DePIN Tokenomics: The Mechanism Design Framework

DePIN tokenomics mechanism design framework: operator unit economics, emission scheduling, demand-side revenue transition, and vertical-specific token design.

DePIN tokenomics is the mechanism design discipline for token incentive systems that coordinate real-world hardware through cryptographic rewards. A sound DePIN token model must resolve five design variables: operator unit economics, emission schedule, proof-of-work mechanism, demand-side revenue transition, and governance design. Getting any of these wrong produces a predictable failure sequence that the DePIN sector has already seen play out across dozens of protocols.

DePIN stands for decentralized physical infrastructure networks. These protocols coordinate real-world hardware operators through token rewards, spanning wireless coverage (Helium), distributed compute (Render, NOSANA), distributed energy (Glow, Arkreen), mobility and mapping (Hivemapper), and environmental sensing. The tokenomics design problem these protocols face is structurally different from anything in DeFi. Node operators are not liquidity providers with zero marginal cost. They are running physical equipment with real capital costs, real operating expenses, and real exit barriers. DePIN tokenomics design requires a framework built for that cost structure, not borrowed from liquidity mining.

The failure mode is predictable: front-loaded emissions attract hardware deployers who collect rewards, dump tokens, and exit the moment yields compress. What remains is empty infrastructure with no demand side and no token supply capable of attracting replacements. If you're building a DePIN protocol and need the tokenomics to hold up before you lock in supply architecture, book a strategy call before the emission schedule is committed to a smart contract.

This post walks through the five design decisions and what getting each one right actually looks like in practice.

#What Makes DePIN Tokenomics Different from DeFi Tokenomics

Most founders reach for the DeFi playbook when designing DePIN incentives. That doesn't work.

A DeFi liquidity provider allocates capital with zero physical friction. Moving liquidity from one pool to another takes one transaction. A DePIN node operator allocates physical capital: $400 to $2,000 in hardware, connectivity infrastructure, power, and the time required to configure and maintain the node. Exit costs are real. If yields compress faster than the demand side develops, the operator takes a loss on hardware they cannot redeploy elsewhere.

Three design constraints separate DePIN from DeFi tokenomics.

Physical capital commitment. DePIN operators make irreversible capital decisions before token income arrives. Hardware must be purchased, configured, and deployed before the first reward. The incentive design must account for this pre-commitment cost structure.

Geographic coverage requirements. DePIN protocols require physical presence in specific locations. A liquidity pool does not care where capital comes from. A wireless coverage network does. This creates coverage gap problems that tokenomics must solve through variable reward rates by geography.

Service delivery proof before reward. DePIN operators prove contribution through Proof-of-Coverage (PoC) or service-delivery verification before earning rewards. A DeFi LP proves capital commitment through the protocol's smart contract state. Designing PoC mechanisms that are both verifiable and gaming-resistant is a distinct engineering challenge with direct tokenomics implications.

The DePIN sector passed $20 billion in projected market value in 2024, with over 650 active protocols across compute, wireless, energy, and sensing categories (Source: Messari DePIN Sector Report, 2024). Most of those protocols are in bootstrap phase. Most of them are applying frameworks designed for a different incentive landscape. The ones that adapt the design to the physical infrastructure cost structure from the start are the ones that survive compression.

#The Five Design Decisions Every DePIN Token Model Must Resolve

We use what we call the Five-Variable DePIN Design Framework. Every DePIN token model must resolve each of these five decisions or leave them to chance. Chance is not a mechanism.

Decision 1: Operator unit economics. What does it cost to run a node for 12 months, and what yield makes deployment rational at launch? This is the floor calculation. Every other design variable depends on it.

Decision 2: Emission schedule. How much token supply is allocated to operator rewards, and at what release rate over what time horizon? The schedule must be long enough to cover the bootstrap period, tight enough to avoid catastrophic dilution, and flexible enough to respond to demand-side development.

Decision 3: Proof-of-work mechanism. How does the protocol verify that operators are providing genuine infrastructure contribution? And what gaming vectors does the mechanism close? A PoC mechanism that can be gamed destroys the incentive design from the inside.

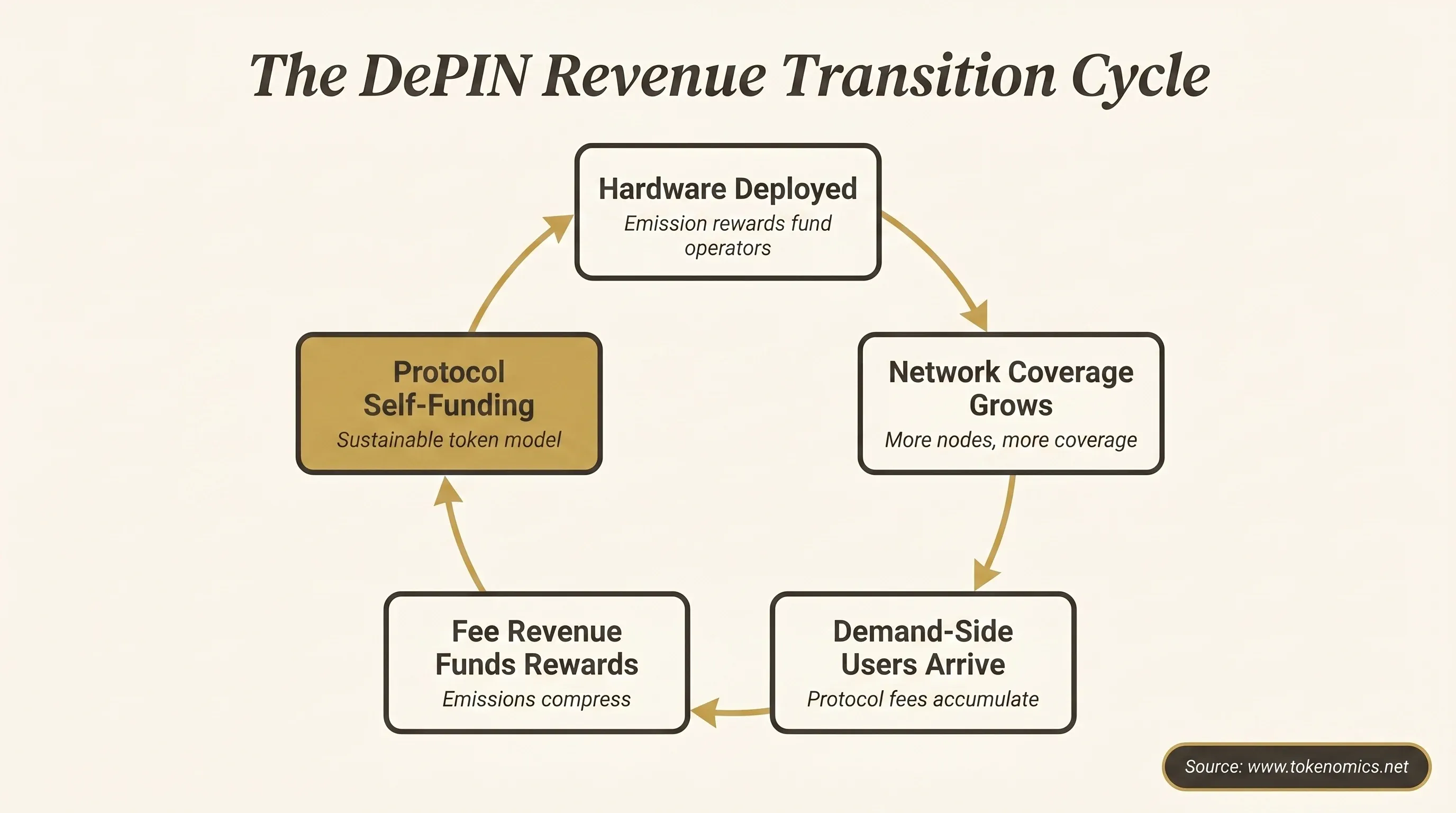

Decision 4: Demand-side revenue transition. How does the protocol define the trigger and pace for shifting from emission-funded rewards to demand-funded rewards? The transition must happen. The question is whether it is designed or improvised.

Decision 5: Governance and staking design. Who has protocol upgrade authority, and how does staking interact with the emission schedule? Governance design determines whether the protocol can adapt the first four decisions as real-world data arrives.

Most DePIN teams treat these as independent choices. They are not. The emission schedule depends on the operator floor. The PoC mechanism design affects which gaming vectors the emission schedule must account for. The demand-transition trigger depends on how quickly real revenue accumulates. Governance design determines whether any of it can be adjusted after launch. Treat them as a system, not a checklist.

For a broader view of DePIN incentive design including how staking layers interact with the reward stack, the published DePIN incentive design framework post covers the three-layer structure in detail.

#Operator Unit Economics: The Foundation of a Sound DePIN Model

Most DePIN teams set the emission schedule based on the tokenomics model they want, then check whether it works for operators afterward. The correct sequence is the reverse.

The floor calculation starts with operator cost. What does it cost to deploy and run a node for 12 months?

- Hardware amortization: the capital cost of the required equipment, amortized over its expected useful life.

- Connectivity: monthly data plan or bandwidth costs where applicable.

- Power: monthly electricity cost for operating the node.

- Maintenance: expected time and parts costs over 12 months.

- Opportunity cost: the return the operator would have earned by deploying that capital elsewhere.

Once you have the floor, the launch-period reward target is the floor plus a risk premium. The risk premium exists because early operators take on novel protocol risk, illiquidity of token rewards at launch, and genuine uncertainty about whether demand-side revenue will develop on schedule. Across the protocols we've worked with, the launch-year reward target typically runs 30-60% above operator floor. That premium compresses toward floor over 24-36 months as the protocol matures and protocol risk decreases.

The emission schedule cannot compress faster than the demand-side revenue ramp. If it does, operators exit. If operators exit, coverage thins. If coverage thins, demand-side users lose the service quality that brought them to the protocol. That cascade compounds against you in every direction.

DePIN tokens are typically structured as utility tokens, but the classification analysis is fact-specific and jurisdiction-specific. Whether a DePIN reward token satisfies the Howey test depends on the specific offering structure, the presence of a common enterprise, and whether purchasers have a reasonable expectation of profit from others' efforts. Get legal classification advice before locking the token design.

Do not set the reward target at "what APY looks competitive in DePIN token marketing." Set it at what the operator math requires. These are different numbers, and the difference is where most DePIN tokenomics fails.

A starting framework for tokenomics consulting engagements in the DePIN vertical always begins with operator unit economics, not with total supply decisions. Supply follows from operator economics, not the other way around. Institutional capital increasingly applies this same operator-economics lens when evaluating DePIN protocol investability: Coinbase research coverage of DePIN protocols consistently cites operator unit economics and demand-transition credibility as the primary investment-thesis variables.

#Designing the Emission Schedule and Supply Architecture

The operator economics floor gives you the reward target. The emission schedule translates that target into a supply architecture.

Four parameters define the emission schedule:

Operator allocation percentage. What share of total token supply is reserved for node operator rewards? This is not a fixed industry norm. It depends on the business model. Protocols where operator activity is the core product (wireless coverage, compute delivery) allocate a larger share to operators. Protocols with significant investor and team capital requirements allocate less. We see operator reward pools ranging from 30% to 65% of total supply across the DePIN sector.

Release rate and time horizon. Over how many years are operator rewards distributed? A longer horizon gives the protocol more time for demand-side revenue to develop before emissions run thin. A shorter horizon concentrates early incentives but accelerates the supply crisis if demand does not materialize.

Emission shape. Three shapes appear consistently in DePIN design.

- Linear decay: Rewards decrease at a fixed rate per epoch. Predictable, easy to model, transparent to operators. The risk: a cliff at the end of the bootstrap window if demand revenue has not ramped.

- Halving: Bitcoin-style punctuated compression. Rewards cut by half at defined intervals. Creates strong early-operator retention (the halving is a known event, so operators plan for it). The risk: mass exit spikes at halving epochs if operators believe post-halving rewards fall below floor.

- Demand-adaptive: Emissions compress algorithmically as demand-side revenue crosses defined thresholds. The most defensible shape for long-term sustainability, but the hardest to implement and communicate. Requires a reliable on-chain revenue oracle.

Reward liquidity design. Are operator rewards immediately liquid, vested linearly, or staked-to-claim? Immediately-liquid rewards produce consistent sell pressure. If that sell pressure depresses the token price faster than demand-side revenue develops, the USD value of rewards falls below operator floor and operators exit. Partial vesting or staked-to-claim mechanics reduce sell pressure but reduce the perceived attractiveness of the program for early bootstrapping. This is a genuine tradeoff, not a free optimization.

The token distribution model framework covers the broader supply architecture decisions, including investor allocations and treasury design, which interact with the operator reward pool.

#Proof-of-Work Mechanisms and Gaming Resistance

The emission schedule defines how much reward is available. The PoC mechanism determines who earns it. A gaming-vulnerable PoC mechanism is not a minor technical detail; it is an existential threat to the token model.

Three PoC mechanisms appear across the DePIN sector.

GPS-attestation: The node proves geographic location through signed GPS coordinates. Used by coverage-based protocols where location is the core verification requirement (Hivemapper, location-based wireless). Gaming vector: GPS spoofing using software tools that broadcast falsified coordinates.

Radio-signal witness: Peer devices attest that a node is transmitting a real radio signal in a claimed location. Used by Helium's LORAWAN and similar wireless protocols. Gaming vector: collusion rings where multiple wallets controlled by one operator attest to each other's coverage.

Service-delivery proof: The node proves it delivered a specific service (a compute job, a data package, an energy generation record) by returning a cryptographically verifiable output. Used by compute DePIN (Render, NOSANA) and energy DePIN (Glow, Arkreen). Gaming vector: returning cached outputs or failing jobs silently without penalty.

Design responses that close these vectors:

- Geographic exclusion zones: No two nodes within a minimum geographic radius earn overlapping coverage rewards. Reduces the incentive to deploy fake nodes adjacent to real ones.

- Witness diversity requirements: A minimum number of distinct witness nodes required per attestation, with those witnesses required to be geographically distributed. Breaks the collusion-ring vector.

- Cryptographic output verification: Verifiable computation proofs, merkle-proof delivery receipts, or signed energy generation certificates. Makes service-delivery fraud detectable on-chain.

The pattern we've seen across 80+ projects: protocols that invest in PoC mechanism design before launch have materially lower gaming rates at 12 months than those that treat anti-gaming as a governance patch. Compliance is the architecture, not a feature. Retrofitting gaming resistance after the protocol is live and the collusion networks are established is far more disruptive than designing for it from the start.

#Vertical-Specific DePIN Tokenomics: Wireless, Compute, Energy, and Mobility

The Five-Variable Framework applies across all DePIN verticals. The specific inputs and tradeoffs differ by vertical. Here is how the framework resolves differently across the four major DePIN categories.

Wireless DePIN. The production case is Helium. Hardware cost: $400 to $2,000 per hotspot. Revenue model: data credits, a flat fee per data packet consumed by device operators. The primary token design tradeoff in wireless DePIN is the multi-token question. Helium's migration to HNT/IOT/MOBILE created governance fragmentation and liquidity fragmentation simultaneously. For new wireless DePIN protocols, we recommend strongly against multi-token architecture before demonstrable product-market fit. The complexity cost is not worth the flexibility until you have real demand data to optimize against.

Compute DePIN. The production cases are Render and NOSANA. Hardware cost: $1,000 to $20,000 or more per GPU node, depending on compute tier. Revenue model: per-job fees, billed in the protocol's native token or converted from fiat demand. The distinctive token design challenge in compute DePIN is that AI-driven demand can scale non-linearly and fast. That is both an opportunity and a risk: if the token model is calibrated for slow demand growth and AI demand arrives quickly, the demand-transition curve shortens in ways the emission schedule was not designed for. Build flexibility into the demand-adaptive mechanism rather than hardcoding thresholds.

Energy DePIN. The production cases are Glow and Arkreen. Hardware cost: $3,000 to $50,000 or more per deployment (solar panels, inverters, smart meters). Revenue model: renewable energy certificate (REC) sales plus grid revenue. The primary token design challenge in energy DePIN is regulatory. Energy trading is a licensed activity in most jurisdictions. The tokenomics design must be scoped to avoid creating an unlicensed energy trading market. The compliance design must front-run jurisdiction-specific energy trading law (Source: CryptoRank DePIN sector analysis, 2024).

Mobility DePIN. The production case is Hivemapper. Hardware cost: dashcam plus connectivity hardware at $400 to $700 per vehicle. Revenue model: map data licensing. The distinctive challenge is geographic coverage gaps. In mobility DePIN, under-mapped areas are the most valuable to license buyers. Tokenomics must actively incentivize coverage in underserved areas through variable reward rates by geographic zone. A flat reward rate produces over-coverage in easy-access urban routes and persistent gaps in rural and developing-region areas where the commercial value of map data is highest.

#Common DePIN Tokenomics Mistakes We See

After advising 80+ projects, the failure patterns in DePIN tokenomics are predictable.

Copying DeFi APY design. Setting operator reward targets at "competitive APY" rather than at operator unit economics. A DeFi liquidity provider thinks in annual percentage yield because their capital has zero deployment friction. A node operator thinks in monthly dollar yield versus monthly operating cost. These are different calculations, and the APY framing systematically produces reward levels that either over-compensate at launch (front-loading the dilution problem) or under-compensate after the first compression event (triggering operator exit).

Front-loading emissions without a demand-side timeline. Concentrating 60-70% of operator rewards in years one and two without a defined demand-ramp model. The protocols that do this attract mercenary hardware capital in year one, see their governance forums fill with operator complaints as rewards compress in year two, and enter year three with declining coverage and no plan for how demand-side revenue closes the gap.

Single-layer PoC that does not close gaming vectors. Launching with GPS attestation as the only PoC mechanism, then discovering widespread spoofing in month three. Retrofitting gaming resistance after launch is a governance crisis. The collusion networks are established, the bad actors have been collecting rewards for months, and any retroactive punishment creates legal and community risk. Design the full gaming-resistance stack before the first node goes live.

Ignoring the operator exit cliff. Emission schedules that compress from 100% to 40% in a single governance vote or a single halving event create mass exit events. Operators plan for known compression schedules. They do not plan for sudden, unannounced compression driven by governance urgency or budget pressure. The compression must be gradual, predictable, and communicated well in advance.

Multi-token complexity before product-market fit. Launching a three-token model (governance token plus reward token plus utility token) before the protocol has demonstrable demand. Multi-token architecture creates liquidity fragmentation, increases UX complexity, and multiplies the number of treasury management decisions required. Build the minimum-complexity token model that solves the core incentive problem. Add complexity only when the problem it solves is real and confirmed by data.

These are not edge cases. They're the five most common ways DePIN protocols create structural tokenomics failure before they reach self-funding.

For a broader view of tokenomics mistakes that apply across crypto project types, including the over-distribution and governance design failures that overlap with DePIN, the tokenomics mistakes post covers seven structural errors in detail.

#Building DePIN Tokenomics That Hold Up Under Scrutiny

DePIN is a young sector. Most of the design failures are still being discovered in real time. The protocols that build from operator economics first, design a credible demand-transition model, and invest in PoC mechanism integrity are the ones that reach self-funding. The others are countdowns.

The token is the bootstrap mechanism. The business is a real-world infrastructure network that generates real service revenue. If the token is the product, the protocol does not survive emission compression. Revenue-first design applies in DePIN as much as it applies anywhere else in the token economy.

If you're building a DePIN protocol and need your tokenomics to hold up under institutional and regulatory scrutiny, book a discovery call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.

FAQ: DePIN Tokenomics

What is DePIN tokenomics? DePIN tokenomics is the mechanism design discipline for token incentive systems that coordinate decentralized physical infrastructure networks. It covers the five core design decisions: operator unit economics, emission scheduling, proof-of-work mechanism, demand-side revenue transition, and governance design.

How is DePIN tokenomics different from DeFi tokenomics? DeFi liquidity providers allocate capital with zero physical friction. DePIN node operators invest in physical hardware with real setup costs, operating costs, and exit barriers. DePIN tokenomics must account for hardware depreciation, geographic coverage requirements, and service delivery proof before reward. Standard DeFi liquidity-mining models applied to DePIN produce predictable operator exit failures.

What is the operator unit economics floor in DePIN? The operator unit economics floor is the minimum token reward, expressed in USD equivalent, required to make node deployment economically rational. It equals the total 12-month operator cost: hardware amortization, connectivity, power, maintenance, and opportunity cost of the deployed capital. The launch-year reward target should exceed this floor by 30-60% to compensate for novel protocol risk and launch-period token illiquidity.

What is the demand-side revenue transition in DePIN? The demand-side revenue transition is the protocol's designed shift from emission-funded operator rewards to demand-funded operator rewards. As demand-side revenue (protocol fees, data credit purchases, compute fees) accumulates, emissions compress. A well-designed transition is gradual, predictable, and triggered by defined on-chain revenue thresholds, not by governance vote under pressure.

What are the main DePIN verticals and how do their token designs differ? The four main DePIN verticals are wireless, compute, energy, and mobility. Wireless DePIN faces the multi-token complexity trap (Helium's HNT/IOT/MOBILE being the cautionary example). Compute DePIN must handle non-linear demand growth from AI. Energy DePIN must front-run jurisdiction-specific energy trading regulation. Mobility DePIN must solve geographic coverage gaps through variable reward rates by zone.

What is the most common DePIN tokenomics mistake? Copying DeFi APY design. Node operators do not think in APY; they think in monthly dollar yield versus monthly operating cost. Setting reward targets using APY framing systematically produces either over-compensation at launch (creating front-loaded dilution) or under-compensation at first compression (triggering operator exit). Start with the operator floor calculation, not with a target APY.