Real World Asset Tokenomics: Designs Built for Institutional Scrutiny

Real world asset tokenomics is the design of token models for physical and financial assets. Learn the revenue models, supply mechanics, and compliance architecture that separate institutional-grade RWA designs from failed ones.

Real world asset tokenomics: The design of token models that represent physical or financial assets on-chain, where the token's supply mechanics, yield distribution, compliance architecture, and governance model are derived from the underlying asset's revenue structure rather than from a native crypto incentive design.

Real world asset tokenomics is the design of token models that represent real-world assets: real estate, private credit, tokenized treasuries, commodities, and revenue-generating businesses. Unlike DeFi tokenomics driven by emissions and speculation, RWA tokens derive value from real cash flows. The tokenomics design must reflect the asset's actual revenue mechanics, and that constraint changes almost every design decision from supply to governance.

Most DeFi tokenomics starts with a token and works backward to find utility. RWA tokenomics starts with a real asset and works forward to find the right tokenization structure. This reversal changes everything about the design process.

The institutional capital entering onchain markets, the Franklin Templeton BENJI tokenized money market fund, the BlackRock BUIDL tokenized fund, the Centrifuge-and-Maple ecosystem, arrived with this discipline already in place. These projects designed the legal structure, the revenue model, and the compliance architecture before they chose a token standard. Projects that work backward from a token model to a real asset tend to fail at the institutional due diligence stage. The RWA market has grown to over $19 billion in tokenized assets on-chain as of 2025 (Source: the RWA.xyz on-chain RWA tracker), and every institutional participant at that scale operates on this discipline.

#Why RWA Tokenomics Starts With the Asset, Not the Token

Most tokenomics frameworks assume you're designing from scratch, creating new incentive structures for digital-native protocols. Real-world asset tokenization is the opposite.

The asset exists. It has a legal structure. It generates revenue or holds value in ways governed by existing contracts, regulations, and counterparties. The token is a representation of that structure, not a replacement for it. This means the token's mechanics must be derivable from the asset's mechanics, and any token design that cannot be traced back to the underlying asset's legal and financial structure will fail at the compliance review.

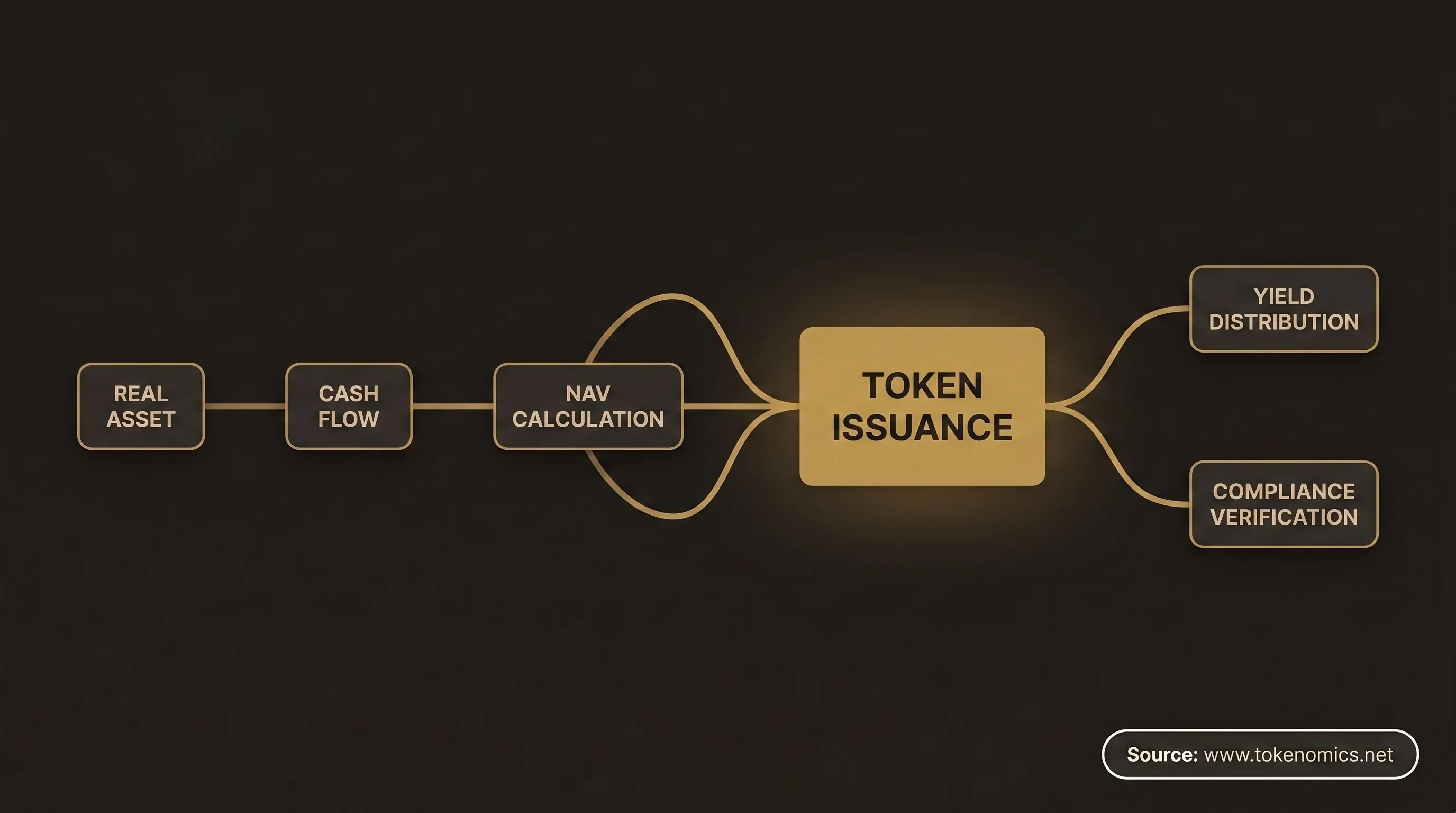

We use what we call the RWA Value Chain Framework to structure this derivation. The framework has six nodes: the real asset itself, the cash flow the asset generates, the NAV (net asset value) calculation methodology, the token issuance mechanism, the yield distribution mechanics, and the compliance verification layer. Each node must be explicitly designed before the token can be issued. Projects that jump from "we have an asset" to "we're launching a token" are skipping four of the six nodes.

The most common skipped node is NAV calculation. For tokenized real estate, NAV is the appraised value of the underlying property adjusted for outstanding obligations. For tokenized credit funds, NAV is the marked-to-market or marked-to-model value of the credit portfolio. For tokenized commodities, NAV is the spot price of the commodity times the quantity held in custody. Each asset class has a different NAV methodology, and the token's supply mechanics must reflect that methodology directly. A token that mints freely without reference to the underlying NAV is not a real world asset token; it's a synthetic with a real-asset story attached.

#The Three Revenue Models in RWA Tokenomics

RWA tokenomics concentrates into three revenue models. Each has different tokenomics implications, different compliance postures, and different market-making requirements.

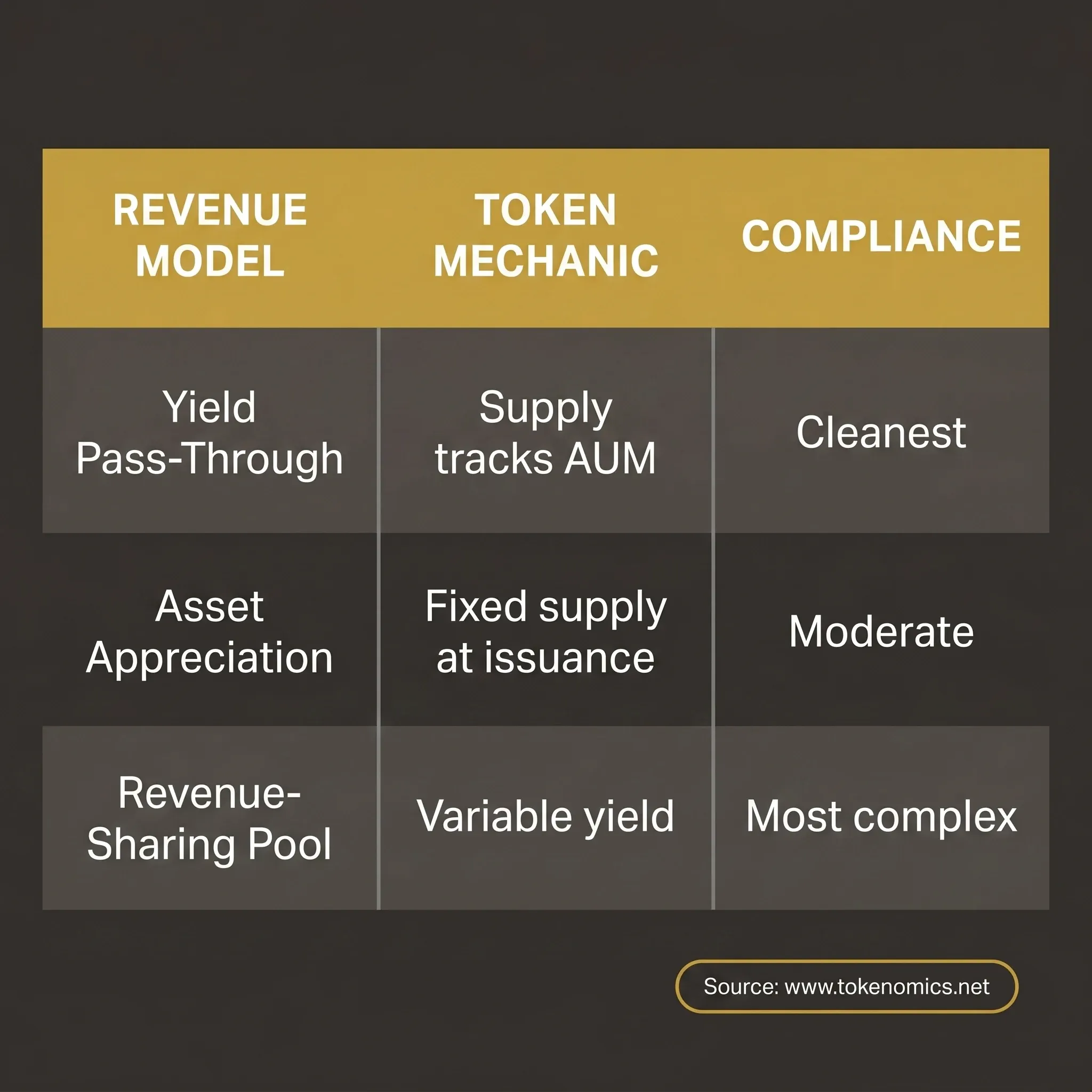

Yield pass-through. The most institutionally mature model. The token represents a claim on an asset that generates a deterministic yield: a treasury bill, a money market instrument, a fixed-rate loan. The token's value tracks the underlying asset's NAV; yield accrues to holders in proportion to their balance. The Franklin Templeton BENJI tokenized money market fund and the BlackRock BUIDL tokenized fund operate on this model. The tokenomics design is relatively constrained: fixed or slowly-growing supply, no emissions incentives, yield distribution tied directly to the underlying instrument's coupon or money market rate. Compliance posture is also cleanest in this model, the token is representing a known regulated instrument, and the KYC/AML and accreditation requirements track those of the underlying fund.

Asset appreciation tokenization. The token represents an equity-like claim on an asset whose value appreciates over time: real estate, private equity, or a revenue-generating business. Yield may or may not be distributed to holders; the primary value proposition is capital appreciation on the underlying asset. This model is significantly more complex from a tokenomics standpoint. The token's supply must reflect the total capitalization of the asset. Governance mechanics become critical: who decides when to sell the asset, when to distribute proceeds, and how to manage capital improvements? The classification question is also harder in this model, the closer the token sits to an equity or profit-distribution mechanism, the more the design surfaces the Howey test's "expectation of profits from others' efforts" prong.

Revenue-sharing pools. The token represents a claim on a share of an operational business's revenue. DePIN protocols sit in this category, as do tokenized media platforms and infrastructure projects. This is the most complex revenue model from a tokenomics perspective. Revenue is variable, the asset does not have a clear liquidation value, and the distribution mechanics must handle uneven revenue streams without creating the yield instability that institutional token holders find unacceptable. The compliance question here is the hardest: revenue-sharing pools look most like unregistered securities to regulators, and the design must be structured carefully against the applicable regulatory framework from day one.

#Supply Design for RWA Tokens

Supply design for RWA tokens follows from the revenue model. This is the dimension where most RWA projects make their first and most costly mistake.

Fixed supply tracks NAV. For yield pass-through tokens, supply should track the total capital committed to the underlying instrument. New tokens are minted when new capital enters the fund; tokens are burned when holders redeem. The supply at any moment equals the total assets under management, divided by the token price. This is the cleanest supply design for institutional investors, who can model their exposure directly.

Variable supply requires explicit NAV oracle. For asset appreciation models, the supply is often fixed at issuance (representing 100% of the asset's equity). The token price floats based on the underlying asset's NAV. For this to function, the protocol needs a verified, audited NAV calculation published on a defined cadence, quarterly for real estate, monthly for private credit, daily for liquid instruments. Without this oracle, the token's market price disconnects from the underlying value, and the "real world asset" story collapses into speculation.

Redemption mechanics are non-negotiable. Every RWA token must have a clear, documented, and legally-enforceable redemption path. Investors must know exactly how they exit: through secondary market trading, through protocol-level redemption at NAV, through a defined liquidity window, or through some combination. Projects that launch RWA tokens without a redemption mechanism are issuing illiquid receipts, not tokenized assets. The distinction matters to institutional investors, to exchanges evaluating a listing, and to regulators evaluating whether the token constitutes an unregistered security.

#Compliance Architecture Is the Foundation, Not a Feature

Compliance is the architecture, not a feature.

For RWA tokens, this isn't a philosophical statement, it's a technical constraint. The token standard you choose determines which compliance mechanisms are technically available to you. ERC-20 tokens are permissionless by default; anyone can hold and transfer them. That is incompatible with the accreditation requirements, transfer restrictions, and identity verification requirements that apply to most regulated RWA instruments.

ERC-3643 is the standard purpose-built for this problem. It embeds identity verification and transfer compliance directly into the token contract via an on-chain identity registry. Transfers are permitted only between verified participants. Accreditation status, jurisdiction restrictions, and KYC/AML clearances are enforced at the smart contract layer, not via off-chain gates that can be bypassed. Centrifuge on-chain credit markets and other institutional RWA protocols have moved to ERC-3643 or equivalent standards for this reason.

For EU-facing RWA projects, MiCA (Markets in Crypto-Assets) introduces registration and reserve requirements that vary by asset class and token structure. For U.S.-facing projects, the FIT-21 digital asset legislation introduces a framework that distinguishes digital commodities from digital securities on factors including decentralization and issuer involvement. The RWA tokenomics design must be evaluated against both frameworks before launch, not after. Compliance is the architecture, not a feature.

#Distribution and Governance in RWA Tokens

Yield distribution mechanics deserve their own design sprint. The question is not just how to distribute yield, but when, in what denomination, and with what gas-cost structure.

On-chain yield distribution in the native token raises the fewest compliance questions but creates gas-cost overhead at scale. Stablecoin distributions (USDC, USDT) are more practical for institutional holders who need a defined-value denomination for accounting purposes. Some protocols distribute yield off-chain entirely, with the token serving as a record-of-right rather than a settlement instrument. Each approach has different smart contract requirements, different accounting treatment for holders, and different compliance posture.

Governance mechanics for RWA tokens are where projects consistently over-engineer. The instinct is to create a governance token that controls asset management decisions: when to buy, when to sell, when to re-invest yield. In practice, institutional asset managers operating under fiduciary duties cannot delegate these decisions to a token governance vote. Governance in an RWA context is narrower than DeFi governance: it covers protocol parameters (fee splits, service provider selection, redemption queue management), not asset management decisions. Projects that conflate protocol governance with asset management authority will find institutional capital managers declining to participate.

#Common Mistakes We See in RWA Tokenomics

After designing tokenomics across 80+ projects, including multiple RWA engagements, the failure patterns in this category are consistent.

Designing the token before the revenue model. The first design question in RWA tokenomics is not "what should the token do?" It is "how does the underlying asset generate revenue, and what legal structure governs that revenue?" Projects that design the token first build backward into the asset and consistently discover mid-engagement that the token mechanics they chose are incompatible with the asset's legal structure.

Treating compliance as a post-design step. We see this in almost every RWA project that comes to us having started elsewhere. The token standard was chosen for technical reasons (gas cost, ecosystem tooling), without evaluating whether that standard supports the compliance requirements the asset class actually needs. Retrofitting compliance onto a token standard that wasn't designed for it is expensive and, in some cases, impossible without redeployment.

Infinite minting without redemption mechanics. RWA tokens with no ceiling on minting and no redemption path are not real world asset tokens in any institutional sense. The supply mechanics must be directly tied to the underlying asset's capital structure. Every minted token should correspond to a unit of the underlying asset; every burned token should correspond to a redemption at NAV.

Conflating token governance with asset management authority. The governance design should cover protocol parameters, not the asset manager's fiduciary decisions. Institutional capital managers will not participate in a structure where their investment is subject to governance votes they cannot control.

Copying DeFi emissions models onto real assets. A tokenized treasury bond that also has a liquidity mining program to incentivize liquidity provision is mixing incompatible value propositions. The treasury bond's value comes from the underlying instrument's yield. Emissions-driven liquidity incentives introduce inflationary supply pressure that distorts the token's price relative to its NAV. These two mechanics are not additive in the RWA context; they are contradictory.

#Frequently Asked Questions

What is real world asset tokenomics? Real world asset tokenomics is the design of token models for protocols that represent physical or financial assets on-chain. It covers the revenue model (how the underlying asset generates cash flows), supply mechanics (how token supply tracks the underlying asset's NAV or equity), compliance architecture (which token standards and verification mechanisms apply), yield distribution (how revenue passes through to token holders), and governance design (what protocol decisions are appropriate for token governance vs. professional asset management).

How is RWA tokenomics different from DeFi tokenomics? DeFi tokenomics typically starts with a token model and designs incentives to create demand. RWA tokenomics must start with the underlying asset's revenue structure and work forward to the token mechanics. The compliance constraints are also fundamentally different: DeFi tokens can be permissionless; most RWA tokens require identity verification, accreditation checks, and transfer restrictions at the smart contract layer to satisfy the regulatory requirements applicable to the underlying asset.

What token standard is best for RWA tokenization? ERC-3643 is the standard purpose-built for regulated assets. It embeds identity verification and transfer compliance directly into the token contract. For projects that need partition management (representing different classes or tranches of the same underlying asset), ERC-1400 provides the partition architecture. ERC-20 is generally not appropriate for tokenized assets with regulatory compliance requirements, because permissionless transfers cannot satisfy KYC/AML and accreditation-verification obligations.

What are the three revenue models in RWA tokenomics? The three models are: (1) yield pass-through, where the token represents a claim on a yield-generating instrument and distributions track the underlying instrument's coupon or return; (2) asset appreciation tokenization, where the token represents an equity-like claim on an appreciating asset with no mandatory yield distribution; and (3) revenue-sharing pools, where the token represents a claim on a share of an operational business's revenue stream. Each model has different supply mechanics, compliance posture, and governance requirements.

Do RWA tokens require a redemption mechanism? Yes. Every institutional-grade RWA token design requires a clear, documented, and legally-enforceable redemption path. Without a redemption mechanism, the token is an illiquid receipt rather than a tokenized asset. Exchange listing teams and institutional investors require redemption mechanics as a precondition for participation. The specific form, secondary market liquidity, protocol-level NAV redemption, defined liquidity windows, depends on the asset class and the issuer's legal structure.

What compliance frameworks apply to RWA tokenomics? The applicable frameworks depend on the asset class and the jurisdictions the issuer operates in. U.S.-focused projects must evaluate the Howey test analysis, Regulation D (for accredited investor exemptions), and the emerging FIT-21 framework. EU-facing projects must evaluate MiCA registration requirements. Projects with international distribution face the full matrix. Compliance architecture, the specific token standard and on-chain verification mechanisms, must be selected to satisfy these requirements from day one, not retrofitted after launch.

How does the RWA market validate a token's NAV? NAV validation methodologies vary by asset class. Tokenized treasury funds typically use daily NAV calculations published by the fund administrator, mirroring the methodology used for traditional money market funds. Tokenized real estate uses quarterly independent appraisals from registered appraisers. Tokenized credit funds use marked-to-model or marked-to-market methodologies published on a monthly cadence. The critical design requirement is that the NAV calculation is published on a defined, auditable schedule and that the token's supply mechanics reference it directly.

#The Bar Is Institutional Now

The RWA market is not waiting for retail adoption to validate the model. The institutional capital is already there. Franklin Templeton, BlackRock, Ondo, and the emerging credit infrastructure projects are operating with the full compliance and mechanism design discipline that institutional asset management requires.

Projects that design RWA tokenomics the way they'd design a DeFi farming protocol will not meet that bar. The revenue model must be explicit. The supply mechanics must track NAV. The compliance architecture must be embedded at the token standard level. The redemption path must be documented and enforceable. None of this is optional if the goal is institutional participation.

If you're building onchain in the RWA category and need your token mechanics to hold up under institutional scrutiny, book a strategy call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.