amplifies correlated slashing risk because a shared client bug or operational failure can trigger simultaneous slashing across multiple AVSes validated by the same operators.

This is the defining risk-design problem in LRT tokenomics. The same staked capital is exposed to slashing conditions from multiple independent protocols at once. No competitor covers this at mechanism depth, so spend the attention here.

Slashing in restaking is not simply additive. Each AVS has independent slashing conditions. An operator can be slashed by AVS-A and AVS-B simultaneously for unrelated failures. This is multi-vector exposure, not a summed probability you can average away.

The independence assumption is where designs break. Restaking protocols often model AVS slashing events as independent and uncorrelated. In practice, a validator client bug affecting consensus behavior can also affect validation duties for multiple AVSes running on the same client. That produces correlated slashing risk the independence model never priced in.

LRT protocols design for slashing through a few mechanisms:

Operator bond model. Operators post collateral (ETH, the protocol's native token, or other assets) that gets slashed before LRT holder capital is touched. This is analogous to Rocket Pool's RPL bond, applied to restaking (Source: Rocket Pool documentation, validator collateral specifications).

Insurance reserve. The protocol accumulates a reserve funded by protocol fees that absorbs slashing events below a defined threshold.

AVS slashing caps. Some protocols cap the maximum slashable percentage per AVS exposure, limiting the worst-case loss from any single AVS.

AVS vetting criteria. Not every AVS is an equal security obligation. Vetting AVS slashing conditions before whitelisting is a governance function with direct tokenomics consequences.

There is one risk unique to restaking: operator concentration. If a small set of large operators dominates AVS validation, a client bug hitting those operators at once creates outsized systemic risk. It is the validator client concentration problem from Ethereum's base layer, moved one level up the stack.

The design principle is simple to state and expensive to honor. An LRT protocol's slashing reserve is not optional. It is the premium payment for the yield stack the protocol promises. The higher the AVS yield target, the larger the reserve needed to back that promise credibly. Whether any specific protocol's reserve is adequate is a fact-specific analysis, not a label.

#The Governance Token in LRT Protocols: What It Must Control

LRT protocols typically run a governance token alongside the LRT itself. What that token controls determines whether it has durable demand or is a speculative overlay.

An LRT governance token typically controls the AVS whitelist (which services operators may validate), operator selection and vetting criteria, fee parameters (protocol rate, treasury allocation, operator split), insurance reserve size and trigger thresholds, and protocol upgrade authorization. The list looks similar to an LST governance token's until you reach the first item.

AVS whitelist control is the key structural demand driver. A governance token that decides which AVSes operators can validate controls the supply of security to the restaking market. That is a chokepoint with real economic weight. If AVS onboarding is governance-gated, governance holders sit on a lever the market actually needs.

Contrast that with a governance-only token. If all the token does is vote on fee parameters, its intrinsic value is the present value of that parameter range. Adjusting a fee by 0.5% is not value capture. That's a voting widget.

Some LRT protocols require operators to hold and stake the governance token as collateral, the same alignment Rocket Pool builds with RPL. That creates mandatory demand from operators rather than speculative demand from governance participants. The lesson: governance token value should be structural, anchored to a critical chokepoint, not yield-additive. A token that also pays a revenue share through buybacks or dividends just competes with the LRT itself on yield.

For the broader structural-demand question, a tokenomics audit checklist covers the dimensions used to separate durable governance token designs from speculative ones.

#LRT Tokenomics vs. LST Tokenomics: Key Design Differences

The LRT builds on the LST design pattern, but every dimension of complexity is amplified. This is the quick-reference for a builder deciding which problem they are actually signing up for.

| Dimension | LST Design | LRT Design |

|---|---|---|

| Security obligations | One (Ethereum consensus) | Multiple (Ethereum plus N AVSes) |

| Slashing vectors | One | Multiple, potentially correlated |

| Yield sources | Staking base (consensus, MEV, fees) | Staking base plus AVS fees |

| Fee layers | One (staking protocol fee) | Two to three (staking, AVS, LRT protocol) |

| Token model | Rebasing or exchange-rate | Primarily exchange-rate |

| Governance function | Fee params, validator set, treasury | Plus AVS whitelist, operator criteria, slashing caps |

| Insurance reserve complexity | Medium (one vector) | High (multiple, potentially correlated vectors) |

| Composability complexity | Moderate | High (balance must stay stable for DeFi) |

Read down the right column and the pattern is consistent: yield composition is multi-layered, slashing risk is multi-vector, governance decisions are more consequential, and fee transparency is harder to achieve. An LRT makes design sense when you are building on mature restaking infrastructure with a live AVS ecosystem paying real fees, and your team has the operational capacity to vet and monitor AVSes continuously. It does not make sense when you are designing tokenomics around future AVS yields that don't exist yet, shipping a governance token with no structural utility, or operating without the monitoring infrastructure for multi-AVS slashing conditions.

#Common LRT Tokenomics Mistakes

After working through the mechanism design on dozens of DeFi protocol engagements, the failure patterns in restaking are predictable.

Yield promises based on un-launched AVS fees. Marketing an LRT yield rate that includes projected AVS fees before those AVSes are operational. The protocol delivers plain staking yield, the gap between promised and real destroys trust, and the LST market was already delivering that base yield more cleanly. If the AVS fees aren't live, don't put them in the number you show depositors.

No slashing reserve with multi-AVS exposure. Routing all protocol fee to governance token buybacks and treasury marketing while holding no insurance reserve for multi-AVS slashing. The first correlated slashing event breaks the LRT peg, and a peg break is not a recoverable NAV adjustment.

Governance token with no structural demand driver. Launching a governance token that votes only on minor fee parameters, with no control over the AVS whitelist or operator onboarding. Non-speculative demand is near zero. A governance token that controls the AVS whitelist controls the supply of security to the market. A token that votes on a 0.5% fee adjustment does not.

Fee opacity, presenting gross yield instead of net. Showing depositors the gross stack (base staking plus all AVS fees before any fee take) without disclosing the net yield after the LRT protocol fee, the operator fee, and the underlying staking fee. Protocols competing on apparent yield set up a trust collapse the moment real yields are revealed.

Operator concentration with no diversity incentive. Letting a few large operators dominate AVS validation with no tokenomics incentive for operator diversity, such as a bonus rate for operators below a concentration threshold. This replicates Ethereum's validator client concentration risk one level up the stack, and the correlated slashing it invites is exactly what the reserve was supposed to prevent.

#How to Evaluate an LRT Protocol's Tokenomics

We use what we call the LRT Design Evaluation Framework to assess a liquid restaking protocol's tokenomics. Six questions structure the review.

What is the yield composition? What percentage comes from base staking versus AVS fees, and are those AVS fees live and verifiable onchain, or projected? A protocol that can't separate the two is selling a forecast as a yield.

What is the full fee stack? What is the depositor's effective net yield after every fee layer, staking protocol, AVS split, and LRT protocol fee included?

How is multi-AVS slashing risk managed? What is the insurance reserve size relative to maximum slashable exposure, and is the operator bond model documented?

What does the governance token control? Is AVS whitelist approval governance-gated? Do operators hold the governance token as mandatory collateral, or is it a voting widget?

What is the operator concentration? What percentage of AVS validation sits with the top-5 operators, and is client diversity tracked and incentivized?

What are the onchain slashing conditions for each whitelisted AVS? Are they documented in governance forums with audit references, or asserted in a marketing deck?

If you need a systematic review of your full restaking token model, the complete data room is where that work gets done.

#Frequently Asked Questions

How does LRT tokenomics differ from LST tokenomics?

LRT tokenomics adds two dimensions that LST tokenomics does not have: multi-AVS yield composition and multi-vector slashing risk. An LST manages one security obligation (Ethereum consensus) with one yield source and one slashing vector. An LRT manages multiple simultaneous security obligations, each with independent slashing conditions, stacking AVS operator fees on top of base staking yield while exposing the holder to correlated slashing risk across all those obligations.

What is restaking yield and how is it calculated?

Restaking yield is the composite return earned by an LRT holder from two sources: base Ethereum staking rewards (consensus layer rewards, MEV, and execution fees, historically 3-4% APY on ETH) plus AVS operator fees paid by each Actively Validated Service the operator secures. The LRT holder earns the sum after the LRT protocol takes its own fee layer. Because AVS fee rates vary by service and depend on market-driven security pricing, restaking yield is not a fixed rate and changes as AVS adoption and fee levels shift.

What happens if an AVS slashes and there is no insurance reserve?

If a whitelisted AVS triggers slashing and the LRT protocol holds no insurance reserve, the slashing loss propagates directly to LRT holders through a reduction in the exchange rate of the token. In a multi-AVS exposure where correlated slashing events hit simultaneously, this can cause the LRT to break its peg against the underlying staked ETH value. A peg break is not a recoverable NAV adjustment in liquid markets: it triggers redemption pressure and may cascade into insolvency if slashing exposure exceeds liquid reserves.

Can an LRT protocol be slashed across multiple AVSes at once?

Yes. Each AVS operates independent slashing conditions, so an operator can face simultaneous slashing from multiple AVSes for unrelated failures in the same block. More significantly, a shared validator client bug can trigger failures across every AVS that operator validates simultaneously, converting what looks like independent risk into correlated exposure. This is the independence assumption failure that LRT slashing reserve sizing must account for.

How do you evaluate whether an LRT governance token has real value?

Ask what the token controls. A governance token with structural value sits on a chokepoint the market depends on: typically the AVS whitelist (which services operators may validate) and operator onboarding criteria. If AVS onboarding is governance-gated, token holders control the supply of security to the restaking market, which is a lever with real economic weight. A token that only votes on fee parameters in the 0.1-0.5% range has near-zero non-speculative demand. Additional structural demand comes from protocols that require operators to hold and stake the governance token as mandatory collateral.

What is the bootstrapping problem in LRT tokenomics?

Early-stage LRT protocols face a yield gap: AVS fees are negligible when few AVSes have launched and secured commitments from operators. The yield stack is partially prospective, dependent on future AVS adoption materializing at the rates the token model assumes. A protocol that markets an LRT yield rate that includes projected, un-launched AVS fees is selling a forecast as a real yield. When AVS fees fail to materialize on schedule, the LRT delivers plain staking yield, which the LST market already provides more efficiently and with fewer risk layers.

How should fee transparency work in an LRT protocol?

LRT protocols should publish the effective net yield after every fee layer, not the gross yield stack. The relevant disclosures are: the underlying staking protocol fee taken on consensus rewards, the AVS-to-operator fee split and the restaking marketplace's cut, and the LRT protocol's own fee on aggregate distributed yield. The depositor's real return is the gross yield stack minus all three layers. Protocols that display only the gross stack set up a trust collapse when depositors calculate the actual number themselves.

#Conclusion: LRT Tokenomics Is Protocol Risk Architecture

LRT tokenomics is not yield optimization. It is multi-layer risk architecture. The yield is the product, and the tokenomics is the engineering that determines whether that product is sustainable or just a louder version of plain staking.

The complexity premium is real. LRT design demands more than LST design because the surface area for error is larger. Yield promises, slashing reserves, fee stacking, governance token structural demand, and operator diversity all interact, and a weak link in any one of them propagates. The category is still early. The TVL is significant and growing, but the design patterns are not mature. Get the fundamentals right, and the protocol holds up when institutional capital looks under the hood.

If you're building an LRT protocol and need the tokenomics to hold up under institutional scrutiny, yields that are accurate, slashing reserves that are sized right, and a governance token that carries structural value, book a discovery call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.