Stablecoin Design From First Principles: Mechanisms and Regulatory Fit

Mechanism-by-mechanism breakdown of stablecoin design: fiat-backed, crypto-collateralized, and algorithmic, with MiCA compliance analysis for protocol teams and fintech builders.

Stablecoin design is the discipline of selecting and configuring the peg mechanism that keeps a token's value anchored to a reference asset, typically a fiat currency, a basket of assets, or a commodity. The mechanism you choose determines your reserve obligations, your regulatory classification, your revenue model, and your capital efficiency profile. Get it right and you have an asset that circulates. Get it wrong and you have a compliance liability that no amount of marketing can fix.

This post walks through the three primary stablecoin mechanism types, how they compare on the dimensions that matter to protocol teams and fintech builders, and the design variables each mechanism requires you to resolve before you write a single line of smart contract code. It builds on the stablecoin design fundamentals overview published earlier this year.

MiCA (Markets in Crypto-Assets) enforcement is at its peak window right now. For any team issuing a stablecoin with EU distribution, mechanism selection is not a product decision. It is a regulatory classification decision.

#Why Stablecoin Design Is a Business Decision, Not a Technical One

Most teams approach stablecoin design as an engineering problem. The right framing is a business problem. The mechanism you select determines three things that have nothing to do with code.

First, it determines who holds the reserves and what liability that creates for your organization. A fiat-backed reserve held by a regulated custodian creates banking relationships, audit obligations, and jurisdictional licensing requirements. A crypto-collateralized mechanism shifts that liability on-chain, where liquidation mechanics and oracle dependencies carry their own failure modes.

Second, it determines what regulatory classification your stablecoin receives in each market where it circulates. In the EU, MiCA's Article 3 creates a hard bifurcation between E-Money Tokens (EMTs) and Asset-Referenced Tokens (ARTs). The mechanism you build determines which category you land in, and the two categories carry materially different regulatory burdens. There is no post-hoc reclassification.

Third, it determines your revenue model. Stablecoins are not neutral infrastructure. Every viable stablecoin design generates revenue through a mechanism that must be deliberately built in, whether that is yield on reserves, stability fees on minted supply, or protocol fees on transactions. Teams that treat the revenue model as an afterthought discover after launch that their circulating supply generates insufficient protocol income to sustain operations.

Three questions frame every stablecoin design engagement we run:

- Who holds the reserves, and what liability does that create for your entity?

- What jurisdictions will the stablecoin circulate in at launch, and what licenses do those require?

- What is your revenue model at launch-day circulating supply, and at what scale does it become self-sustaining?

The mechanism follows from the answers. Teams that select mechanism before answering these questions build designs that require re-engineering inside twelve months.

#The Three Stablecoin Mechanism Types: A Classification Framework

We use a three-mechanism classification framework when advising stablecoin teams. Every viable stablecoin design maps to one of these types, or to a hybrid that blends elements of two. The hybrid category is rarer than most teams assume; most of what teams call "hybrid" is either fiat-backed with some crypto reserve exposure or crypto-collateralized with an algorithmic rate-adjustment layer.

#Fiat-Backed Stablecoins (Full-Reserve Model)

A fiat-backed stablecoin maintains its peg through 1:1 reserves of fiat currency or near-equivalent instruments held by a regulated custodian. Each token in circulation represents a direct claim on those reserves. Redemption, the conversion of tokens back to fiat, is the peg mechanism. When the market price deviates from par, arbitrage between the secondary market and the redemption process restores equilibrium.

Capital efficiency: Lowest of the three types. Every token requires 100% backing. There is no leverage, no fractional reserve, no algorithmic supply adjustment.

Revenue model: Yield on reserve assets. The issuer earns interest on the underlying reserves (Treasury bills, overnight repos, money market instruments) while token holders receive no yield. This is the Circle/USDC model. At scale, yield on reserves can be material. At launch-day circulating supply of tens of millions, revenue is modest.

Regulatory classification under MiCA: E-Money Token (EMT), regulated under MiCA Title III. EMTs are the lighter regulatory burden of the two MiCA stablecoin categories. Requirements include reserve asset composition standards, redemption at par within specific timeframes, independent custody obligations, and a regulatory whitepaper filing. EMTs issued in volume above 5 million EUR in average outstanding tokens per day face enhanced requirements.

Best fit: Payment-focused projects with existing banking relationships, regulated fintech operators with MSB licensing in target jurisdictions, institutional settlement use cases requiring regulatory certainty.

Primary examples: USDC (Circle), USDT (Tether), EURS (Stasis). These are mechanism descriptions; individual projects carry their own audit and compliance status.

Key design variables inside this category:

- Reserve composition. Cash equivalents carry no yield but maximum safety. Short-duration T-bills generate yield but carry mark-to-market exposure. Mixed reserves require a clear policy statement and independent attestation.

- Attestation vs. audit. Attestation by a named firm (Grant Thornton, Deloitte) at defined frequency (monthly, quarterly) is the market standard. Full audit is more defensible but significantly more resource-intensive.

- Redemption queue design. FIFO queues are operationally straightforward. Tiered queues (institutional vs. retail) allow larger redemptions to settle without depleting retail reserves. The design choice has operational and legal implications that must be resolved before launch.

#Crypto-Collateralized Stablecoins (Over-Collateral Model)

A crypto-collateralized stablecoin maintains its peg through on-chain collateral deposits above 100% of the minted stablecoin supply. Borrowers lock crypto assets (ETH, wBTC, or approved collateral assets) in a smart contract vault, mint stablecoins against that collateral up to the permitted collateralization ratio, and pay a stability fee (interest rate) on outstanding supply. If collateral value drops below the liquidation threshold, the position is automatically liquidated to protect the peg.

Capital efficiency: Medium. Typical collateralization ratios run 150% to 200%. For every $150 to $200 in collateral, the protocol mints $100 in stablecoins.

Revenue model: Stability fee. The protocol earns interest on all outstanding stablecoin supply. MakerDAO, the reference implementation of this model, earned protocol revenue in the hundreds of millions in 2023 from stability fees across its DAI supply (Source: MakerDAO governance forum, MIP65 financial report series). For on-chain tracking of stablecoin supply and circulating metrics, the RWA.xyz on-chain RWA tracker provides real-time data across major tokenized asset categories.

Regulatory classification under MiCA: Asset-Referenced Token (ART), regulated under MiCA Title IV. ARTs carry the heavier regulatory burden. Requirements include reserve asset holding by independent custodians, enhanced whitepaper obligations, significant capital requirements for issuers, and in some cases prior authorization from the national competent authority before issuance.

Best fit: DeFi-native protocols that cannot establish banking relationships with regulated custodians; teams targeting on-chain liquidity provisioning; protocols where censorship-resistance and decentralization are primary design goals.

Primary example: DAI (MakerDAO, now USDS in its current iteration). Mechanism description only.

Key design variables inside this category:

- Collateralization ratio. Higher ratios increase peg stability but reduce capital efficiency and make the stablecoin less attractive to borrowers. Most implementations use tiered ratios by collateral risk profile.

- Liquidation mechanics. Who can trigger liquidations, at what threshold, and what penalty applies to the liquidated borrower. Poorly designed liquidation mechanics create death-spiral risk when collateral prices fall rapidly.

- Oracle dependency. The protocol depends entirely on price feed accuracy. Oracle manipulation or failure can trigger mass liquidation events. Multi-oracle architectures and circuit breakers are standard risk mitigations.

#Algorithmic and Hybrid Stablecoins

Algorithmic stablecoins attempt to maintain their peg through supply expansion and contraction managed by an algorithm rather than through collateral reserves. When the price rises above the peg, the protocol mints new supply and distributes it, pushing price down. When price falls below the peg, the protocol burns supply or incentivizes buying, pushing price up.

The mechanism sounds elegant. In practice, it carries a failure mode that the market has demonstrated at scale.

Capital efficiency: Highest. No reserve requirement in pure algorithmic designs.

Regulatory classification under MiCA: MiCA Article 19 requires that ART issuers hold a reserve of assets backing the tokens. Uncollateralized algorithmic stablecoins are functionally incompatible with MiCA's ART framework. Pure algorithmic designs face a near-total barrier to EU distribution under current regulation.

The Terra/Luna case. In May 2022, TerraUSD (UST) lost its peg in a liquidity crisis that destroyed approximately $45 billion in combined market capitalization of UST and LUNA within 72 hours. The mechanism failure was specific: UST's peg relied on demand for LUNA, a sister token whose value was itself speculative. When confidence in the system fell, the mechanism that was supposed to defend the peg accelerated the collapse. The lesson is not "algorithmic stablecoins never work." The lesson is that any peg mechanism whose stabilization depends on speculative demand for another asset has a single point of failure that compounds in a liquidity crisis.

Hybrid designs. Hybrid models layer partial collateral with algorithmic supply adjustment. Frax is the reference implementation: partial fiat-backed reserves with an algorithmic supply mechanism managing the uncollateralized portion. Hybrid designs can thread the needle between capital efficiency and stability if the collateral ratio is managed conservatively and the algorithm's incentive structure holds under stress.

Best fit: Narrow use cases, primarily on-chain DeFi contexts where regulatory exposure is managed at the application layer rather than the protocol layer. Not recommended for projects seeking institutional adoption or EU distribution.

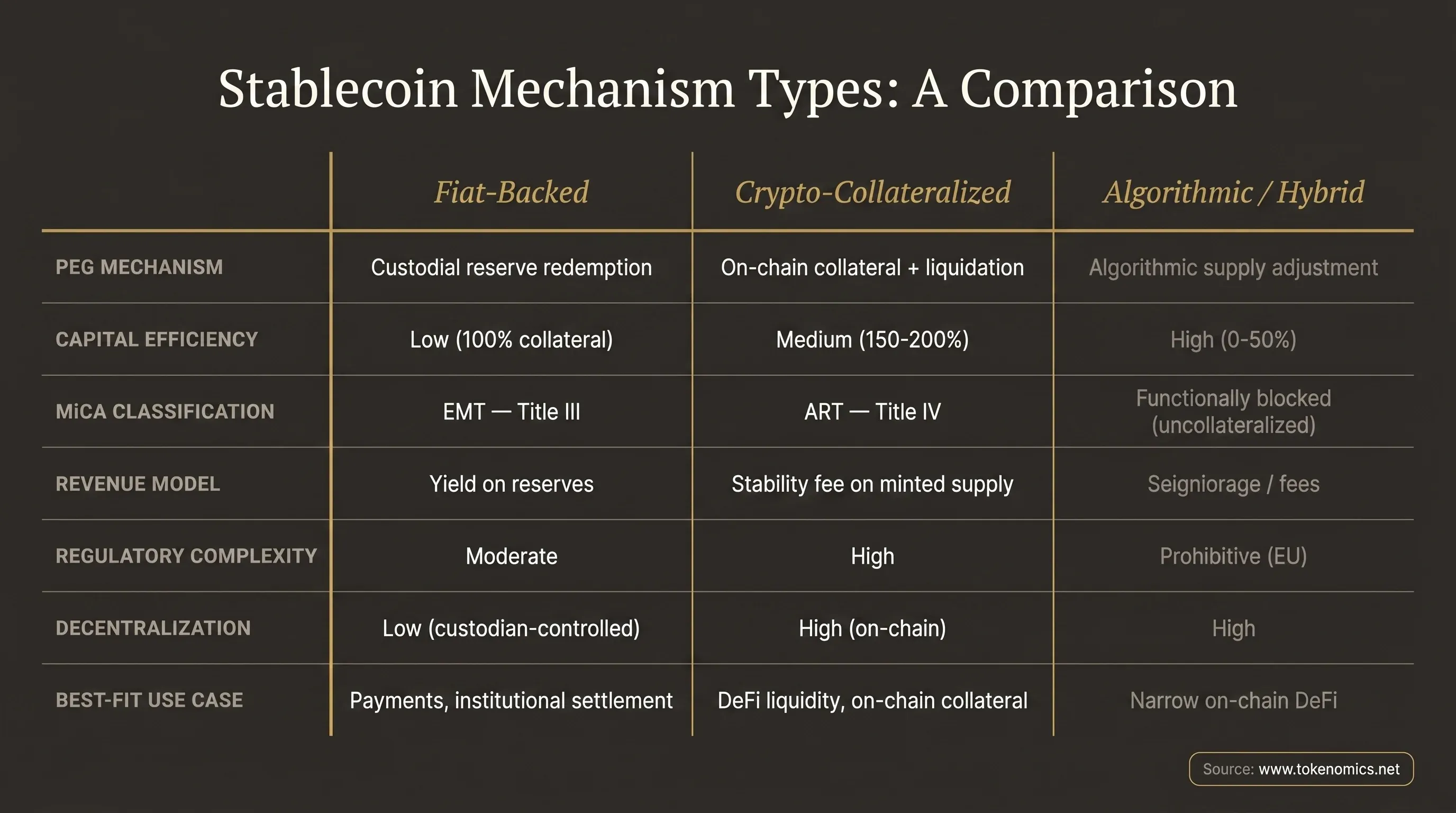

| Design Dimension | Fiat-Backed | Crypto-Collateralized | Algorithmic / Hybrid |

|---|---|---|---|

| Peg mechanism | Custodial reserve redemption | On-chain collateral + liquidation | Algorithm-driven supply adjustment |

| Capital efficiency | Low (100% collateral) | Medium (150-200%) | High (0-50% collateral) |

| Decentralization | Low (off-chain custodian) | High (on-chain vaults) | High |

| MiCA classification | EMT (Title III, lighter burden) | ART (Title IV, heavier burden) | Functionally blocked (uncollateralized) |

| Revenue model | Yield on reserves | Stability fee on minted supply | Seigniorage / fee mechanisms |

| Regulatory complexity (EU) | Moderate | High | Prohibitive |

| Best-fit use case | Payments, institutional settlement | DeFi liquidity, on-chain collateral | Narrow on-chain DeFi |

| Banking relationship required | Yes | No | No |

#Regulatory Fit: MiCA, the US Framework, and What They Require of Your Design

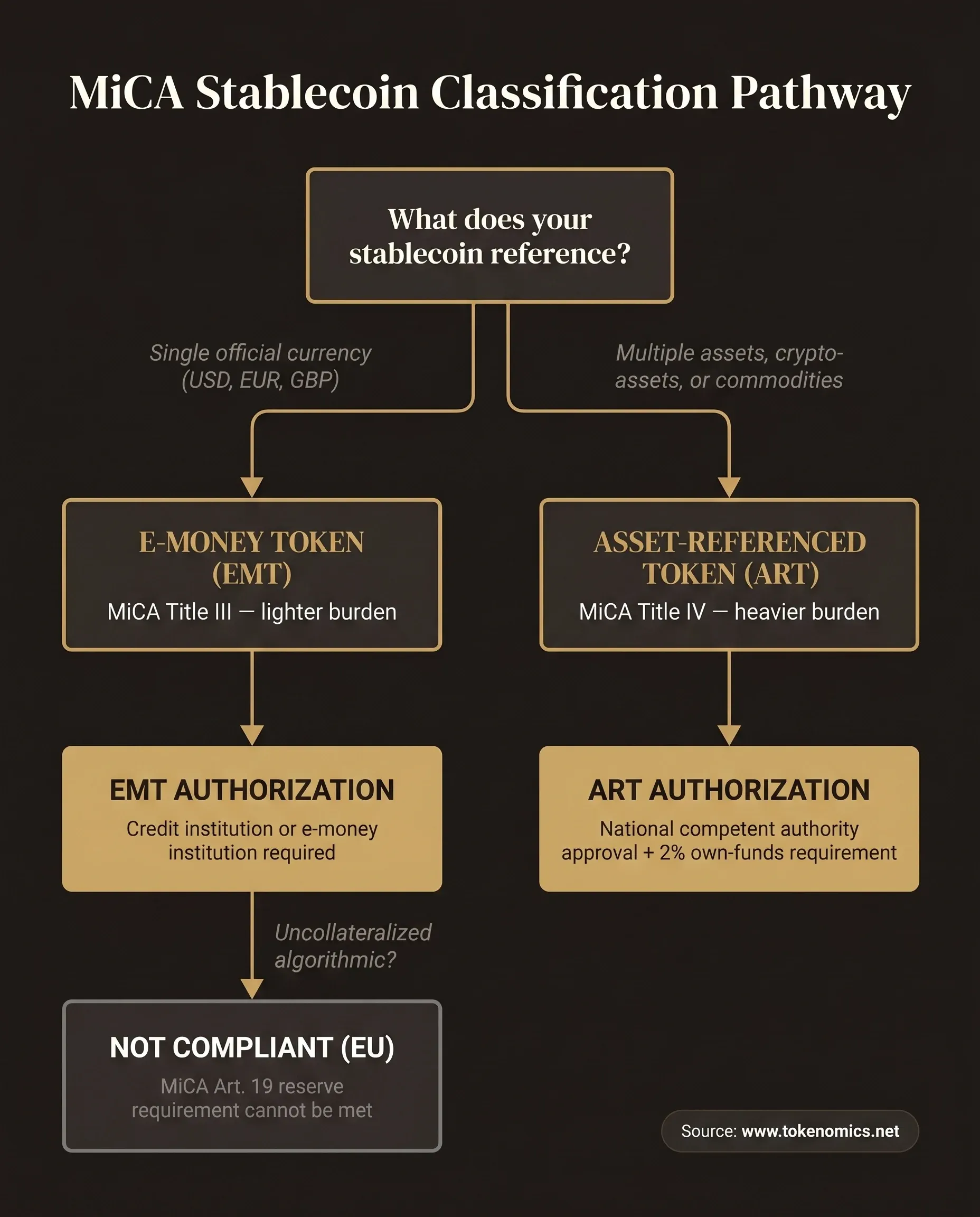

The regulatory question is not theoretical for 2026 issuers. MiCA enforcement began in June 2024 for crypto-asset service providers and December 2024 for stablecoin issuers. Projects with EU distribution that have not completed their regulatory classification analysis are operating under enforcement risk today.

MiCA stablecoin classification. MiCA creates two regulated stablecoin categories:

-

E-Money Tokens (EMTs) reference a single official currency. They are regulated under Title III. EMT issuers must be authorized credit institutions or electronic money institutions in an EU member state. Reserve assets must be held in highly liquid, low-risk instruments. Redemption at par within one business day is required. Monthly reporting to the national competent authority is required above the 5 million EUR threshold.

-

Asset-Referenced Tokens (ARTs) reference multiple assets, commodities, or crypto-assets. They are regulated under Title IV. ART authorization requirements are more extensive: a regulatory whitepaper reviewed by the national competent authority, reserve asset custody by independent custodians, a minimum own-funds requirement of 2% of average outstanding token value (or 3% for significant ARTs), and ongoing reporting obligations.

The mechanism-to-classification mapping is direct. Fiat-backed stablecoins referencing a single currency land as EMTs. Crypto-collateralized stablecoins land as ARTs. Algorithmic stablecoins without collateral backing cannot satisfy MiCA's reserve requirements.

US regulatory context. The US does not yet have a federal stablecoin framework as of June 2026. The SEC continues to evaluate stablecoin classification on a case-by-case basis under existing securities law authority. The STABLE Act has been in committee without resolution. OCC guidance has addressed bank participation in stablecoin activities without creating a unified issuance framework. State-level money transmitter licenses remain the operational path for most US stablecoin issuers. This is a fluid environment; any US regulatory statement in this post should be verified against current guidance.

Singapore context. The Monetary Authority of Singapore (MAS) has finalized its stablecoin regulatory framework under the Payment Services Act. Single-currency stablecoins pegged to the SGD or any G10 currency, with circulation above SGD 5 million, require licensing as a Major Payment Institution and must hold 100% of outstanding value in low-risk liquid assets.

The design implication across all three jurisdictions: fiat-backed designs have the clearest and most achievable regulatory path. Crypto-collateralized designs face material regulatory burden in the EU, uncertainty in the US, and limited framework recognition in Singapore. Algorithmic designs without collateral are functionally blocked in the EU and face severe credibility barriers in any institutional context. For a broader treatment of how mechanism choices interact with post-FIT-21 regulatory requirements, see our post on tokenomics compliance requirements.

Whether your specific design meets the requirements in any specific jurisdiction is an analysis for your legal team, not a characterization this post can provide. We design stablecoin mechanisms with compliance review in mind; the compliance determination is made by counsel and the relevant regulator.

#Reserve Design: The Decisions Inside the Fiat-Backed Model

For teams that have selected fiat-backed as their mechanism, reserve design is where the complexity lives. The peg mechanism itself is straightforward. The reserve composition, custody, attestation, and redemption architecture require deliberate design decisions, and each decision has regulatory and financial implications.

Reserve composition options:

- Cash in bank accounts. Maximum liquidity, zero market risk. Revenue: minimal (near-zero deposit rates at scale). Regulatory treatment: most direct. Risk: bank failure and deposit insurance limits.

- Short-duration US Treasury bills. Low market risk, predictable yield (approximately 5.0-5.3% as of late 2025), high liquidity in normal markets. Risk: mark-to-market exposure in rate environments, settlement timing.

- Money market funds (government-only). SEC-regulated, daily liquidity, modest yield. Circle's USDC reserve composition has historically included significant money market fund allocation. Ondo Finance tokenized treasury products represents the institutional-grade model of reserve composition transparency applied to tokenized yield-bearing assets.

- Mixed reserve. A policy-specified blend across cash, T-bills, and money market instruments. Requires a published reserve policy and independent attestation against the stated composition.

Attestation cadence. Monthly attestations by a Big Four or top-tier regional firm are the market standard. Centrifuge on-chain credit markets is one example of a project that has published attestation-style reserve disclosures for tokenized real-world credit portfolios. Quarterly attestations are defensible for smaller issuers but will draw scrutiny from institutional partners. Annual attestations are not sufficient for a circulating stablecoin.

Redemption architecture. Every holder of your stablecoin has an implicit or explicit right to redeem for the reference fiat at par. The redemption design determines who can redeem (retail vs. institutional only), how quickly (same day vs. T+1 vs. T+2), and what the minimum redemption size is. Designs that restrict redemption to institutional clients must be disclosed clearly; retail holders must be able to access secondary market liquidity or a retail redemption channel.

SPV structure. Bankruptcy-remote structuring of the reserve through a special purpose vehicle (SPV) protects holders from issuer insolvency. This is the institutional-grade standard. It adds legal overhead but materially improves the risk profile that institutional partners and exchanges will accept.

#Common Design Mistakes We See

After advising projects across 80+ token design engagements, the failure patterns in stablecoin design are predictable. They are not unique to small teams. Some of the most expensive mistakes have been made by well-funded, technically sophisticated teams.

Selecting mechanism before resolving jurisdiction. A team builds a crypto-collateralized stablecoin targeting EU distribution without completing MiCA classification analysis. They discover six months before launch that ART authorization takes twelve to eighteen months and requires significant capital reserves. The mechanism redesign at that stage is a full project restart.

Treating reserve yield as certain revenue. Reserve yield depends on market interest rates, reserve composition, and circulating supply scale. A team projecting 5% yield on a $10M circulating supply at launch is projecting $500K in annual revenue, which barely covers compliance overhead. The revenue model for fiat-backed stablecoins is a scale game. The projections need to show the path to sustainable operations at the target circulating supply, not just the launch-day snapshot. The token distribution model post covers the supply-side mechanics that inform this analysis.

Underestimating the attestation cost and cadence requirement. Monthly attestations from a credible firm cost more than most teams budget, particularly in year one before the issuer has established a relationship with an audit firm that understands crypto reserve structures. Teams that budget for annual attestations and need to retroactively upgrade to monthly cadence face both cost and reputational disruption.

Building a hybrid design without modeling the stress scenario. Hybrid designs that rely on algorithmic supply adjustment for the uncollateralized portion are only as stable as the incentive structure that drives that adjustment. Teams that model the mechanism under normal conditions and not under a sustained liquidity drain discover the failure mode at the worst possible time.

Ignoring the oracle dependency in crypto-collateralized designs. A crypto-collateralized stablecoin that uses a single price oracle, or that uses oracles with slow update cadence, is exposed to oracle manipulation and to market gap-down events that outpace liquidation mechanics. Multi-oracle architectures with circuit breakers are not optional; they are the baseline design requirement.

#What to Ask Before Committing to a Mechanism

The questions below define the scope of a stablecoin design engagement. If your team cannot answer all of them before selecting a mechanism, the selection is premature.

-

What is the primary use case at launch? Payments and retail use cases favor fiat-backed. On-chain DeFi collateral use cases favor crypto-collateralized. The use case is not interchangeable with the mechanism; it constrains the viable mechanism set.

-

Which jurisdictions will the stablecoin circulate in during the first 12 months? EU distribution requires MiCA classification analysis before mechanism selection. US distribution requires state-by-state money transmitter analysis or a federal charter pathway analysis.

-

Does the team have existing banking relationships sufficient for fiat-backed reserve custody? If the answer is no, crypto-collateralized may be the only viable path regardless of preference. Most non-regulated fintech teams discover that establishing custodial banking relationships for a stablecoin is a 6 to 18-month process.

-

What is the circulating supply target at launch, and what revenue does the mechanism generate at that supply level? Run the revenue math before mechanism selection. If the mechanism does not generate sustainable protocol revenue at the expected launch-day supply, the business model requires rethinking.

-

What are the audit or attestation requirements, and what is the budget for year-one compliance overhead? Compliance overhead for a fiat-backed stablecoin with monthly attestations from a credible firm typically runs $200K to $500K per year in year one, before accounting for legal fees for ongoing regulatory monitoring.

-

Is censorship-resistance a core design requirement? If yes, fiat-backed designs are incompatible. A custodian-controlled reserve is, by definition, censorable. Crypto-collateralized designs on public blockchains offer genuine censorship-resistance, with the trade-offs in capital efficiency and regulatory classification that entails.

-

What is the stress scenario for the peg, and does the mechanism survive it? Every peg mechanism has a failure mode. The fiat-backed failure mode is custodian insolvency or withdrawal restrictions. The crypto-collateralized failure mode is collateral price collapse exceeding the liquidation mechanism's capacity to respond. The algorithmic failure mode is confidence collapse. Model all three before selecting mechanism.

#FAQ: Stablecoin Design

What is stablecoin design? Stablecoin design is the process of selecting and configuring the mechanism that maintains a token's peg to a reference asset. It covers reserve structure, collateralization ratios, liquidation mechanics, revenue model, and regulatory classification, and it determines the compliance path available to the issuer in each target jurisdiction.

What are the three types of stablecoins by mechanism? The three primary stablecoin mechanism types are fiat-backed (full-reserve), crypto-collateralized (over-collateral), and algorithmic. Fiat-backed stablecoins hold 1:1 reserves of fiat or near-equivalent instruments. Crypto-collateralized stablecoins require on-chain collateral deposits above 100% of minted supply, with automatic liquidation protecting the peg. Algorithmic stablecoins manage peg through supply expansion and contraction without a reserve requirement, though pure algorithmic designs carry structural fragility risk and face regulatory barriers in major jurisdictions.

What does MiCA require for stablecoin issuers? MiCA creates two stablecoin categories: E-Money Tokens (EMTs) and Asset-Referenced Tokens (ARTs). EMT issuers must be authorized credit institutions or e-money institutions in the EU, hold reserves in liquid low-risk assets, and redeem tokens at par within one business day. ART issuers face authorization requirements from the national competent authority, mandatory independent custody of reserve assets, minimum own-funds requirements, and enhanced reporting obligations. Uncollateralized algorithmic stablecoins cannot satisfy MiCA's reserve requirements under Article 19.

What is the difference between an EMT and an ART under MiCA? An EMT (E-Money Token) references a single official currency and is regulated under MiCA Title III, the lighter regulatory category. An ART (Asset-Referenced Token) references multiple currencies, commodities, or crypto-assets and is regulated under MiCA Title IV, the heavier regulatory category. Fiat-backed stablecoins pegged to a single currency land as EMTs. Crypto-collateralized stablecoins backed by multiple crypto-assets land as ARTs.

How do fiat-backed stablecoins generate revenue? Fiat-backed stablecoin issuers earn yield on the reserve assets (T-bills, money market funds, repos) that back circulating supply. Token holders receive no yield. The revenue model is fundamentally a scale game: yield on $100M in reserves at 5% generates $5M annually; yield on $1B in reserves at the same rate generates $50M. Revenue is modest at launch-day supply levels typical of new projects.

Is an algorithmic stablecoin legal in the EU? MiCA's reserve requirement effectively prohibits uncollateralized algorithmic stablecoins from circulating in the EU as regulated stablecoins. A stablecoin without backing assets cannot satisfy MiCA's reserve-holding requirements for ARTs. Hybrid designs with partial collateral may be able to satisfy ART requirements if the collateralized portion meets the reserve standards, but this is a jurisdiction-specific legal analysis, not a general characterization.

How much collateral does a crypto-collateralized stablecoin require? Collateralization ratios for crypto-collateralized stablecoins typically run from 150% to 200% of the minted stablecoin value, depending on the collateral asset's volatility profile. Highly volatile collateral assets require higher ratios to provide a buffer against rapid price declines before the liquidation mechanism can respond. Conservative designs use tiered ratios by collateral type, with higher-volatility assets requiring higher collateralization.

What is a stablecoin reserve attestation? A reserve attestation is an independent verification by a third-party firm (typically an accounting firm) that confirms the issuer's stated reserve composition is accurate at a point in time. It differs from a full audit: an audit provides assurance over financial statements, while an attestation provides assurance over a specific factual assertion (the reserve balance and composition). The market standard for circulating stablecoin issuers is monthly attestations published publicly. Circle, for USDC, uses Grant Thornton for monthly attestations.

The expectations for stablecoin design have risen sharply since MiCA enforcement began. Mechanism selection that made sense in 2021 may require revisiting in 2026. Projects that completed their mechanism analysis in a pre-MiCA environment and have not updated that analysis since are operating on potentially stale assumptions about their regulatory classification.

If your team is working through mechanism selection and needs the design to hold up under institutional and regulatory scrutiny, book a strategy call. If you need an independent review of an existing mechanism before launch, our tokenomics audit process covers every dimension we evaluate. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.