Stablecoin Design: Three Mechanisms and What Makes a Stablecoin Work at Scale

Stablecoin design determines how a stablecoin maintains its peg, sources collateral, and manages supply. This post covers the three mechanism types and what institutional investors require.

Stablecoin design: The mechanism engineering discipline that determines how a stablecoin maintains its price peg, sources and manages collateral, and responds to supply-demand imbalances, encompassing collateral architecture, redemption mechanics, liquidation structures, and revenue sustainability.

Stablecoin design is the mechanism engineering discipline that determines how a stablecoin maintains its peg, sources its collateral, and manages supply in response to demand. Getting this decision wrong does not produce a suboptimal token. It produces one of the most expensive failures in crypto. The 2022 Terra/LUNA collapse wiped $40 billion in market cap in 72 hours. The mechanism was not poorly implemented. It was structurally incorrect for the conditions it faced.

Most stablecoin failures we see across 80+ engagements share a single root cause: the mechanism was designed for stability at launch, not for stability under market stress. Stablecoin tokenomics starts with stress testing the peg, not with optimizing the yield.

#The Three Stablecoin Mechanisms

Stablecoin design choices collapse into three mechanism categories. Each carries a distinct collateral risk, regulatory posture, and institutional investor documentation requirement. Choosing the wrong mechanism for your use case is not recoverable after launch.

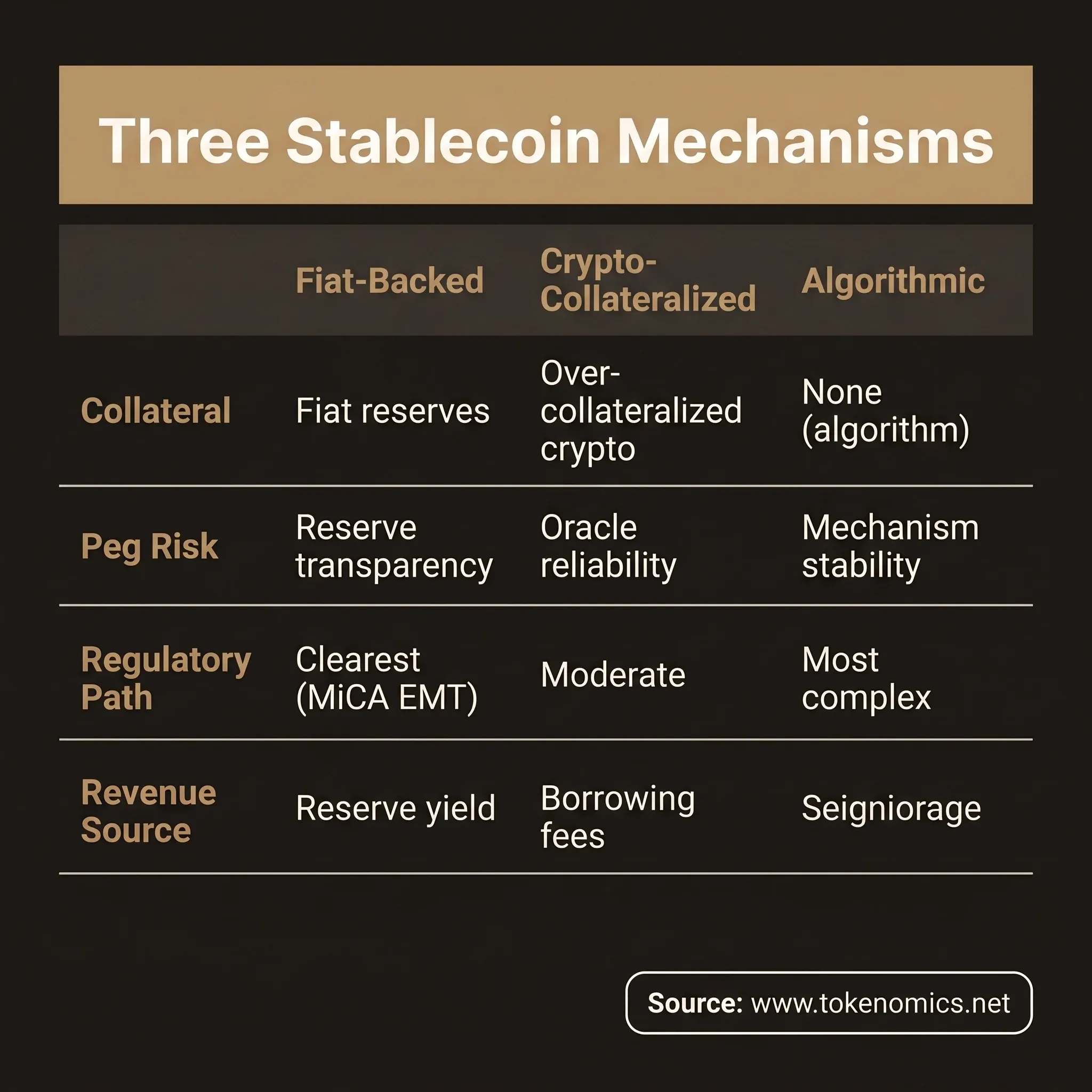

Fiat-backed stablecoins (Type 1). The mechanism is simple: for every stablecoin in circulation, an equivalent fiat currency amount sits in a reserve account. USDC and USDT are the canonical examples. The peg holds because redemption is straightforward, a holder submits stablecoins and receives fiat. The primary risk is custodial and reputational: if the reserve does not match the claims, confidence collapses immediately. The reserve transparency standard is rising. Monthly attestation is no longer sufficient for institutional integration. Real-time reserve proof mechanisms are the emerging minimum.

Crypto-collateralized stablecoins (Type 2). The mechanism uses over-collateralization to absorb collateral volatility. DAI and LUSD are the primary examples. A borrower locks 150% or more of a stablecoin's value in crypto collateral (typically ETH or a basket), mints the stablecoin against that position, and the protocol liquidates the position if the collateral ratio falls below the liquidation threshold. The peg holds because the mechanism can always redeem stablecoins for at least $1 of collateral value at the liquidation threshold. Oracle reliability is the primary risk variable: a price feed manipulation attack can trigger mass liquidations at incorrect prices.

Algorithmic stablecoins (Type 3). The mechanism maintains the peg without direct collateral. Instead, it uses seigniorage (expanding and contracting the token supply algorithmically) or rebase mechanics. This category has the highest failure rate. The 2022 Terra/LUNA collapse wiped $40 billion in market cap in 72 hours because the algorithmic peg mechanism was self-referential: stablecoin redemptions required minting the governance token (LUNA), which created a death spiral under sell pressure (Source: CryptoRank token market data). Projects proposing algorithmic stablecoin mechanisms today face investor and regulatory skepticism that is substantially higher than before the Terra event.

Collateral ratio: The ratio of the value of collateral locked in a position to the value of stablecoins minted against it. A 150% collateral ratio means $150 in collateral backs $100 in stablecoins. The liquidation threshold is the minimum ratio before the protocol forces a liquidation.

Seigniorage: In algorithmic stablecoin design, the profit (seigniorage) generated when new stablecoins are minted at a price above $1, the mechanism distributes this profit to governance token holders or burns the governance token to maintain the peg. It is the primary value accrual mechanism in non-collateralized stablecoin designs.

#Stablecoin Mechanism Design: What to Optimize For

Most teams designing a stablecoin optimize for yield. That is the wrong optimization target. The primary optimization target is peg stability under stress.

Three stress scenarios define good stablecoin mechanism design:

Normal demand. The mechanism works for every stablecoin type at normal demand. This is the scenario most teams design for. It tells you almost nothing about mechanism quality.

Sudden redemption pressure. What happens when 30% of circulating supply seeks redemption in 24 hours? Fiat-backed stablecoins handle this through reserve liquidity, are the reserves in liquid instruments that can be converted in hours? Crypto-collateralized stablecoins handle this through liquidation mechanics, are there enough liquid positions to absorb the redemption demand without cascading liquidation failures? Algorithmic stablecoins typically fail this scenario when the governance token has correlated sell pressure.

Correlated market crash. This is the stress test most mechanisms fail. When ETH drops 40% in 6 hours, a crypto-collateralized stablecoin with 150% collateral ratios has a 25% margin before mass liquidation. That margin shrinks quickly when every liquidation adds to the downward price pressure on the collateral asset.

The stablecoin mechanism design must specify circuit breakers: a pause mechanism for unusual redemption volumes, a redemption queue for high-stress scenarios, and an emergency governance path that is faster than a standard DAO vote (which can take 48-72 hours, too slow for a 4-hour market crisis).

Revenue routing inside a stablecoin matters for sustainability. Revenue-First Design applies directly: a stablecoin without a documented revenue model is a countdown timer for treasury drawdown. The primary revenue sources are collateral yield (for fiat-backed stablecoins holding US Treasuries), borrowing fees (for crypto-collateralized stablecoins), and liquidation penalties. The revenue model must cover protocol operating costs at the minimum expected TVL.

#Compliance and Classification: The Regulatory Surface

Stablecoin design choices determine regulatory exposure as much as peg mechanism. The classification analysis differs by mechanism type.

Fiat-backed stablecoins have the clearest regulatory path. The EU's MiCA (Markets in Crypto-Assets) regulation created a direct category for e-money tokens (EMTs), fiat-backed stablecoins that redeem 1:1 for fiat. MiCA's requirements include authorization, capital requirements, reserve management rules, and redemption rights. US legislative frameworks are converging on a similar payment token category. Projects launching fiat-backed stablecoins today can reasonably design for MiCA compliance and treat US legislation as a predictable path.

Algorithmic stablecoins face a harder regulatory surface. The Howey test applies when the stablecoin mechanism involves purchasing a governance token that supports peg stability, the SEC has signaled that algorithmic mechanisms where token holders profit from protocol growth may constitute an investment contract. Stablecoin compliance analysis for algorithmic mechanisms requires a jurisdiction-specific legal opinion before launch.

The FIT-21 digital asset legislation creates a payment token category for stablecoins backed by dollar-denominated assets. For projects designing stablecoins today, FIT-21's payment token provisions are the most relevant US legislative signal. The key risk for any stablecoin design is whether the mechanism creates a profit expectation from the efforts of others, that is the threshold where payment token treatment ends and securities treatment begins.

Token classification for stablecoins is fact-specific and jurisdiction-specific. A legal opinion is required before launch for any mechanism that is not straightforwardly fiat-backed with no governance token profit mechanics.

#What Institutional Investors Require

Institutional investors approaching stablecoin due diligence have specific documentation requirements by mechanism type. Projects that do not have this documentation ready face a longer diligence process, or a decline.

For fiat-backed stablecoins, the standard is moving toward real-time reserve attestation. The Franklin Templeton BENJI tokenized money market fund set the institutional standard for reserve transparency in on-chain products. Monthly third-party attestations are now the floor; projects seeking institutional integration should target at least weekly, with real-time proof mechanisms as the emerging standard.

For crypto-collateralized stablecoins, investors require documented collateral quality analysis: oracle source documentation, historical drawdown data for each collateral asset, liquidation threshold rationale, and a stress test showing the mechanism's behavior at 30%, 50%, and 80% collateral drawdown scenarios.

The investor question that stablecoin designs must answer is this: "What happens to my redemption if the collateral loses 30% of its value in 24 hours?" Projects that cannot answer this question with a documented analysis cannot move through institutional due diligence.

#Common Stablecoin Design Mistakes

After reviewing stablecoin designs across dozens of engagements, the failure patterns are predictable.

Designing for normal conditions. Every mechanism works at 1:1 demand. The mechanism quality shows at 3:1 redemption pressure or at correlated collateral stress. Teams that have only modeled normal conditions have not modeled the mechanism.

Under-collateralizing to compete on yield. Every basis point of yield improvement financed by lower collateral ratios is a risk transfer from the protocol to the reserve. Over-collateralization is not conservative tokenomics. It is the mechanism's stability margin.

Relying on governance for emergency intervention. A DAO vote takes 48-72 hours. A correlated market crash takes 4 hours. Emergency governance paths must be pre-approved, with defined trigger conditions, execution thresholds, and automatic circuit breakers.

Launching without a classification analysis. Projects that launch without a stablecoin design legal opinion discover the classification question in an enforcement context. That is the most expensive version of the analysis.

Copying the last generation's mechanism without understanding the failure mode. The Terra/LUNA post-mortem is required reading for any team designing an algorithmic stablecoin. Not understanding why the mechanism failed does not prevent the next mechanism from failing the same way.

#Frequently Asked Questions

What is the difference between a fiat-backed and an algorithmic stablecoin? A fiat-backed stablecoin holds a 1:1 reserve in fiat currency or equivalent liquid assets and redeems stablecoins for fiat at par. An algorithmic stablecoin maintains its peg without direct collateral, using token supply expansion and contraction mechanics instead. Fiat-backed stablecoins carry custodial and reserve transparency risk. Algorithmic stablecoins carry mechanism risk, when demand to redeem exceeds the mechanism's ability to maintain the peg, the peg can collapse rapidly, as the Terra/LUNA event demonstrated.

How does a crypto-collateralized stablecoin maintain its peg? A crypto-collateralized stablecoin requires borrowers to lock significantly more collateral value than the stablecoins they mint, typically 150% or more. If the collateral's market value drops below the liquidation threshold, the protocol automatically liquidates the position and uses the proceeds to retire the stablecoins. The peg holds as long as the collateral can be liquidated for at least $1 per stablecoin. Oracle reliability is the critical dependency: price feed manipulation can trigger incorrect liquidations.

What does MiCA require for stablecoin issuers? MiCA (Markets in Crypto-Assets) establishes two categories for stablecoins in the EU: asset-referenced tokens (ARTs) and e-money tokens (EMTs). Fiat-backed stablecoins that redeem 1:1 for a single fiat currency qualify as EMTs and require regulatory authorization, capital requirements, reserve segregation, and real-time redemption rights. ARTs, stablecoins backed by a basket of assets, carry stricter capital requirements. MiCA is in force; EU-based stablecoin issuers without authorization are operating unlawfully.

Can an algorithmic stablecoin be classified as a security? Yes, depending on the mechanism. The Howey test, the US framework for investment contract analysis, applies when buyers of a complementary governance token expect profits from the efforts of the stablecoin protocol team. If an algorithmic stablecoin's peg mechanism depends on governance token demand, and governance token holders profit from protocol growth, the SEC may treat the system as an investment contract. This is a fact-specific analysis; a legal opinion before launch is required.

What revenue does a stablecoin protocol actually generate? The primary revenue sources depend on mechanism type. Fiat-backed stablecoins earn yield on reserve assets, typically US Treasuries or money market instruments. Crypto-collateralized stablecoins earn borrowing fees (the interest rate charged for minting stablecoins against collateral) and liquidation penalties. The sustainability test: does the protocol cover operating costs at the minimum expected TVL without relying on treasury drawdown or token price appreciation?

What is the minimum reserve transparency standard for institutional integration? Monthly third-party attestations are now the minimum. Projects seeking integration with institutional custody providers, regulated funds, or on-chain treasury management protocols are expected to provide at least weekly attestations with auditor-verified reserve composition. Real-time proof of reserves using on-chain verification is the emerging standard for institutional-grade stablecoin integration.

What documentation do investors require before funding a stablecoin project? Investors require mechanism documentation (stress test models covering normal demand, redemption pressure, and correlated market crash scenarios), reserve management documentation (for fiat-backed: reserve composition, custodian, attestation frequency; for crypto-collateralized: oracle source, collateral basket composition, historical drawdown data), a token classification legal opinion, and a revenue sustainability model. Projects that cannot produce this documentation face a longer diligence process or a decline.

The stablecoin category is maturing faster than most project teams realize. MiCA is live in the EU. US payment token legislation is advancing. Projects that design for regulatory clarity now are building for the next 5 years. Projects that copy the last generation's mechanism without understanding its regulatory surface are taking on undisclosed liability.

If you're building onchain and need your stablecoin design to hold up under institutional scrutiny, book a strategy call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.