MiCA Compliance for Token Issuers: What Your Token Design Determines

MiCA compliance for token issuers: how token design choices determine classification, authorization requirements, and timing in the EU enforcement window.

MiCA compliance is the process of aligning a crypto-asset's design, documentation, and distribution with the Markets in Crypto-Assets (MiCA) Regulation (EU) 2023/1114, the EU's binding legal framework governing token issuance and crypto-asset service providers. The classification your token receives under MiCA determines whether you face a full authorization regime, a notification-only path, or no MiCA obligation at all. That classification is not decided at launch. It is decided at design.

This post covers what MiCA regulates, how the three token categories differ in what they require, and which specific design choices determine your classification before a single line of code is written. If you have EU investors, EU users, or plans to list on an EU-licensed exchange, this framework applies to you now.

The MiCA enforcement 2024 timeline is not a future concern. For ARTs and EMTs, MiCA entered full force on June 30, 2024. For most crypto-asset service providers, the December 30, 2024 deadline has passed. Transition periods for projects that were already operating before those dates are expiring through mid-2026. The projects that treat MiCA compliance as a future concern are working backward from a regulatory position they've already missed.

MiCA compliance refers to adherence to the Markets in Crypto-Assets Regulation (EU) 2023/1114, the EU's binding legal framework for crypto-asset issuers and service providers. Under MiCA, tokens are classified as Asset-Referenced Tokens (ARTs), E-Money Tokens (EMTs), or other crypto-assets (utility and governance tokens). Classification determines whether an issuer faces full EU authorization, NCCA notification, or a self-certification pathway. MiCA entered full force on June 30, 2024 for ARTs and EMTs.

Quick Summary

- What MiCA regulates: ARTs (multi-asset referenced), EMTs (single-fiat referenced), and other crypto-assets (utility, governance, access tokens). Does NOT cover fully decentralized DeFi without an identifiable issuer, genuinely unique NFTs, or MiFID II-regulated securities.

- Key classification variables: Redemption mechanism design, revenue distribution to holders, staking yield denomination, geographic distribution structure.

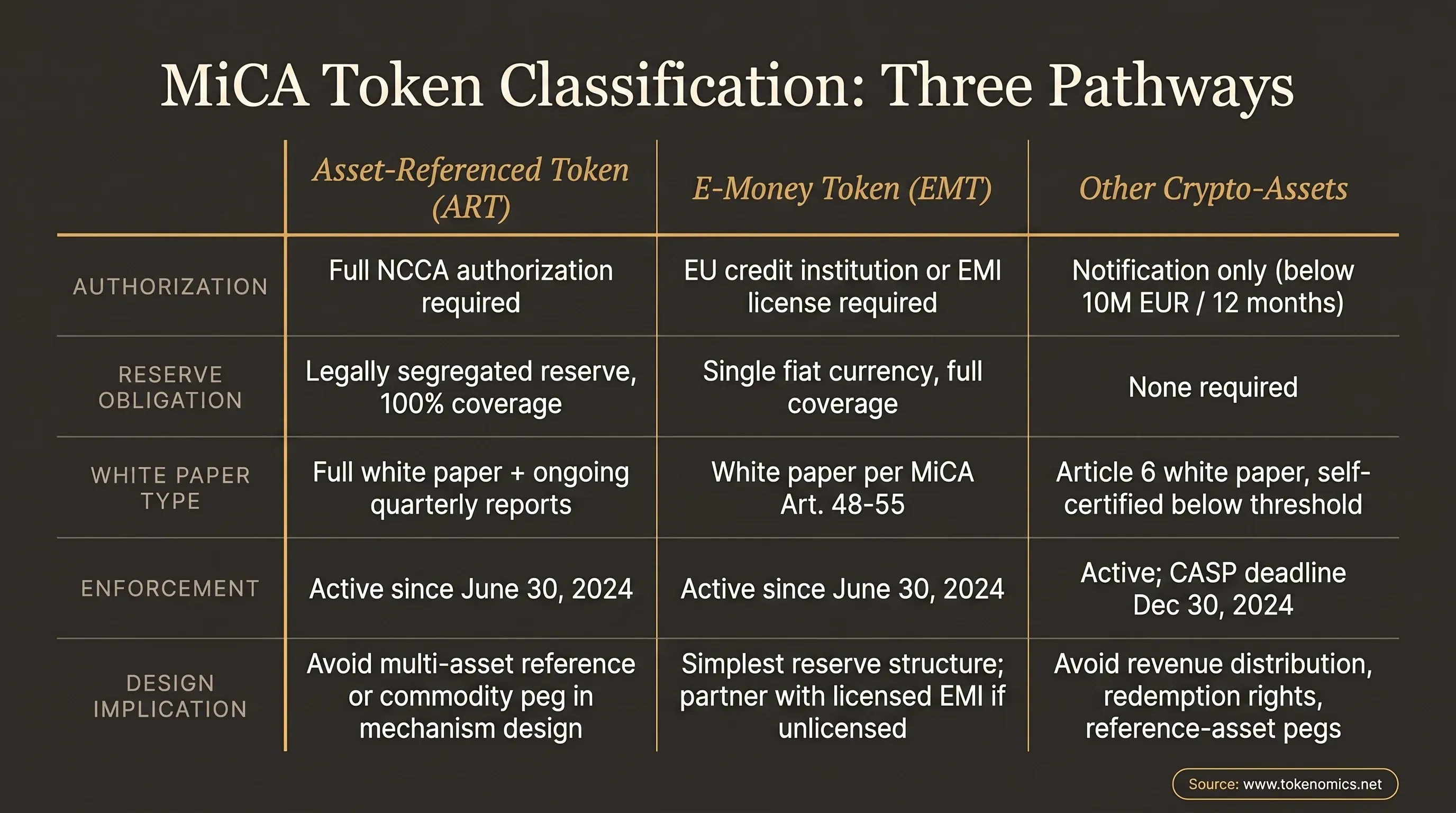

- Authorization requirement: ARTs require full NCCA authorization; EMTs require credit institution or EMI licensing; other crypto-assets require white paper notification only (below 10M EUR / 12 months).

- Enforcement status: Full enforcement active since June 30, 2024 for ARTs/EMTs. Transition periods expiring mid-2026.

- Action required now: Classify your token, assess EU nexus, prepare MiCA white paper per Articles 4-14, begin NCCA notification if ART/EMT path.

#What MiCA Actually Regulates (and What It Misses)

MiCA (Markets in Crypto-Assets) is a regulation, not a directive. That means it applies directly across all 27 EU member states without requiring transposition into national law. If you are offering a crypto-asset to EU investors, seeking admission to trading on an EU-regulated venue, or providing crypto-asset services in the EU, MiCA compliance scope covers you regardless of where your entity is incorporated (Source: MiCA Regulation (EU) 2023/1114, Article 2, Official Journal of the European Union).

MiCA covers three broad asset categories: Asset-Referenced Tokens (ARTs), E-Money Tokens (EMTs), and all other crypto-assets that don't fit the first two categories. Most governance tokens, access tokens, and utility tokens without currency reference fall into the third bucket. Understanding which category your token belongs to is the first step in any Markets in Crypto-Assets compliance analysis.

What MiCA does not cover is equally important to understand:

DeFi protocols operating in a fully decentralized manner are excluded from MiCA's scope. "Fully decentralized" has no safe-harbor definition yet, which means projects claiming this exclusion are making a factual assertion that regulators can and do challenge.

NFTs that are genuinely unique and non-fungible are excluded. Fractional NFTs, NFT series, and NFTs with embedded financial rights are not. The line is fact-specific and the EU Commission is watching closely.

Financial instruments already regulated under MiFID II (including most security tokens) are excluded from MiCA because they're already covered by existing securities law. MiCA is the framework for the crypto-assets that previously fell outside existing regulation.

The practical implication: before you ask "are we MiCA compliant?", you need to answer "are we MiCA-regulated at all?" Misclassifying a security as a utility token is not a MiCA problem; it is a MiFID II problem with a different set of consequences.

#The Three MiCA Token Categories and What They Require

MiCA's three regulated categories have fundamentally different requirements. The category you fall into is the single most consequential variable in your compliance planning.

Asset-Referenced Tokens (ARTs): ARTs are tokens that reference the value of multiple currencies, one or more commodities, one or more crypto-assets, or a basket of these assets. Backed multi-asset stablecoins sit here. Full authorization from your home-member-state National Competent Authority (NCCA) is required before issuance. Reserve asset requirements apply from day one: the reserve must be legally segregated, held in custody, and cover 100% of outstanding claims. Redemption rights must be granted to all holders at par value. If your ART exceeds 10 million transactions per day or holds reserves above certain EUR thresholds, you become a "significant ART" subject to direct EBA oversight (Source: MiCA Articles 17-46, EUR-Lex).

E-Money Tokens (EMTs): EMTs reference a single fiat currency. Think: a euro-pegged stablecoin. The issuer must be a licensed EU credit institution or an electronic money institution (EMI). If you are not already licensed as one of those, you either license before launch or you partner with a licensed entity for the issuance structure. Reserve composition must be entirely in the referenced currency. Holders have a continuous redemption right at par on request. The design simplicity of EMTs is their compliance advantage: a single reference currency means a cleaner reserve structure and a narrower authorization scope than ARTs (Source: MiCA Articles 48-55, EUR-Lex). EY-Parthenon global institutional digital assets research identifies the EMT licensing pathway as a lower-friction route to EU market access for stablecoin issuers with an existing EMI license.

Other Crypto-Assets (Utility, Governance, Access Tokens): Everything that does not fit ART or EMT falls here: utility tokens, governance tokens, access tokens, and most community tokens. The requirement is a white paper notification, not full authorization, as long as you stay below the 10 million EUR issuance threshold per 12-month rolling period. Above that threshold, you notify your NCCA. Below it, you can self-certify. The white paper must still comply with MiCA Article 6 content requirements; it is a regulatory disclosure document, not a marketing whitepaper.

The table shows the key distinctions across all three categories. For additional context on the broader regulatory framework shaping token design today, see our overview of tokenomics compliance requirements.

#How Token Design Choices Affect Your Classification

Most projects approach MiCA compliance as a legal question. It is a design question first. The choices you make in your token model before writing smart contract code determine your MiCA token classification, and changing that classification after deployment is expensive.

Redemption mechanism design. If your token includes a mechanism by which holders can redeem against a reserve pool, MiCA's ART analysis kicks in unless the reference is a single fiat currency. The question is not just "do we have a buyback program?" but "does the buyback guarantee return of a specified value denominated in a reference asset?" A market buyback funded from protocol treasury is different from a redemption mechanism that guarantees parity with a basket of assets. The first is a tokenomics decision. The second is an ART trigger.

Revenue distribution to holders. Governance tokens that distribute protocol revenue directly to token holders in a defined proportion introduce an ART-adjacent signal to regulators and, separately, a MiFID II securities analysis risk. The safer design pattern routes protocol revenue through discretionary distributions, buybacks of the open-market token supply, or treasury reinvestment, rather than through automatic pro-rata distributions that resemble dividend mechanics. For projects navigating the EMT and ART boundary in stablecoin design specifically, our breakdown of stablecoin mechanism design and how mechanisms determine regulatory classification covers the mechanism-level decisions in detail.

Staking yields denominated in stable value. When a staking program pays rewards denominated in a stablecoin or promises yield pegged to a fiat reference, MiCA reviewers may read the staked token as part of an EMT-adjacent structure. Free-floating token emissions paid in the native protocol token carry a cleaner analysis: there is no reference asset, no redemption right, and no stable value peg.

Geographic distribution gating. MiCA applies based on where you offer and admit to trading, not solely where your users are domiciled. Projects that use geographic access controls to restrict EU user interaction reduce their MiCA scope, but this is a risk-reduction tactic, not an exemption. If EU-domiciled venture investors hold your tokens or if your token is listed on an EU-regulated exchange, geographic blocking of retail users does not eliminate MiCA analysis.

Governance weighting with no revenue share. Pure governance tokens with no reserve backing, no reference-asset peg, no guaranteed redemption, and no automatic revenue distribution sit closest to the notification-only path for other crypto-assets. "Pure" is the operative word. Any introduced mechanic that implies a return based on a reference asset reopens the ART analysis.

The tradeoff is real: governance structures that maximize holder alignment through revenue sharing often maximize regulatory complexity. Getting this right at design phase costs a fraction of retrofitting it under time pressure or after a regulatory inquiry.

#The MiCA White Paper Requirement and What It Must Contain

All three MiCA token categories require a white paper before offering or admission to trading, with limited exceptions for very small projects and private placements to fewer than 150 EU persons per member state (Source: MiCA Articles 4-14, EUR-Lex).

The MiCA white paper is a regulatory disclosure instrument. It is not the same as your tokenomics whitepaper or your project pitch deck. The mandatory contents differ materially by category.

For other crypto-assets, the white paper must include: a description of the issuer; a description of the project; a description of the rights and obligations attached to the token; the underlying technology and protocols; the risks relevant to the issuer, the crypto-asset, and the implementation of the project; and the MiCA-specific disclaimer language. The disclosure obligation is forward-looking: you are making representations about the token's characteristics at the time of issuance.

For ARTs specifically, the white paper is just the starting point. Ongoing disclosure obligations include quarterly reserve reports, incident reporting within defined SLA windows, and significant holder reporting when any single entity exceeds 20% of outstanding supply. The documentation burden does not end at launch.

The MiCA regulation tokenomics documentation that MiCA's white paper requires overlaps heavily with a well-built tokenomics data room: supply architecture, rights and obligations per token class, governance mechanism design, allocation and vesting structure, and treasury reserve policy. Projects that have already built institutional-grade tokenomics documentation have a material head start. Projects that have not are building the white paper and the tokenomics model simultaneously, which tends to surface design problems at the worst possible time. If you want to understand what a complete tokenomics documentation package looks like, what a tokenomics data room contains and why investors expect one explains the standard.

#Common MiCA Compliance Mistakes We See

After advising 80+ projects on token design in a tightening regulatory environment, the MiCA compliance failure patterns are consistent. MiCA has introduced a new layer, but the underlying mistakes are the same ones that have been costing crypto-asset issuers since the first enforcement cycle.

Treating MiCA as a post-launch legal task. Token design is fixed before smart contract deployment. If your redemption mechanic qualifies your token as an ART, that classification does not disappear because your lawyer reviews it after launch. It means you are operating an unauthorized ART. Retrofitting the classification requires a re-design of core token mechanics, re-notification or re-authorization with the NCCA, and in some cases a voluntary suspension of trading until the process completes.

Missing the significant-issuance threshold. The 10 million EUR per 12-month exemption applies only to the "other crypto-assets" category. ARTs and EMTs have no equivalent notification-only path below a threshold: they require full authorization regardless of issuance size. Teams assume small-project exemptions cover them across all categories. That assumption is wrong and it is expensive to correct.

Confusing geographic user exclusion with MiCA exemption. Blocking EU-resident retail users from your front-end interface reduces exposure but does not eliminate MiCA analysis. If EU institutional investors hold your token in a SAFT or token warrant structure, or if your token is listed on any EU-regulated trading venue, MiCA applies. The relevant question is not "do we block EU users?" but "do we have any EU nexus through investors, trading venues, or marketing activities?"

Dual-category ambiguity by design. Projects that build governance tokens with optional stablecoin conversion features, or stablecoins with embedded voting mechanics, create instruments that MiCA reviewers may analyze under both ART and EMT frameworks simultaneously. Resolving that ambiguity with an NCCA or in front of an EU court is not fast, not cheap, and not certain.

Underestimating documentation lead time. ART authorization involves a formal application to an NCCA, a review period of up to three months from a complete application, and back-and-forth on documentation deficiencies that can extend the timeline substantially. Projects that begin the authorization process 60 days before planned token launch are not compliant. They are late.

#MiCA's Enforcement Timeline and What Issuers Need to Do Now

The June 30, 2024 effective date for ARTs and EMTs is behind us. The December 30, 2024 deadline for crypto-asset service providers has passed. Transition periods extended to projects already operating before those dates are expiring through mid-2026 (Source: MiCA Regulation (EU) 2023/1114, Official Journal of the European Union).

The June through August 2026 window is the critical action period for any crypto-asset issuer compliance review. NCCAs across EU member states are moving from passive monitoring to active enforcement. Projects that cannot demonstrate completed MiCA compliance classification analysis, white paper preparation, or active NCCA notification are operating with increasing regulatory risk.

Five actions matter this quarter:

1. Classify your token. MiCA Articles 4-16 (other crypto-assets), 17-46 (ARTs), and 48-55 (EMTs) are the statutory tests. Run your token design against each category. If it is ambiguous, get legal opinion now, not after you have issued.

2. Assess your EU nexus. Identify every EU touchpoint: investors, advisors, listed exchanges, marketing activity. Each one is a potential scope trigger.

3. If ART or EMT path: engage EU counsel and begin NCCA notification. Authorization lead times mean Q4 2026 launches require applications in Q2-Q3 2026.

4. If other crypto-asset path: prepare your white paper to Article 6 standards. This is a disclosure document, not a pitch deck. It needs tokenomics documentation that can stand regulatory review.

5. Run a tokenomics data room review. The MiCA white paper will surface every gap in your token model documentation. Better to find those gaps in a structured review than in an NCCA inquiry. Our tokenomics data room service is built to produce exactly the documentation a MiCA white paper requires.

The projects that complete this analysis in 2026 avoid the retrofitting cost. The ones that don't will be redesigning under regulatory pressure with a shorter runway and fewer options.

#Frequently Asked Questions

What tokens does MiCA cover?

MiCA covers three categories: Asset-Referenced Tokens (ARTs), E-Money Tokens (EMTs), and other crypto-assets including utility tokens, governance tokens, and access tokens. It does not cover DeFi protocols operating without an identifiable issuer, genuinely unique non-fungible tokens (NFTs), or financial instruments already regulated under MiFID II.

Does MiCA apply to governance tokens?

Most governance tokens fall under MiCA's other crypto-assets category. If your governance token does not reference a currency or commodity, does not grant guaranteed redemption rights, and does not automatically distribute protocol revenue to holders in a defined proportion, it is likely subject only to the white paper notification requirement, not full authorization. Any revenue distribution mechanic or reference-asset structure changes this analysis.

What must a MiCA white paper contain?

A MiCA white paper for other crypto-assets must include a description of the issuer and the project, a description of the rights and obligations attached to the token, the underlying technology and protocols, relevant risks, and MiCA-specific disclaimer language. ARTs require additional disclosures on reserve composition and redemption rights. The white paper must be notified to the relevant National Competent Authority before the token is offered or admitted to trading.

When did MiCA come into force?

MiCA entered full force on June 30, 2024 for ARTs and EMTs. The deadline for crypto-asset service providers was December 30, 2024. Transition periods for projects already operating before those dates are expiring through mid-2026.

How does MiCA affect DeFi projects?

MiCA explicitly excludes DeFi protocols operating in a fully decentralized manner from its scope. However, "fully decentralized" has no EU safe-harbor definition. Projects that claim this exclusion are making a factual assertion that National Competent Authorities can challenge. Projects with identifiable issuers, centralized governance, or upgrade rights should seek legal analysis before relying on the decentralization exclusion.

If you're building onchain and need your token design and compliance documentation to hold up under EU regulatory scrutiny, book a strategy call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.